When two or more people decide to start a business together, choosing the right legal structure can mean the difference between personal financial protection and unlimited liability. A partnership LLC combines the operational flexibility of a traditional partnership with the liability shield that limited liability companies offer—but the terminology itself often confuses new business owners.

Understanding how multi-member LLCs work, how they're taxed, and what legal protections they provide helps you make an informed decision before filing formation documents or signing operating agreements with your co-founders.

What Is a Partnership LLC?

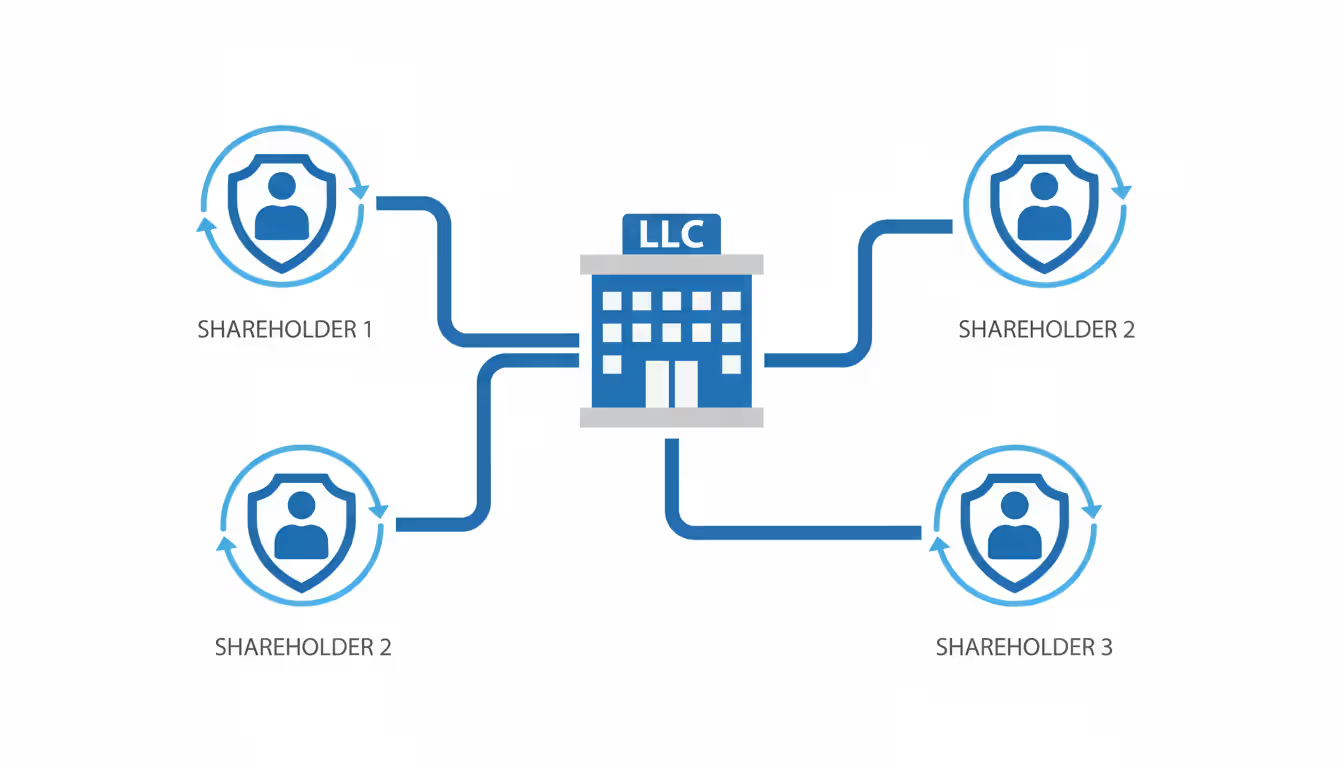

A partnership LLC is simply a limited liability company owned by two or more members. The IRS and most state laws refer to this structure as a multi-member LLC, though many entrepreneurs use "partnership LLC" colloquially because the business operates much like a partnership while maintaining LLC protections.

