If you run a business, you've probably wondered whether last year's tax return could come back to haunt you—or maybe one from five years ago. Here's the reality: the IRS can't chase your old returns forever. Federal law sets clear boundaries on how long they can reach back, though those limits shift dramatically depending on what's actually on your return.

In most cases, you're looking at a three-year window. File your return today, and three years from now, that return becomes untouchable. But substantial errors change the equation entirely. Leave out a quarter of your income? That window doubles to six years. Commit fraud? The calendar stops mattering altogether.

The type of business you operate also plays a role. Sole proprietors, partnerships, S corporations, and C corporations all face the same basic time limits, but the IRS applies different examination procedures to each structure. Understanding where your business falls—and which mistakes extend the audit clock—helps you keep the right records for the right amount of time.

Standard IRS Audit Lookback Periods for Businesses

Here's the baseline: the IRS gets three years from your filing date to start examining your business tax return. This irs three year audit limit covers most businesses that report their income accurately and file proper returns.

The starting point isn't always obvious. Say you finish your 2025 corporate return early and submit it March 1, 2026—two weeks before the March 15 deadline. You might assume the three-year countdown begins March 1. It doesn't. The tax return audit period starts March 15, the actual due date. Filing ahead of schedule gives the IRS extra time, not less.

This applies only when you file something the IRS considers a legitimate return. Slapping your business name on a blank form won't cut it. The return needs sufficient information for the IRS to calculate what you owe. Missing that threshold means the clock never starts running.

How many years irs can audit also depends on when they make contact. They don't need to finish the entire examination within three years—just send you an audit notice before the deadline passes. Initial contact is what counts.

Picture this scenario: You submit your 2023 business return April 15, 2024. The IRS has until April 15, 2027, to reach out. If an audit letter arrives April 10, 2027, they've made the cutoff. The actual audit might drag on another eighteen months, but they got their foot in the door on time.

Author: Marcus Ellwood;

Source: craftydeb.com

When the IRS Can Audit Six Years Back

The irs six year audit rule activates when you omit substantial income from your business return. "Substantial" isn't subjective—it means leaving out more than 25% of the gross income you reported.

The math works like this: Report $200,000 in gross receipts when you actually brought in $300,000, and you've hidden $100,000. That's 50% of what you disclosed, well past the 25% trigger. Your audit window just stretched from three years to six.

Several situations beyond simple underreporting extend the irs business audit period to six years:

Foreign income and assets: Fail to report foreign income exceeding $5,000, and you face six years of exposure. The 25% threshold doesn't even enter the equation for international income.

Overstated basis: Inflate what you paid for property to reduce your gain when selling it, and if that overstatement exceeds 25% of the correct basis, the six-year rule applies.

Related-party international transactions: Businesses dealing with foreign affiliates often trigger extended scrutiny under transfer pricing rules, subjecting them to the longer examination period.

The 25% calculation uses gross income—not your taxable income after deductions. A catering company reporting $500,000 in revenue that actually earned $700,000 crosses the threshold. That $200,000 gap exceeds 25% of the $500,000 reported, regardless of what deductions would have reduced the final tax bill.

Watch out for this trap: inflating your cost of goods sold can backfire. When you pump up COGS to shrink gross receipts, you're effectively hiding gross income. The IRS treats this as meeting the 25% omission trigger.

Situations with No Statute of Limitations

Three circumstances erase the irs audit statute of limitations entirely. The IRS can dig into these returns twenty years later if they want.

Fraudulent returns: File a return designed to dodge taxes—keeping two sets of books, fabricating expenses, burying income streams—and the statute never closes. The IRS must prove you acted deliberately, not just carelessly. Clear and convincing evidence of intentional wrongdoing is required. Sloppy bookkeeping doesn't qualify as fraud.

Unfiled returns: Don't file a required business return, and the examination window never opens because it never starts. This covers businesses operating under the table, not situations where you mailed a return the IRS claims it never received.

