If you've ever dealt with corporate tax losses and ownership changes, you know the headache that Section 382 brings. This piece of the Internal Revenue Code creates a minefield for companies carrying net operating losses through mergers, acquisitions, or significant equity shifts.

Here's the reality: your company might have millions in NOL carryforwards, but one ownership change can dramatically limit—or effectively eliminate—your ability to use them. I've seen deals collapse over Section 382 complications that weren't spotted during due diligence.

The statute emerged from a 1980s problem: companies were buying and selling tax losses like trading cards. Congress shut down that market in 1986, but the solution they created imposes tracking requirements and mathematical tests that catch many businesses off guard. Miss an ownership change by even one percentage point, and you might discover the mistake years later when the IRS comes calling.

What Is Section 382 and Why Does It Exist?

Think of Section 382 as the IRS's answer to tax loss shopping. The provision caps how much of a corporation's pre-existing NOLs can reduce taxable income after the ownership structure substantially changes.

Back in the mid-1980s, a bizarre market had developed. Profitable companies would hunt for failing businesses with one valuable asset: expiring tax losses. They'd acquire these corporate shells, inject profitable operations, and use the purchased losses to eliminate tax bills. The acquired business's losses had nothing to do with the buyer's operations—pure tax arbitrage.

Congress decided this violated basic fairness. Why should a thriving business escape taxation by buying another company's old losses? The Tax Reform Act of 1986 introduced the current Section 382 framework to stop this practice.

Here's how the limitation works. When ownership of a loss company changes hands (we'll get to what that means exactly), the law imposes a ceiling on annual NOL usage. You calculate this ceiling by taking the company's fair market value right before the ownership shift and multiplying it by a federal interest rate.

Author: Marcus Ellwood;

Source: craftydeb.com

What is section 382's practical impact? Let's say your corporation carries $8 million in NOLs. You go through an ownership change when the company's worth $4 million and the applicable federal rate sits at 3%. Your annual limitation becomes $120,000 ($4 million × 3%). That's the maximum pre-change NOL you can use each year, regardless of how much taxable income you generate.

The rules cover C corporations primarily, though they reach partnerships and S corporations in specific situations. Beyond NOLs, the limitations affect capital loss carryforwards, business interest expense carryforwards, and certain credit carryforwards. You're potentially restricted for the entire carryforward period—which could span 20 years for older NOLs.

Section 382 explained another way: the government wants you to benefit from losses generated by your business operations, not from losses you purchased through ownership transactions. The annual limitation tries to approximate what the loss company would have earned on its own equity value, preventing buyers from immediately capturing the full tax benefit of acquired losses.