The confusion stems from mixing two distinct legal concepts. A partnership—whether general or limited—is one type of business entity. An LLC is a completely different entity type. When people say "partnership LLC," they typically mean a multi-member LLC that the IRS taxes as a partnership by default.

Here's what defines this structure: Multiple owners (called members rather than partners) form an LLC by filing Articles of Organization with their state. Each member contributes capital, expertise, or both. The LLC itself owns business assets and enters contracts. Members enjoy limited liability protection, meaning creditors generally cannot pursue their personal assets to satisfy business debts.

The llc partnership structure offers operational flexibility that corporations lack. Members can distribute profits disproportionately to ownership percentages, create different classes of membership, and customize management arrangements. A member who contributes 30% of startup capital might receive 50% of profits if the operating agreement specifies that arrangement.

Author: Marcus Ellwood;

Source: craftydeb.com

Unlike single-member LLCs, which some states treat with additional scrutiny in liability cases, multi-member LLCs benefit from stronger legal precedent supporting the separation between business and personal obligations. Courts have historically been more willing to "pierce the corporate veil" of single-member entities when owners fail to maintain proper formalities.

How Partnership LLCs Differ from Other Business Structures

Choosing between an LLC and traditional partnership structures affects everything from personal liability to tax complexity and formation costs. The differences matter most when disputes arise, tax bills come due, or creditors pursue payment.

General Partnership vs LLC

A general partnership forms automatically when two or more people operate a business for profit without filing formal entity documents. You and a friend start selling handmade furniture at farmers markets, split the revenue, and share expenses? You've created a general partnership whether you intended to or not.

This default structure creates significant risk. Every partner bears unlimited personal liability for business debts and the actions of other partners. If your partner causes a car accident while delivering furniture, creditors can pursue your personal bank accounts, home equity, and other assets. One partner's poor decision exposes everyone.

General partnerships also dissolve automatically when a partner dies or withdraws, unless the partnership agreement states otherwise. The business essentially ceases to exist legally, forcing remaining partners to form a new entity or operate as sole proprietors.

An LLC eliminates these problems. Members face liability only up to their capital contributions in most circumstances. If the LLC owes $200,000 and you invested $30,000, creditors cannot take your house or personal savings (assuming you've maintained proper LLC formalities). Your personal exposure caps at the $30,000 already invested.

The LLC continues existing when members leave or die. Membership interests transfer according to the operating agreement rather than forcing dissolution. This continuity protects business relationships, contracts, and ongoing operations.

Formation requires more upfront work. You must file Articles of Organization, pay state filing fees ($50–$500 depending on location), and maintain annual compliance requirements. General partnerships need none of this, though smart partners still draft partnership agreements.

Limited Partnership vs LLC

Limited partnerships (LPs) offer a middle ground that still falls short of LLC protections. An LP requires at least one general partner with unlimited liability and one limited partner whose liability caps at their investment amount.

The general partner manages daily operations and bears full personal risk. Limited partners function as passive investors—they contribute capital but cannot participate in management without losing their liability protection. This restriction makes LPs useful for investment vehicles but awkward for operating businesses where all owners want management input.

Compare this to a multi-member LLC. Every member enjoys limited liability regardless of their management role. You can actively run the business, make daily decisions, and still protect personal assets. The operating agreement determines who manages what, completely separate from liability considerations.

Tax treatment differs slightly. Both LPs and multi-member LLCs default to partnership taxation, but LLCs offer easier paths to alternative tax elections. An LLC can elect S-corporation status with a simple IRS form, potentially reducing self-employment taxes. LPs face more complications when changing tax treatment.

Formation costs run similar for both structures, though LPs require identifying general and limited partners in formation documents. This creates rigidity—converting a limited partner to a general partner later requires amending state filings. LLC members switch management roles by updating their operating agreement without state involvement.

