Business owners often wonder whether they can reduce their tax burden by deducting political contributions. The answer is straightforward but frequently misunderstood: political donations made by businesses are not tax deductible under federal law. This prohibition applies regardless of business structure, contribution size, or recipient type.

Understanding the tax treatment of corporate political spending requires familiarity with specific IRS code sections, distinguishing between different types of political activity, and recognizing the narrow exceptions that exist. Many businesses inadvertently violate these rules, leading to denied deductions, penalties, and potential audits.

IRS Rules on Political Contributions and Business Taxes

Section 162(e) of the Internal Revenue Code explicitly prohibits businesses from deducting political contributions as ordinary business expenses. This provision has existed since 1962 and was strengthened through subsequent amendments. The tax treatment political contributions receive reflects a deliberate policy choice: taxpayers should not subsidize political activities through the tax system.

The IRS defines political contributions broadly to include any payment made to influence the selection, nomination, election, or appointment of any individual to federal, state, or local public office. This definition extends beyond direct candidate donations to encompass contributions to political parties, political action committees, and campaign committees.

Under irs rules political donations fall into the category of non-deductible expenses alongside fines, penalties, and illegal bribes. The rationale centers on public policy—the federal government declines to effectively subsidize political activity by allowing tax deductions that would reduce the true cost of such contributions.

The prohibition applies to all business entities: C corporations, S corporations, partnerships, limited liability companies, and sole proprietorships. Pass-through entities cannot circumvent these rules by allocating political contributions to individual owners who might attempt to deduct them personally. Individual taxpayers also cannot deduct political contributions, even when made in connection with business activities.

Author: Andrew Bellamy;

Source: craftydeb.com

Political contribution tax deductibility restrictions remain absolute. Unlike charitable contributions, which face percentage limitations but remain deductible within those bounds, political donations receive no favorable tax treatment whatsoever. A corporation that donates $100,000 to a political candidate receives zero tax benefit from that expenditure.

What Types of Political Spending Cannot Be Deducted

Businesses cannot deduct several categories of political spending, each triggering the Section 162(e) prohibition:

Direct candidate contributions represent the most obvious non-deductible category. When a business writes a check to a congressional candidate's campaign committee, that expense provides no tax benefit. The same applies to in-kind contributions such as providing office space, equipment, or staff time to a candidate.

Political party contributions similarly receive no deduction, whether directed to national, state, or local party committees. Donations to the Democratic National Committee, Republican National Committee, or state party organizations all fall under the prohibition.

PAC contributions from corporate treasuries remain non-deductible. When a corporation contributes to its own political action committee or to an independent PAC, those funds cannot reduce taxable income.

Super PAC donations and contributions to independent expenditure committees face the same treatment. These entities, which can accept unlimited contributions but cannot coordinate with candidates, still qualify as political organizations under IRS definitions.

Independent expenditures made directly by corporations—such as funding advertisements supporting or opposing candidates—are non-deductible even though Citizens United v. FEC permits such spending.