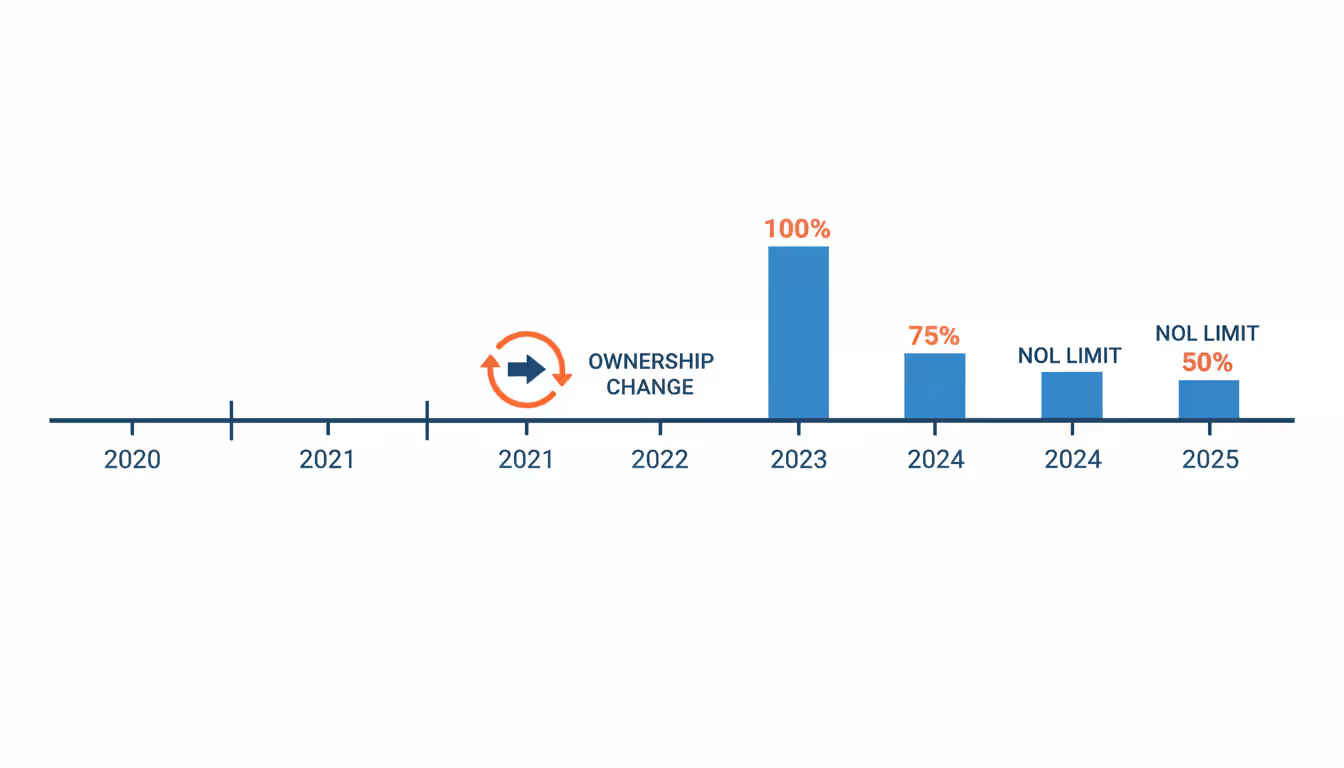

How Section 382 Ownership Changes Trigger NOL Limitations

An ownership change happens when 5% shareholders collectively increase their ownership by more than 50 percentage points during a three-year window. That sentence packs in several technical concepts that each deserve unpacking.

You're constantly looking backward across a rolling three-year period. Every time stock changes hands—through sales, redemptions, new issuances, whatever—you need to test whether the cumulative shifts have crossed the 50-point threshold. Many companies only check annually at tax time, which is a mistake that can cost millions.

The measurement compares each significant shareholder's current stake against their lowest ownership point during the testing window. You sum up all the increases. Once the total exceeds 50 percentage points, boom—ownership change.

The 5% Shareholder Rule

Section 382 doesn't make you track every single stockholder. Instead, the law focuses on "5% shareholders"—anyone owning at least 5% of the company's stock by value. Everyone below that threshold gets lumped together into what's called a "public group."

This creates an interesting dynamic. Public companies with thousands of shareholders don't need individualized tracking for most investors. But you absolutely must know when someone crosses into 5% territory, and that gets tricky when stock prices bounce around or when convertible securities enter the picture.

The 5% measurement looks through certain entities. If a partnership holds stock, you might need to treat the individual partners as the actual owners. Options, warrants, and convertible debt? Those can be deemed exercised if treating them as exercised would trigger an ownership change—a rule designed to stop companies from gaming the system with derivatives.

Public groups get segmented by transaction. If your company goes public, all the new public shareholders form one public group tied to that IPO. A later equity offering creates a separate public group. This segregation prevents natural market trading from triggering ownership changes, though it adds another layer of tracking complexity.

Author: Marcus Ellwood;

Source: craftydeb.com

Testing Periods and Calculation Methods

That three-year testing period never stops rolling. Picture it like a sliding window—you're always looking back 36 months from any testing date. Frequent equity transactions mean frequent testing requirements, especially for venture-backed startups raising multiple funding rounds.

The section 382 ownership test works by identifying each 5% shareholder's lowest ownership percentage anywhere in that three-year window, then measuring how much they've increased from that low point. Here's a concrete example:

Imagine ABC Corp starts with three founders, each owning 33.33%. Over 18 months, two founders sell out completely to new investors. Each new investor goes from 0% to 33.33%—that's a 33.33-point increase per investor. Total increase: 66.66 percentage points. You've blown past the 50-point threshold, triggering an ownership change.

Now layer in employee stock option exercises, convertible note conversions, preferred stock with liquidation preferences affecting value allocations, and investor rights that might constitute indirect ownership. The calculations spiral into spreadsheet nightmares requiring specialized software.

I've seen companies discover ownership changes years after the fact during M&A due diligence. By then, they've been using NOLs beyond their actual limitation, creating tax liabilities plus interest stretching back to the change date.

Section 382 Limitation Calculation Process

Once you've identified an ownership change, you need to calculate the annual ceiling. The basic formula takes the loss corporation's equity value immediately before the ownership change and multiplies it by something called the "long-term tax-exempt rate."