Feature

General Partnership

Limited Partnership

Multi-Member LLC

Formation Requirements

No state filing needed; forms automatically

File Certificate of Limited Partnership; designate GP and LPs

File Articles of Organization with state

Liability Protection

Unlimited personal liability for all partners

GP has unlimited liability; LPs protected if passive

All members have limited liability regardless of role

Tax Treatment

Pass-through (partnership taxation)

Pass-through (partnership taxation)

Pass-through by default; can elect corporate taxation

Management Structure

All partners can manage

Only GP manages; LPs lose protection if active

Flexible; all members can manage or designate managers

Compliance Burden

Minimal; no annual state filings

Annual reports in most states

Annual reports and fees in most states

How Multi-Member LLCs Are Taxed

The IRS doesn't recognize LLCs as a distinct tax category. Instead, multi-member LLCs default to partnership taxation unless members actively elect different treatment. This creates flexibility but also requires understanding several tax concepts that single-owner businesses avoid.

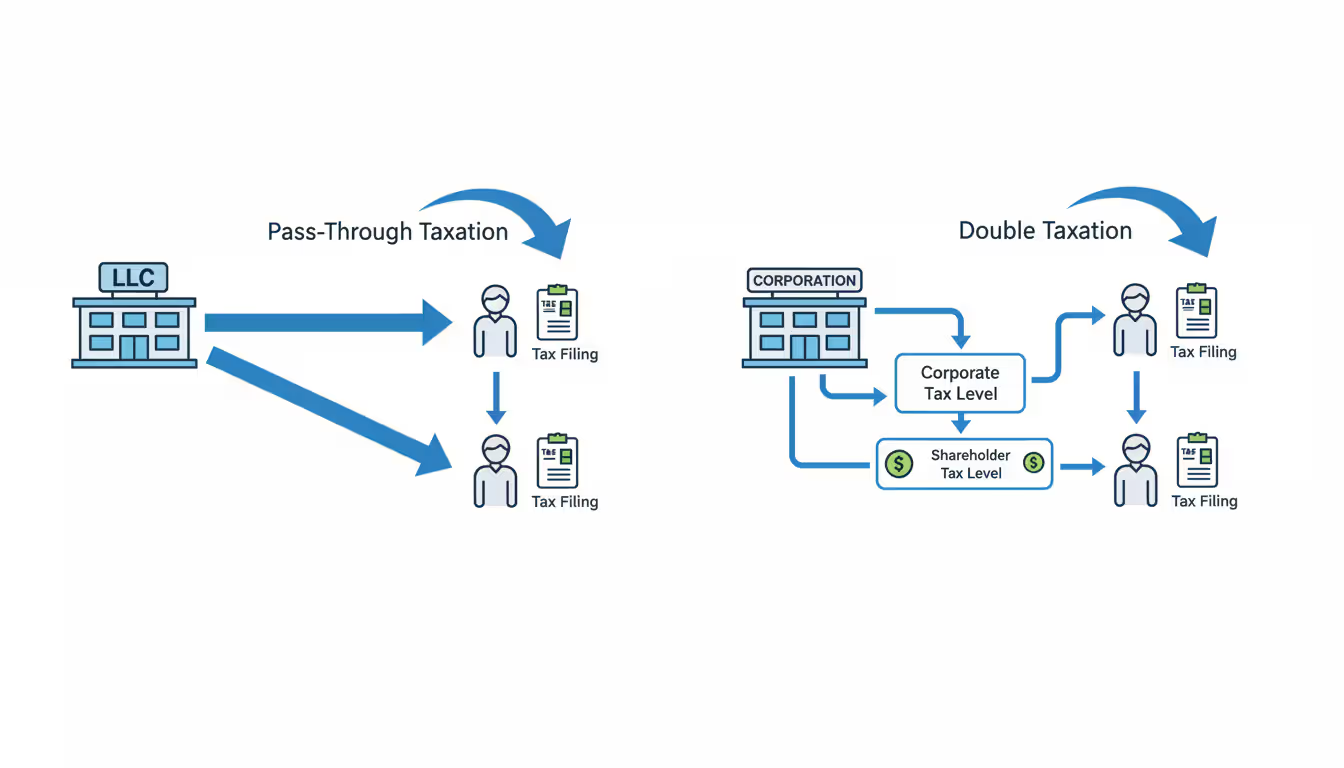

Partnership taxation means the LLC itself pays no federal income tax. Instead, profits and losses "pass through" to members, who report their share on personal tax returns. The LLC files Form 1065 (informational return) annually and issues each member a Schedule K-1 showing their portion of income, deductions, and credits.