Willful evasion: Beyond filing a false return, actively dodging tax through elaborate schemes keeps your returns permanently exposed. Offshore account manipulation, using nominees to conceal ownership, or creating shell companies to hide income all fall here.

When does irs audit expire in these cases? It doesn't. The IRS has successfully examined returns from the 1990s when they uncovered fraud schemes.

Here's a lesser-known issue: file a return without signing it, and some courts say it doesn't count as valid. The statute might not start until you submit a properly signed version. Electronic signatures on e-filed returns satisfy this requirement, so digital filing avoids the problem.

The IRS carries the burden of proving fraud or willful evasion. They can't simply declare your statute is unlimited without evidence. They need documents, witnesses, or patterns demonstrating intentional misconduct.

How Business Structure Affects Audit Periods

Your entity type shapes both your tax treatment and how irs audit years business work. Different structures face distinct examination procedures.

Sole proprietors report business income on Schedule C attached to Form 1040. The audit period for the entire return—business activity included—follows individual return rules. Three years for clean returns, six for substantial understatement, unlimited for fraud.

Pass-Through Entities and Partnership Audits

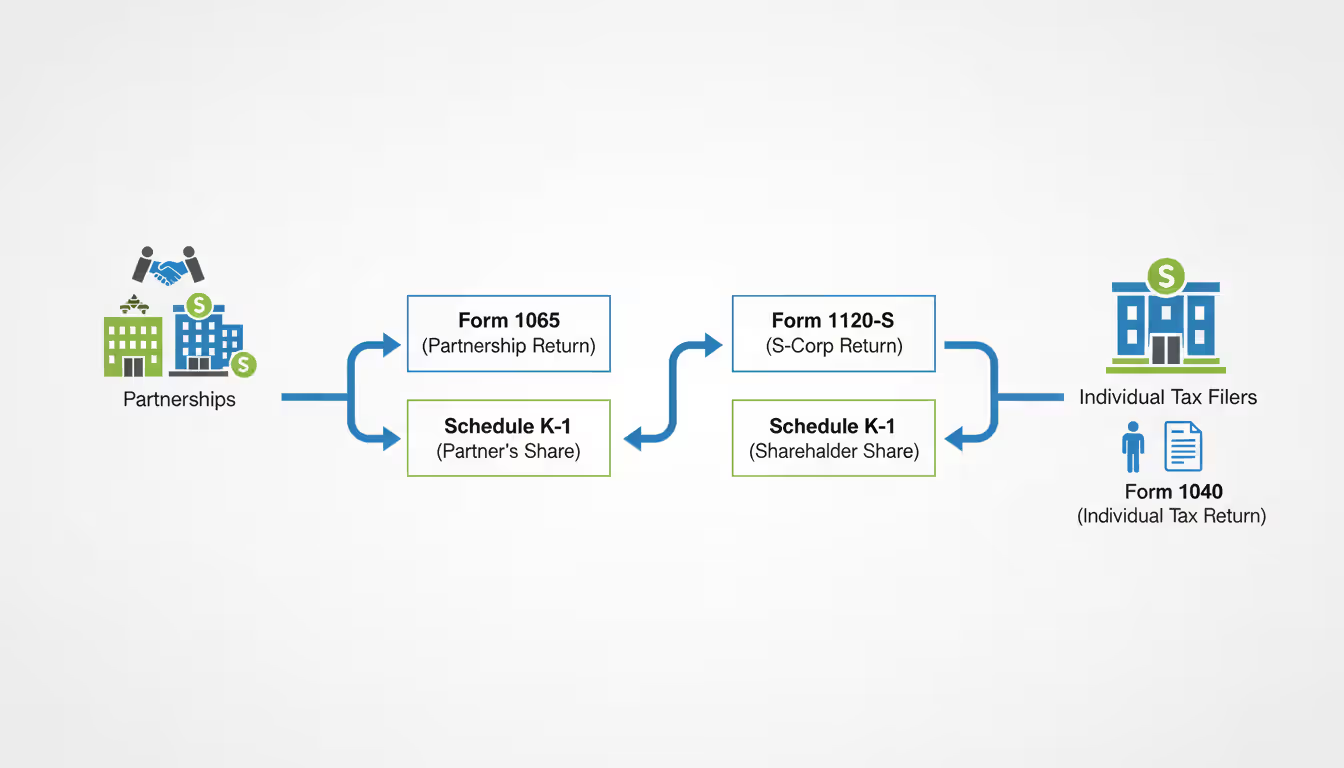

Partnerships, S corporations, and multi-member LLCs taxed as partnerships operate under special rules following the Bipartisan Budget Act of 2015. The business tax audit timeline for these entities has two layers.

The entity-level examination reviews the partnership or S-corp return itself. The IRS can adjust items at the entity level, and the statute runs from when the entity filed. Partnerships file Form 1065; S-corps file Form 1120-S.

Under centralized partnership audit rules, the IRS typically assesses tax at the entity level instead of adjusting each partner's individual return separately. Current-year partners end up paying tax on adjustments from prior years—even if they weren't partners when the audited return was originally filed.

The business entity gets the same three-year window from filing for the IRS to initiate a partnership audit. The six-year and unlimited exceptions apply identically. But when a partnership skips filing a required return or files a fraudulent one, each partner's individual statute stays open for those items.

S corporations follow parallel rules. The IRS examines the 1120-S and makes adjustments that flow through to shareholders. The corporate-level statute controls when the IRS can audit, though shareholder returns may face separate examination for items unrelated to the S-corp.

Author: Marcus Ellwood;

Source: craftydeb.com