What the loss company's stock was worth right before the ownership shift

For public companies, recent trading prices; for private companies, typically requires independent appraisal

Higher valuations mean bigger annual limitations—sometimes creates incentive for aggressive valuations

Long-Term Tax-Exempt Rate

Federal rate based on tax-exempt municipal bond yields

IRS publishes this monthly in revenue rulings; recently bouncing between 2.5% and 4% depending on bond market conditions

When rates are higher, your limitation increases; timing the change date by even one month can matter

Built-In Gain Adjustments

Asset appreciation existing at change date but recognized afterward

Requires asset-by-asset appraisal comparing fair market value to tax basis at change date

Each dollar of built-in gain recognized within five years post-change increases that year's limitation by a dollar

Business Continuity Mandate

Company must continue its historical business or use substantial historical assets in a business

Factual examination of what the company actually does for two years after the change

Fail this test and your limitation drops to zero—you lose NOL usage entirely, not just face a cap

Determining equity value requires careful attention. The statute includes anti-stuffing rules that reduce the value if the loss corporation receives a capital contribution as part of the ownership change transaction. You can't just inject cash right before an ownership change to inflate the limitation base.

The long-term tax-exempt rate changes monthly based on municipal bond markets. As I'm writing this in early 2026, the rate hovers around 3.6%. I've seen it below 2% during ultra-low interest rate environments and above 5% when rates spiked. Whatever rate applies in the month of your ownership change locks in for that change's limitation calculation.

Built-in gains create a valuable safety valve. Say your loss company owns a building worth $5 million with a $2 million tax basis at the ownership change date. If you sell that building within five years post-change, the $3 million gain increases your Section 382 limitation for that year dollar-for-dollar. This requires getting professional appraisals at the change date—many companies skip this step and lose the opportunity.

Don't forget about partial-year limitations. If your ownership change happens July 1, you only get half the annual limitation for that year (prorated for the 184 days remaining). The full annual limitation applies in subsequent years.

Author: Marcus Ellwood;

Source: craftydeb.com

Section 382 Impact on NOL Carryforwards and Deductions

The section 382 nol limitation creates a yearly budget for using pre-change losses. If your limitation is $200,000 but you generate $1 million in taxable income post-change, only $200,000 of pre-change NOLs can offset that income. The remaining $800,000 gets taxed currently.

Here's what frustrates taxpayers: unused limitation doesn't carry forward. You can't bank it for future years. If you only generate $100,000 of income in a year when your limitation is $200,000, the unused $100,000 of limitation evaporates. Meanwhile, your NOLs keep aging toward their expiration date.

For NOLs generated before 2018, you're racing against a 20-year expiration clock. The combination of Section 382's annual limitation and the 20-year deadline means companies sometimes watch valuable NOLs expire unused even though the company generated sufficient income—it just couldn't use the NOLs fast enough under the annual cap.

Post-2017 NOLs carry forward indefinitely under the Tax Cuts and Jobs Act. But they face their own restriction: they can only offset 80% of taxable income in any year. When you combine that 80% limitation with Section 382's limitation, the math gets messy. You might have both limitations applying simultaneously, each restricting NOL usage from different angles.

The section 382 impact on deductions extends beyond just NOLs. Companies start playing timing games with income and deductions. You might accelerate income into years when you have unused Section 382 capacity, or defer deductible expenses to preserve your limitation for future income.

Built-in losses—assets that declined in value before the ownership change—face additional restrictions. If your loss company held stock worth $3 million with a $5 million basis at the ownership change, and you sell it for $3 million two years later, that $2 million loss counts against your Section 382 limitation even though it's recognized post-change. The theory is that the economic loss occurred pre-change, so limiting it prevents trafficking in built-in losses just like actual NOL carryforwards.

Section 382 in Mergers and Acquisitions

Section 382 in mergers transforms how deals get priced and structured. Buyers evaluating targets with NOL carryforwards need to model out whether the post-acquisition limitation justifies paying extra for those tax attributes.

In a stock acquisition, the target continues existing as a legal entity. Any ownership change triggers Section 382, with the limitation based on the target's pre-deal value. Here's the rub: if the target is distressed, its value might be a fraction of its NOL carryforwards, creating a tiny limitation that makes the NOLs nearly worthless.

I worked on a deal where the target had $15 million in NOLs but was worth only $3 million due to operational struggles. With the long-term tax-exempt rate at 3.5%, the annual limitation came to $105,000. At that rate, it would take over 140 years to use the NOLs—far beyond their 20-year expiration. The buyer essentially ignored the NOLs in valuation.