This pass-through structure avoids the double taxation that C-corporations face. Corporate profits get taxed at the entity level, then shareholders pay personal income tax on dividends. LLC members pay tax only once, at their individual rates.

Members pay self-employment tax (Social Security and Medicare) on their share of LLC profits if they actively participate in the business. For 2026, self-employment tax runs 15.3% on the first $168,600 of net earnings, then 2.9% above that threshold. This often surprises new LLC owners who expect to pay only income tax.

Author: Marcus Ellwood;

Source: craftydeb.com

The operating agreement determines profit distribution, which doesn't need to match ownership percentages. Three members might own equal 33.3% interests but agree to split profits 50/25/25 based on different roles and contributions. The IRS respects these "special allocations" if they have "substantial economic effect"—meaning real economic consequences beyond tax avoidance.

Members can elect corporate taxation by filing Form 8832. This makes sense when profits significantly exceed reasonable compensation for member work. Under S-corporation taxation (requiring Form 2553), active members take salaries subject to payroll taxes, but remaining profits distribute as dividends that avoid self-employment tax.

Consider two members running a consulting LLC generating $400,000 annual profit. Under default partnership taxation, each pays self-employment tax on their $200,000 share—roughly $24,000 each. Electing S-corp status, they might take $120,000 salaries (subject to payroll tax) and receive $80,000 in distributions (no self-employment tax). This saves approximately $12,000 per member, minus additional payroll processing costs.

The election requires careful analysis. S-corporations face restrictions: no more than 100 shareholders, only certain types of owners allowed, one class of stock. You also must run payroll, file additional tax forms, and justify salary amounts to the IRS. Many small multi-member LLCs stick with default partnership taxation until profits justify the administrative burden.

Partnership LLC Operating Agreement Essentials

An operating agreement functions as the constitution for your LLC—the document that governs member relationships, decision-making authority, financial arrangements, and exit procedures. State law provides default rules when LLCs lack written agreements, but those defaults rarely match what members actually want.

Most states don't legally require operating agreements for LLCs, but operating without one invites disaster. Verbal understandings fail when memories differ. Handshake deals crumble under financial pressure. The time to document expectations is before disputes arise, not during them.

Member contributions and ownership percentages should be specified precisely. One member contributes $75,000 cash, another provides $50,000 in equipment, and a third offers sweat equity valued at $25,000. The agreement must state how these different contribution types convert to ownership percentages and whether future contributions are required.

Profit and loss allocation determines who receives what when the business makes or loses money. The default rule—splitting according to ownership percentages—works for many LLCs but not all. Some agreements allocate losses differently than profits, or give certain members preferential returns up to specified amounts before splitting remaining profits equally.

Management structure defines who makes daily decisions versus major strategic choices. Member-managed LLCs let all owners participate in operations. Manager-managed LLCs designate specific members or outside professionals to run the business, while other members function as passive investors. The agreement should list which decisions require unanimous consent (admitting new members, selling major assets) versus simple majority votes.

Capital calls and additional contributions become critical when the business needs more money. Can the LLC require members to invest additional capital? What happens if a member refuses or cannot contribute? Some agreements allow non-contributing members to maintain ownership but dilute their percentage. Others trigger buyout provisions or convert their interest to a different class with reduced rights.

Transfer restrictions protect remaining members from unwanted business partners. Most agreements require member approval before anyone sells or transfers their interest. Some grant existing members a right of first refusal to purchase the departing member's share at the same terms offered to outside buyers.

Buy-sell provisions establish what happens when a member dies, becomes disabled, wants to retire, or gets divorced. Without clear procedures, a deceased member's ownership might pass to their spouse or children—people with no interest in operating the business. Buyout formulas (based on book value, multiple of earnings, or independent appraisal) prevent disputes over price.