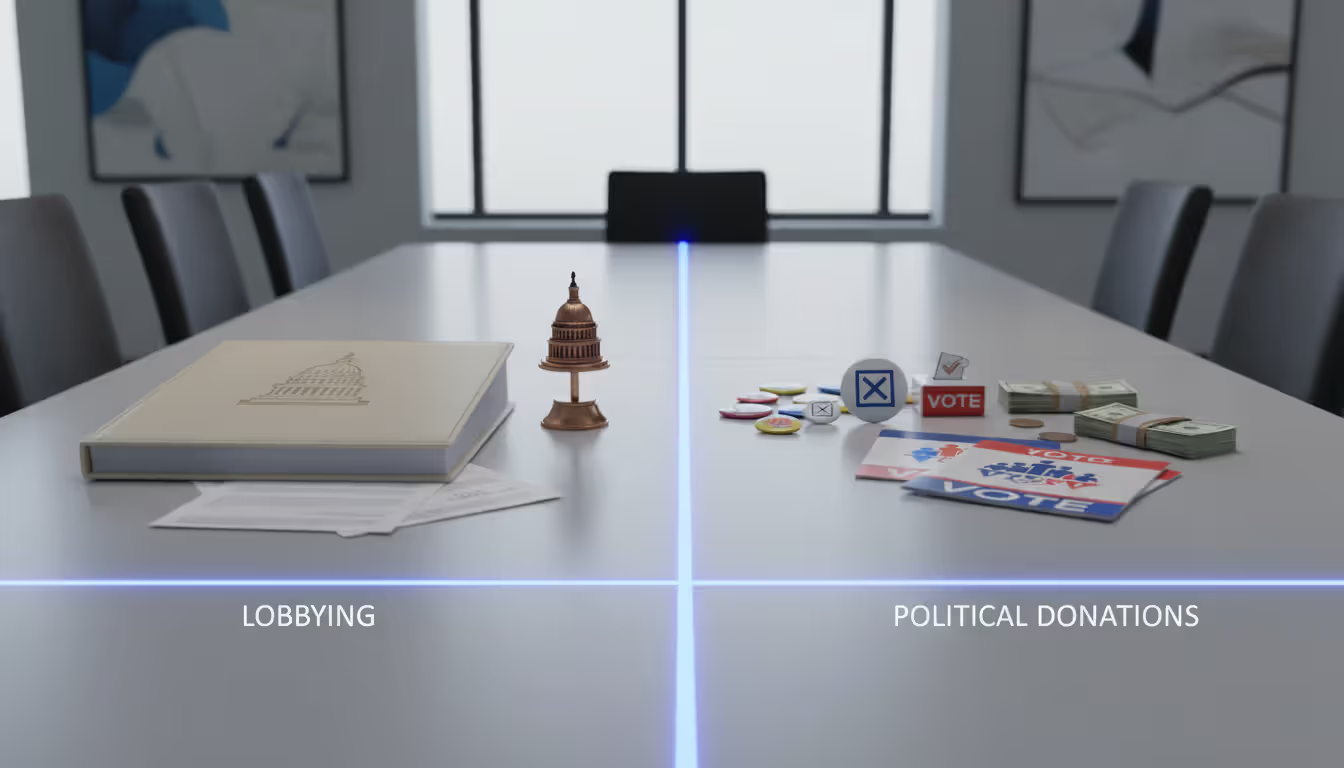

Campaign Contributions vs. Lobbying Expenses

Many business owners confuse campaign contributions with lobbying expenses, but the tax code treats them distinctly. Campaign contributions involve supporting or opposing candidates for public office. Lobbying expenses relate to influencing legislation or communicating with government officials about policy matters.

While campaign contributions receive no deductibility whatsoever, lobbying expenses face partial deductibility restrictions. This distinction matters because businesses might legitimately deduct certain advocacy activities while remaining barred from deducting any political contributions.

The key differentiator: lobbying addresses issues and legislation, while political contributions support candidates and parties. A corporation that spends money urging Congress to pass specific tax reform legislation engages in lobbying. That same corporation writing a check to a senator's re-election campaign makes a political contribution.

Businesses sometimes attempt to characterize political contributions as lobbying expenses to claim deductions. The IRS scrutinizes such classifications carefully. Attending a fundraising dinner for a candidate, even when policy issues are discussed, constitutes political activity rather than lobbying.

Author: Andrew Bellamy;

Source: craftydeb.com

Tax Treatment of PAC Contributions and Corporate Political Spending

Corporate political action committees create confusion regarding pac contribution tax treatment. Understanding the structure clarifies why these contributions remain non-deductible.

A corporate PAC operates as a separate segregated fund established by a corporation to collect voluntary contributions from eligible individuals (typically executives, shareholders, and employees). The corporation can pay administrative costs for operating the PAC—expenses like accounting, legal compliance, and fundraising overhead. These administrative expenses are tax deductible as ordinary business expenses.