Corporate Tax Return Audit Timelines

C corporations file Form 1120 and face the same basic three-year statute. The corporate entity stands as the taxpayer, separate from shareholders, so the audit period runs independently from owner returns.

One wrinkle: when the IRS audits a C corporation and discovers unreported income, they may also examine whether distributions to shareholders should be reclassified as dividends. This can trigger separate examinations of shareholder individual returns within their own statute periods.

Closing a corporation doesn't shorten audit periods. Dissolve your corporation tomorrow, and the IRS still gets the full statute of limitations to audit returns filed before dissolution. Successor liability rules may even let them pursue shareholders or acquiring entities for unpaid corporate tax.

What Starts and Stops the IRS Audit Clock

The irs audit lookback period begins when you file a valid return, but various actions can pause, restart, or extend the deadline.

Filing date versus due date: The statute starts on whichever comes later—your actual filing or the official due date. File a 2025 corporate return January 15, 2026, before the March 15 deadline, and the statute begins March 15, 2026. Early filing gives you nothing.

Extensions to file: Request a filing extension, and you push both the due date and the statute start date forward. Extend your 2025 partnership return from March 15 to September 15, 2026, then file September 1, and the statute begins September 15, 2026.

Amended returns: Filing an amended business return—Form 1120-X for corporations, amended 1040 for sole proprietors, or amended partnership returns—doesn't restart the original three-year period. However, it can extend the statute for items you modified. The IRS gets whichever is later: three years from the original return or two years from when you paid the tax due on the amendment.

Consent to extend (Form 872): The IRS frequently asks businesses to sign Form 872, extending the irs audit statute of limitations. This happens when an audit is complicated and won't wrap up before the statute expires. You can refuse, though the IRS may then rush to assess tax based on whatever information they have. Most businesses agree to reasonable extensions allowing thorough examination.

Bankruptcy: Filing for bankruptcy automatically halts IRS collection activity and suspends the assessment statute. The suspension lasts throughout the bankruptcy plus six months afterward.

Tax Court petitions: Petition Tax Court to dispute an IRS determination, and the assessment period suspends while the case proceeds, plus 60 days after the court decides.

Innocent spouse claims: When a business owner files an innocent spouse claim related to joint returns that included business income, this can extend statutes for examining the business activity.