Dispute resolution mechanisms save enormous legal fees. Many agreements require mediation before members can file lawsuits, or specify binding arbitration for certain types of conflicts. Some include "shotgun clauses"—if members reach an impasse, one can name a price for the entire business, and the other must either buy at that price or sell at that price.

I've seen multi-member LLCs implode over issues that a properly drafted operating agreement would have resolved in a single paragraph.The $2,000 you spend on legal fees upfront can prevent $50,000 in litigation costs later. More importantly, the process of negotiating the agreement forces members to discuss uncomfortable topics—money, control, exit scenarios—while they still like each other

— Jennifer Walton

How to Form a Partnership LLC

Forming a multi-member LLC involves more than filing a single form. The process requires coordinating state filings, federal tax registrations, and internal governance documents. Missing steps creates compliance gaps that can undermine liability protection.

Choose your formation state. Most small businesses form in their home state—the state where they'll physically operate. Forming in Delaware or Nevada offers few advantages for typical multi-member LLCs despite aggressive marketing from formation services. You'll still need to register as a foreign LLC in your home state (paying fees in both states) and gain no meaningful asset protection or tax benefits.

Select and reserve your business name. Check your state's business entity database to ensure your desired name is available and complies with state requirements. Most states require LLC names to include "Limited Liability Company," "LLC," or "L.L.C." Reserve the name if you're not ready to file immediately—most states allow 60-120 day reservations for $10-$50.

Designate a registered agent. Every LLC must maintain a registered agent with a physical address in the formation state to receive legal documents and official correspondence. One member can serve this role, or you can hire a commercial service ($100-$300 annually). The agent's address becomes public record.

Author: Marcus Ellwood;

Source: craftydeb.com

File Articles of Organization. This document officially creates your LLC. Required information varies by state but typically includes: LLC name, registered agent details, management structure (member-managed or manager-managed), and sometimes member names. Filing fees range from $50 (Kentucky, Mississippi) to $500 (Massachusetts) with most states charging $100-$200.

Processing times vary. Online filings in some states complete within 1-2 business days. Paper filings might take 2-4 weeks. Expedited processing costs extra—$50 to $1,000 depending on the state and how fast you need approval.

Obtain an Employer Identification Number (EIN). The IRS requires multi-member LLCs to have an EIN even without employees. Apply free online at IRS.gov—the process takes 10 minutes and provides your EIN immediately. You'll need this number to open business bank accounts, file tax returns, and hire employees.

Draft and execute your operating agreement. Do this immediately after formation, even though most states don't require filing it. All members should review, negotiate, and sign the agreement. Store the original with other corporate records and provide copies to members. Generic templates miss critical provisions—expect to pay $1,000-$3,000 for attorney-drafted agreements customized to your situation.

Open a business bank account. Maintaining separate finances is crucial for preserving liability protection. Mixing business and personal funds gives creditors arguments that the LLC is merely your "alter ego" rather than a distinct entity. Bring your Articles of Organization, EIN confirmation, and operating agreement to the bank.

Obtain necessary licenses and permits. Requirements vary by industry and location. Federal licenses apply to specific industries (firearms, alcohol, agriculture). State professional licenses cover regulated occupations. Local business licenses and zoning permits come from city or county offices. Your state's business portal typically provides industry-specific checklists.

File beneficial ownership reports. The Corporate Transparency Act requires most LLCs formed after 2023 to file beneficial ownership information with FinCEN, identifying individuals who own 25% or more of the company or exercise substantial control. Existing LLCs had until January 1, 2025 to comply. Failure to file carries penalties up to $500 per day.

When a Partnership LLC Makes Sense for Your Business

Multi-member LLCs work brilliantly for some businesses and create unnecessary complexity for others. The structure makes most sense when liability protection, management flexibility, and pass-through taxation all matter to your specific situation.

Professional service partnerships benefit significantly. Two accountants, three attorneys, or four consultants starting a firm together want liability protection from each other's malpractice while maintaining partnership-style operations. An LLC shields each member from the others' professional errors (though not from their own negligence).