Asset acquisitions sidestep Section 382 entirely because the buyer doesn't inherit the target's tax attributes—they stay with the target corporation. Of course, that means the NOLs are lost unless the target continues operating. Some deals structure the target as an ongoing subsidiary to preserve NOLs, but that complicates post-merger integration.

Merger structures present the trickiest scenarios. In a forward merger where the target merges into the buyer, the target's NOLs transfer to the surviving buyer but face Section 382 limits based on the target's pre-merger value. Reverse mergers—where the buyer merges into the target—leave the target as the survivor, but the ownership change still typically occurs.

Tax-free reorganizations under Section 368 can qualify for tax deferral while still triggering Section 382 limitations. The tax-free treatment and the NOL limitations operate independently. You might accomplish a tax-free stock-for-stock reorganization for your shareholders while simultaneously hitting a Section 382 ownership change that limits NOL usage going forward.

Private equity deals deserve special mention. When a PE fund acquires a portfolio company, the fund's investors are looked through for Section 382 purposes. If the fund later admits new investors or existing investors change their fund commitments, those changes can trigger another ownership change at the portfolio company level—imposing a second Section 382 limitation on top of the one from the original acquisition.

Section 382 turns NOLs from straightforward tax assets into time bombs requiring constant vigilance. I've seen sophisticated private equity firms lose track of ownership changes at the fund level, only discovering during exit that they've been overclaiming NOL deductions for years

— Jennifer Morrison

Common Section 382 Mistakes and How to Avoid Them

The biggest mistake? Not tracking ownership changes in the first place. Plenty of private companies lack any system to monitor stock transfers, especially transfers happening between shareholders without company involvement. By the time someone notices the problem—often during a sale or IPO—years have passed and NOLs have been used beyond the allowable limitation.

Set up a mandatory policy: every stock transfer requires board approval, with Section 382 analysis completed before approval. For public companies, coordinate with your transfer agent to flag when investors approach 5% ownership thresholds. Monitor SEC Schedule 13D and 13G filings religiously.

Misunderstanding the testing period creates expensive errors. Companies test only at year-end, missing mid-year ownership changes. If an ownership change happens in March but you don't identify it until December, you may have already used NOLs exceeding the prorated limitation for that year. You'll owe tax on the excess plus interest and potential penalties.

The continuity of business requirement gets overlooked entirely by some companies. Section 382 doesn't just limit your NOL usage—it can eliminate it completely if you fail to continue the historic business or use significant historic assets in a business for two years post-change.

What constitutes business continuity? The rules apply a flexible facts-and-circumstances test. Staying in the same general industry usually works, even with operational modifications. Liquidating all your assets and entering an unrelated field? That fails. Acquiring a tech company and pivoting it into real estate development would likely blow the continuity test.

Document your continuity analysis when the ownership change occurs. Don't wait until the IRS questions your NOL usage three years later to develop your explanation of why you maintained business continuity.

Options and convertible securities trip up many companies. The statute includes complex rules about when these instruments are treated as exercised for ownership testing. Some companies ignore outstanding options completely in their calculations, then discover the IRS treats them as exercised, which pushed the ownership change date earlier than the company recognized.

Failing to get valuations at the ownership change date costs companies real money. While you generally prefer lower valuations for tax purposes, Section 382 flips the incentive—higher valuations produce larger annual limitations. If you don't obtain an independent appraisal to support the value used in your limitation calculation, you might default to book value or some other number that understates the actual fair market value, leaving money on the table.

Author: Marcus Ellwood;

Source: craftydeb.com

Frequently Asked Questions About Section 382

What triggers a Section 382 ownership change?

You hit an ownership change when shareholders who own at least 5% of the company (measured individually or as groups) collectively increase their ownership by more than 50 percentage points during any three-year period. This can result from stock sales between existing shareholders, new stock issuances, redemptions, or even natural shifts in public company shareholder bases. The test aggregates smaller shareholders into public groups, so you're tracking 5%+ holders specifically. Stock options can be treated as exercised if doing so would trigger a change.

How is the Section 382 limitation calculated?

You take the loss corporation's fair market value immediately before the ownership change and multiply it by the long-term tax-exempt rate (a federal rate the IRS publishes monthly, currently around 3.6%). So a company worth $8 million going through an ownership change when the rate is 3.6% faces a $288,000 annual limitation. That's the maximum pre-change NOL that can offset post-change income each year. Built-in gains recognized within five years can increase the limitation. The limitation gets prorated for partial years.

Can Section 382 limitations ever be avoided?