However, the actual contributions made from the PAC to candidates remain non-deductible. The distinction matters: a corporation spending $50,000 on PAC administration can deduct that amount, but the $200,000 in contributions distributed from the PAC to candidates provides no tax benefit.

Corporate political spending law varies at the state level, creating additional complexity. Some states permit direct corporate contributions to candidates, while others prohibit them. Regardless of state law permissibility, federal tax law denies deductions for these contributions.

Business political contribution limits established by federal campaign finance law operate independently from tax deductibility rules. A contribution might comply with Federal Election Commission regulations while still being non-deductible. Conversely, an unlimited contribution to a super PAC might be legally permissible but provides no tax advantage.

Corporations occasionally establish multiple PACs for different purposes—federal versus state elections, or candidate contributions versus independent expenditures. The tax treatment remains consistent: administrative costs are deductible, contributions are not.

Can Businesses Deduct Any Political or Advocacy Activities

Despite the broad prohibition on deducting political contributions, businesses can deduct certain advocacy-related expenses under specific circumstances.

Trade association dues receive partial deductibility. When a business pays membership dues to a trade association that engages in both lobbying and non-political activities, the portion allocated to lobbying faces deduction limitations, while the portion allocated to direct political activity is entirely non-deductible. Trade associations must notify members annually about the non-deductible portion of their dues.

For example, a manufacturer paying $10,000 in annual dues to an industry association might receive notice that 15% relates to lobbying (subject to separate restrictions) and 5% relates to political contributions (entirely non-deductible). The member can deduct $8,000 fully, must treat $1,500 under lobbying rules, and cannot deduct the $500 political portion.

Issue advocacy that doesn't reference specific candidates may be deductible if it qualifies as ordinary business promotion or public relations. A pharmaceutical company running advertisements about the importance of drug innovation, without mentioning candidates or pending legislation, might deduct those costs as business promotion expenses.

The line between deductible issue advocacy and non-deductible political activity blurs when communications occur near elections or reference voting. The IRS applies a facts-and-circumstances test, examining timing, content, and context. An advertisement discussing healthcare policy that airs two weeks before an election and features issues central to a prominent race likely crosses into non-deductible territory.

Grassroots lobbying—encouraging the general public to contact legislators about specific legislation—faces deduction limitations similar to direct lobbying. These expenses don't constitute political contributions but fall under separate lobbying expense restrictions.

Business league memberships to organizations like chambers of commerce follow the same partial deductibility rules as trade associations. Members must reduce their deduction by the portion allocated to political activities.

Lobbying Expense Deductibility Rules for Corporations

Author: Andrew Bellamy;

Source: craftydeb.com

Lobbying expense deductibility operates under different rules than political contribution prohibitions, though both restrict tax benefits for influencing government.

Section 162(e) disallows deductions for amounts paid in connection with influencing legislation, with significant exceptions. Direct lobbying—communicating with legislators or their staff about specific legislation—is generally non-deductible. However, the de minimis exception permits deductions when in-house lobbying expenses don't exceed $2,000 during the tax year.

This threshold applies only to direct costs, not including overhead or allocated employee compensation. A small business whose government affairs director spends occasional time contacting legislators, with direct costs under $2,000 annually, can deduct all related expenses. Once direct lobbying costs exceed $2,000, none of the lobbying expenses are deductible.

Professional lobbying firms hired by corporations cannot deduct their expenses related to influencing legislation, and corporations cannot deduct fees paid to these firms for lobbying services. The prohibition flows through from service provider to client.

Businesses must maintain detailed records segregating lobbying expenses from deductible business expenses. When an employee's responsibilities include both lobbying and non-lobbying activities, compensation must be allocated proportionally. A government affairs professional spending 40% of their time on lobbying cannot have that 40% of salary and benefits deducted.

Reporting requirements accompany these restrictions. Corporations with substantial lobbying activities must disclose non-deductible amounts on tax returns. Form 1120 includes specific lines for reporting lobbying and political expenditures, even though they're not deductible.