Real estate investment groups frequently use multi-member LLCs to hold rental properties. The structure protects members' personal assets from tenant lawsuits while allowing flexible profit distributions. Some members contribute capital, others handle property management, and the operating agreement allocates returns accordingly.

Family businesses with multiple active relatives often choose LLC structures. Parents and adult children operating a restaurant or retail store together appreciate the flexibility to allocate profits based on contribution rather than strict ownership percentages. The operating agreement can include succession planning provisions that keep the business in family hands.

Creative partnerships like design studios, marketing agencies, or video production companies value the LLC's flexibility around equity and compensation. A senior creative director might own 40% but receive only 25% of profits, with the difference compensating for salary differences with other members.

The structure makes less sense for businesses planning rapid growth with outside investors. Venture capital firms strongly prefer C-corporations because LLC tax treatment creates complications for institutional investors. If you're building a tech startup seeking VC funding, start as a corporation or plan to convert later.

Solo founders should form single-member LLCs rather than multi-member structures. Adding a spouse or family member solely to create a "partnership LLC" provides no benefits and complicates taxes. Wait until you have a genuine business partner with active involvement.

Very small side businesses might not justify the administrative burden. If you and a friend occasionally flip furniture for modest profits, the annual LLC fees ($0-$800 depending on state) and tax preparation costs (partnership returns run $500-$1,500 with a CPA) might exceed the value of liability protection. Consider whether adequate insurance provides sufficient protection at lower cost.

Common Mistakes When Structuring a Partnership LLC

Even experienced entrepreneurs make errors when forming multi-member LLCs. These mistakes often remain invisible until disputes arise or tax problems surface—exactly when fixing them becomes most expensive.

Operating without a written agreement tops the list. Members who trust each other assume verbal understandings suffice. Three years later, when the business succeeds and one member wants to buy out another, they discover they remember different terms. Was profit split based on time invested or capital contributed? What formula determines buyout price? State default rules rarely match anyone's expectations.

Using generic operating agreement templates creates similar problems. A $39 online template might cover basic governance but misses provisions specific to your industry or situation. It won't address what happens if one member stops working but retains ownership, or how to handle a member who wants to start a competing business.

Author: Marcus Ellwood;

Source: craftydeb.com

Misunderstanding tax elections costs members thousands unnecessarily. Some LLCs elect S-corporation status when partnership taxation would save money. Others stick with default treatment when an S-corp election would reduce self-employment taxes by $15,000 annually. Run the numbers with a CPA before choosing—and rerun them as circumstances change.

Failing to document capital contributions creates disputes later. One member contributes $50,000 cash, another provides $30,000 in equipment, and a third offers services. Without written documentation of how these contributions convert to ownership percentages, members argue about who owns what when distributing profits or selling the business.

Ignoring ongoing compliance requirements undermines liability protection. States require annual reports, franchise taxes, or both. Miss these filings and your LLC falls into "bad standing," losing the ability to sue in court and potentially exposing members to personal liability. Set calendar reminders for annual deadlines.

Commingling personal and business finances destroys the liability shield. Using the LLC bank account to pay your mortgage, or depositing LLC revenue into personal accounts, gives creditors ammunition to argue the LLC is a sham. Maintain strict separation even when inconvenient.

Inadequate capitalization creates problems from day one. If members contribute minimal capital and immediately drain profits, creditors can argue the LLC was undercapitalized—essentially a shell entity. Maintain reasonable reserves and don't distribute every dollar of profit immediately.

Failing to update the operating agreement as circumstances change leaves you operating under outdated terms. A member leaves, you admit a new member, or business operations change significantly—amend the agreement to reflect reality. Operating under obsolete provisions invites disputes.

Frequently Asked Questions

Can a single-member LLC be a partnership?

No. By definition, a partnership requires two or more owners. A single-member LLC is taxed as a sole proprietorship by default (or can elect corporate taxation), but never as a partnership. If you're the only owner, you have a single-member LLC, not a partnership LLC. Adding a second member automatically converts the entity to multi-member status and changes the default tax treatment to partnership taxation.