Not once an ownership change occurs—the limitation is mandatory. But you can structure transactions to prevent or delay ownership changes in the first place. Strategies include limiting new equity issuances, using debt instead of equity financing, implementing shareholder rights plans that restrict accumulation, carefully spacing transactions to stay under the 50-point threshold, and timing equity raises to push testing dates beyond the three-year window for older transactions. Business needs typically override Section 382 planning, but thoughtful deal structuring can preserve NOL usage.

What is the long-term tax-exempt rate in Section 382?

This rate reflects the average market yield on long-term tax-exempt bonds, published monthly by the IRS in revenue rulings. It typically ranges from 2% to 5% depending on overall interest rate environments. Right now in early 2026, it's running around 3.6%. The rate from the month your ownership change occurs determines your limitation calculation and stays fixed for that change—even if rates later increase or decrease. A one-point difference in the rate can mean hundreds of thousands of dollars in annual limitation for larger companies.

How does Section 382 affect bankruptcy reorganizations?

Bankruptcy creates special rules under Section 382(l)(5) and (l)(6). The Section 382(l)(5) election lets shareholders and qualifying creditors receive stock in the reorganization without triggering an ownership change, but requires reducing NOLs by interest deductions from the prior three years plus the bankruptcy year—often a substantial haircut. Section 382(l)(6) alternatively allows using the company's stock value immediately after emerging from bankruptcy for the limitation calculation, which may be higher than the distressed pre-bankruptcy value but still triggers the annual limitation. Most companies choose whichever approach preserves more NOL value.

What records must companies maintain for Section 382 compliance?

You need detailed cap tables showing every shareholder's ownership percentage at all times, documentation of every stock transfer with dates and parties involved, board resolutions approving transfers, valuations supporting fair market value at potential ownership change dates, calculations proving you stayed within annual limitations each year, and evidence documenting business continuity after ownership changes. Public companies should retain SEC filings and transfer agent reports. Private companies need stock purchase agreements, option exercise notices, and contemporaneous ownership spreadsheets. Keep everything throughout the NOL carryforward period plus at least three years after you use up the last NOL.

Section 382 accomplishes what Congress intended: it stops profitable businesses from buying tax losses to eliminate their tax bills. But the compliance burden is substantial, and the consequences of errors can be severe.

The annual limitation mechanism ties NOL usage to the loss corporation's actual economic value at the ownership change moment. This prevents the worst tax loss trafficking abuses while allowing legitimate businesses to carry their own losses forward through ownership transitions.

Navigating Section 382 successfully requires proactive planning, not reactive scrambling. You need to spot potential ownership changes before they happen, model the limitation's effect on NOL utilization, and structure transactions to maximize tax benefits while achieving business goals.

Companies should implement ownership tracking systems before they need them. By the time you're in the middle of a transaction, it's too late to establish the monitoring infrastructure that would have prevented the problem. This means cap table management software, board policies requiring approval of transfers, and regular Section 382 testing—at minimum quarterly, preferably whenever equity transactions occur.

Given the complexity and the dollars at stake, bringing in experienced tax counsel for significant equity transactions isn't optional. I've seen too many companies lose millions in NOL value because they didn't involve Section 382 specialists until after closing, when they discovered an ownership change had occurred with a limitation far below what basic planning could have preserved. The cost of good advice upfront is always cheaper than the cost of fixing problems years later when the IRS starts asking questions.

UCC stands for the Uniform Commercial Code, a comprehensive set of laws governing commercial transactions across the United States. For business owners, attorneys, and anyone involved in buying or selling goods, understanding the UCC is essential to structuring enforceable agreements and avoiding costly disputes

Transactional law encompasses the legal work involved in business deals and commercial arrangements. Unlike litigation attorneys who resolve disputes in court, transactional lawyers structure transactions, draft agreements, and prevent legal problems before they arise

Personal liability means you can be held financially responsible for business debts and lawsuits using your own assets. Understanding when protection applies, how corporate structures shield personal wealth, and where vulnerabilities exist helps you make informed decisions safeguarding your financial future

US businesses hiring foreign contractors face complex IRS compliance requirements. This guide explains tax withholding rules, required forms like W-8BEN and 1042-S, payment methods, treaty benefits, and step-by-step processes to avoid penalties when paying overseas freelancers legally

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to business and corporate law, contracts, compliance, disputes, M&A, and taxation for companies.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Legal outcomes may vary depending on jurisdiction, company structure, and individual circumstances.

This website does not provide legal advice, and the information presented should not be used as a substitute for consultation with qualified corporate attorneys or legal professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.