The difference between lobbying and political contributions becomes critical: lobbying addresses legislation and policy, while political contributions support candidates. A corporation can engage in limited deductible lobbying (under the de minimis threshold) but can never deduct political contributions.

Common Mistakes Businesses Make with Political Donation Deductions

The IRS maintains strict enforcement of political contribution deduction prohibitions because the rules are unambiguous. We see businesses attempt creative characterizations—calling contributions 'business development' or 'community relations'—but Section 162(e) leaves no room for interpretation. Political donations are never deductible, and attempting to claim them triggers scrutiny that often extends to other areas of the return

— Robert Chen

Tax professionals regularly encounter errors when businesses attempt to navigate corporate political donation rules. These mistakes trigger audits, penalties, and amended returns.

Misclassifying contributions as business expenses represents the most frequent error. A business owner writes a check from the company account to a political candidate and records it as "advertising expense" or "business development." During an audit, the IRS reclassifies the expense, denies the deduction, and may assess penalties for negligent or intentional misreporting.

Attempting deductions through pass-through entities occurs when LLC or partnership owners believe distributing political contributions through the business entity creates deductibility. The tax treatment remains unchanged—political contributions are non-deductible whether made directly by an individual or allocated through a pass-through entity.

Improper allocation of mixed-use expenses happens frequently with event sponsorships. A corporation sponsors a charity golf tournament that also serves as a fundraiser for a political candidate. The business cannot deduct the portion of sponsorship fees that benefit the political campaign, even if the primary purpose involves charitable activity or business networking.

Recordkeeping failures create problems when businesses cannot substantiate the nature of expenses. A payment to a political consultant might serve legitimate, deductible purposes (market research, public relations strategy) or non-deductible purposes (campaign strategy, fundraising advice). Without detailed records, the IRS may disallow the entire deduction.

Deducting attendance at political fundraisers as entertainment was more common before the Tax Cuts and Jobs Act eliminated most entertainment deductions. Some businesses still attempt to characterize political fundraising events as business meals or networking, but these expenses remain non-deductible regardless of any business discussions that occur.

Bundling contributions with deductible expenses on financial statements obscures political spending. When businesses aggregate various expenses into broad categories, political contributions may hide within legitimate deduction categories. This practice, whether intentional or negligent, violates tax reporting requirements.

Tax Deductibility of Business Contributions by Type

Type of Contribution

Tax Deductible?

IRS Code Section

Notes

Direct candidate donation

No

162(e)(1)(B)

Completely non-deductible regardless of amount

PAC contribution

No

162(e)(1)(B)

Contributions from PAC are non-deductible; administrative costs may be deductible

Party committee donation

No

162(e)(1)(B)

Applies to national, state, and local party organizations

Lobbying expenses

Partially

162(e)(1)(A)

Non-deductible except for de minimis exception (under $2,000)

Trade association dues (political portion)

No

162(e)(3)

Association must notify members of non-deductible percentage

Issue advocacy

Sometimes

Various

Deductible if qualifies as business promotion, not political activity

501(c)(3) charitable donation

Yes

170

Subject to percentage limitations based on business entity type

501(c)(4) contribution

No

162(e)(1)(B)

Social welfare organizations engaging in political activity

Frequently Asked Questions

Can an LLC deduct political donations on its tax return?

No. Limited liability companies cannot deduct political donations regardless of tax classification. Whether taxed as a sole proprietorship, partnership, S corporation, or C corporation, the prohibition on deducting political contributions applies uniformly. LLC members also cannot deduct their allocated share of political contributions made by the entity. The non-deductibility follows the contribution through all business structures.

Are contributions to a corporate PAC tax deductible?

No. Contributions to a corporate political action committee are not tax deductible, whether made by the corporation (which is generally prohibited) or by individuals. However, corporations can deduct the administrative expenses of operating a PAC, including compliance costs, accounting fees, and fundraising overhead. Only the actual contributions distributed to candidates remain non-deductible.