Do I need an operating agreement for a partnership LLC?

Legally, most states don't require operating agreements, but practically, you absolutely need one. Without a written agreement, state default rules govern your LLC—and those defaults rarely match what members actually want. The operating agreement controls profit distribution, management authority, member admission and removal, and buyout procedures. Skipping this document is one of the costiest mistakes multi-member LLC owners make.

How is a partnership LLC taxed by the IRS?

The IRS taxes multi-member LLCs as partnerships by default. The LLC files Form 1065 (informational return) and issues each member a Schedule K-1 showing their share of income, deductions, and credits. Members report this information on their personal tax returns and pay tax at individual rates. The LLC itself pays no federal income tax. Members can elect to be taxed as a corporation instead by filing Form 8832, or as an S-corporation by filing Form 2553.

What's the main difference between an LLC and a general partnership?

Liability protection is the critical difference. General partnership members have unlimited personal liability for business debts and other partners' actions. LLC members' personal assets are generally protected—liability is limited to their investment in the company. Additionally, LLCs require state formation filings while general partnerships form automatically when people conduct business together. LLCs continue existing when members leave, while general partnerships typically dissolve.

Can a partnership LLC elect S-corp taxation?

Yes, multi-member LLCs can elect S-corporation tax treatment by filing Form 2553 with the IRS. This election can reduce self-employment taxes for active members by allowing them to split income between salary (subject to payroll taxes) and distributions (not subject to self-employment tax). However, S-corp status requires running payroll, filing additional tax forms, and meeting IRS requirements for reasonable compensation. The tax savings must justify the additional administrative burden and costs.

How do you split profits in a multi-member LLC?

The operating agreement determines profit distribution, which doesn't need to match ownership percentages. Members might own equal shares but split profits unequally based on roles, contributions, or other factors. The IRS allows these "special allocations" if they have substantial economic effect—meaning real economic consequences beyond tax benefits. Without an operating agreement specifying distribution terms, state law defaults to splitting profits according to ownership percentages.

A multi-member LLC combines liability protection with operational flexibility, making it an attractive structure for many co-owned businesses. The entity shields your personal assets from business creditors while allowing customized management arrangements and profit distributions that partnerships and corporations cannot easily match.

Success requires more than filing Articles of Organization. A comprehensive operating agreement protects all members by documenting expectations, procedures, and resolution mechanisms before conflicts arise. Understanding partnership taxation helps you make informed elections that minimize tax burden. Maintaining proper formalities—separate finances, annual compliance, adequate capitalization—preserves the liability protection that makes the structure valuable.

The formation process takes several weeks and costs $1,000–$3,000 including state fees and professional guidance. That investment buys legal protection and operational clarity worth far more when business challenges emerge. Whether you're starting a professional practice, investment venture, or creative partnership, a properly structured multi-member LLC provides the foundation for sustainable growth with manageable personal risk.

When you form a corporation or LLC, state law requires you to designate someone to accept legal papers on behalf of your company. That person or entity is your registered agent. Without one, you can't complete your business formation paperwork, and your company risks serious compliance issues down the line

Every US business must submit mandatory statutory filings to government agencies. Understand formation documents, annual reports, tax filings, and employment requirements by entity type—plus common mistakes that trigger penalties and systems to maintain year-round compliance

Every LLC must maintain a registered agent—a designated contact for legal documents and government correspondence. Learn what registered agents do, state-specific requirements, how to appoint or change your agent, and whether to hire a service or act as your own agent

Navigate LLC filings from formation through ongoing compliance. Learn state-specific requirements, filing timelines, costs, and common mistakes that risk your liability protection. Includes filing checklists and expert compliance strategies

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to business and corporate law, contracts, compliance, disputes, M&A, and taxation for companies.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Legal outcomes may vary depending on jurisdiction, company structure, and individual circumstances.

This website does not provide legal advice, and the information presented should not be used as a substitute for consultation with qualified corporate attorneys or legal professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.