What happens if a business incorrectly deducts a political donation?

The IRS will disallow the deduction during an audit, requiring the business to pay additional taxes on the incorrectly deducted amount. The business may also face accuracy-related penalties of 20% of the underpayment if the IRS determines negligence or substantial understatement. In cases of intentional misreporting, civil fraud penalties of 75% may apply. The business must file an amended return and pay interest on the underpayment from the original due date.

Can a business deduct donations to a 501(c)(4) organization?

No. Contributions to 501(c)(4) social welfare organizations are not tax deductible. Unlike 501(c)(3) charitable organizations, which receive and provide tax-deductible contributions, 501(c)(4) entities can engage in political activities and therefore don't qualify for charitable deduction treatment. This applies even when the contribution supports the organization's non-political social welfare activities.

Do state tax rules differ from federal rules on political donation deductibility?

Most states conform to federal tax treatment, making political contributions non-deductible for state income tax purposes as well. However, some states have enacted specific provisions that differ from federal law. Businesses operating in multiple states should review each jurisdiction's rules. Even in states that might permit deductions, federal tax returns must still treat political contributions as non-deductible.

Are there any reporting requirements for non-deductible political contributions?

Yes. Corporations must report certain non-deductible expenses, including political contributions, on their federal tax returns. Form 1120 includes specific lines for reporting these amounts even though they don't reduce taxable income. Additionally, publicly traded companies face SEC disclosure requirements for political spending. Campaign finance laws impose separate reporting obligations on recipients of contributions, though these don't directly affect the contributing business's tax return.

Political donations made by businesses receive no federal tax deduction under any circumstances. This prohibition, codified in Section 162(e) of the Internal Revenue Code, applies to direct candidate contributions, PAC donations, party committee support, and all other forms of political spending designed to influence elections.

The distinction between non-deductible political contributions and partially restricted lobbying expenses matters significantly for tax planning. While businesses face absolute prohibition on deducting political contributions, they may deduct certain advocacy activities and lobbying expenses under specific conditions, particularly when staying within the de minimis threshold.

Corporate political spending law permits various forms of political engagement, but tax law declines to subsidize these activities through deductions. Businesses can participate in the political process through corporate PACs, independent expenditures, and direct contributions where state law allows, but should expect zero tax benefit from these expenditures.

Proper classification and recordkeeping prevent costly mistakes. Businesses that clearly segregate political spending from deductible business expenses, maintain detailed documentation, and accurately report non-deductible amounts avoid audit complications and penalties.

Understanding these rules enables businesses to make informed decisions about political engagement. The cost of political participation is the actual out-of-pocket expense, without reduction through tax savings. This reality should inform budgeting and strategic decisions about corporate political activity.

UCC stands for the Uniform Commercial Code, a comprehensive set of laws governing commercial transactions across the United States. For business owners, attorneys, and anyone involved in buying or selling goods, understanding the UCC is essential to structuring enforceable agreements and avoiding costly disputes

Transactional law encompasses the legal work involved in business deals and commercial arrangements. Unlike litigation attorneys who resolve disputes in court, transactional lawyers structure transactions, draft agreements, and prevent legal problems before they arise

Section 382 limits NOL carryforwards after ownership changes to prevent tax loss trafficking. Learn how ownership tests work, limitation calculations, and compliance requirements for M&A transactions

Personal liability means you can be held financially responsible for business debts and lawsuits using your own assets. Understanding when protection applies, how corporate structures shield personal wealth, and where vulnerabilities exist helps you make informed decisions safeguarding your financial future

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to business and corporate law, contracts, compliance, disputes, M&A, and taxation for companies.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Legal outcomes may vary depending on jurisdiction, company structure, and individual circumstances.

This website does not provide legal advice, and the information presented should not be used as a substitute for consultation with qualified corporate attorneys or legal professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.