Here's a practical timeline: Your LLC files its 2023 return March 15, 2024. The normal statute expires March 15, 2027. The IRS starts an audit January 2027 and asks you to sign Form 872 extending through December 31, 2027. You agree. They propose adjustments November 2027. You get until February 2028 (90 days) to petition Tax Court. Petition, and the statute suspends again until the case resolves.

Author: Marcus Ellwood;

Source: craftydeb.com

How to Protect Your Business from Extended Audits

Understanding the business tax audit timeline enables you to implement protective measures. The IRS suggests keeping records at least three years, but experienced business owners hold onto documentation much longer.

Maintain records for six years minimum: Even when you file accurate returns, the six-year rule for substantial understatement means you should preserve all supporting documents—receipts, invoices, bank statements, depreciation schedules—at least six years. Seven years provides a cushion.

Keep certain items permanently: Corporate formation documents, partnership agreements, asset purchase records, and property basis documentation should never get tossed. You'll need these to calculate gain or loss when selling assets or dissolving the business, no matter how many years pass.

Document international transactions meticulously: Any business with cross-border activities faces heightened scrutiny and extended statutes. Keep detailed records of foreign income, transfer pricing studies, and foreign bank account reports (FBARs) at least seven years.

Answer IRS notices promptly: When the IRS sends an audit notice, the clock is already running. Delayed responses won't extend the statute in your favor, and they complicate your ability to gather evidence and present your case.

Bring in professional representation early: Tax attorneys and CPAs specializing in IRS audits understand how statutes work and can negotiate extensions strategically. They also spot when the IRS operates outside the statute of limitations—a defense requiring precise calculation of filing dates and extension agreements.

Scrutinize Form 872 before signing: Don't reflexively agree to extend the statute. Evaluate whether you genuinely need more time to compile records or whether the IRS is simply fishing. Sometimes refusing an extension forces the IRS to decide with available information, which may work in your favor.

Organize digital records: Cloud-based accounting systems create automatic audit trails and simplify producing documentation years later. Organized records also reduce the time and expense of responding to audits.

Business owners consistently underestimate the importance of documentation retention beyond the three-year minimum.I've seen profitable businesses face substantial tax bills because they discarded records after three years, not realizing the six-year rule applied to their situation. The cost of maintaining organized records for seven years is negligible compared to the exposure from an extended audit where you can't substantiate legitimate deductions

— Jennifer Martinez

Frequently Asked Questions About IRS Business Audits

Can the IRS audit a business after 10 years?

Usually no, barring specific exceptions. For standard returns without substantial understatement, the three-year statute means audits happening in 2037 for a 2026 return are prohibited. But file a fraudulent return, never file at all, or substantially understate income by more than 25%, and the IRS can audit well past the 10-year mark. Fraud cases carry no time limit whatsoever.

Does the three-year rule apply to all business types?

Yes, the basic three-year statute covers sole proprietorships, partnerships, S corporations, C corporations, and LLCs regardless of tax classification. The difference is which return the IRS examines—Schedule C for sole proprietors, Form 1065 for partnerships, Form 1120-S for S-corps, and Form 1120 for C-corps. Examination procedures vary by entity type, but the fundamental three-year period remains consistent across structures.

What happens if I amend my business tax return?

Amending doesn't restart the original three-year statute from your initial filing. The IRS does get additional time to examine items you modified on the amendment. They receive whichever is later: three years from the original return or two years from when you paid any extra tax shown on the amended return. If your amendment reduces tax, the original statute still controls for items you left unchanged.

How long should I keep business tax records?

Maintain records at least six years to cover the extended statute for substantial understatement. Seven years offers extra protection. Preserve documents proving asset basis, formation agreements, and major transactions indefinitely since you'll need them for future calculations. Employment tax records warrant at least four years of retention. File returns involving fraud or skip required filings entirely, and you should keep records permanently since the statute never expires.

Can the IRS extend the audit period?

The IRS cannot unilaterally extend the statute of limitations. They require your agreement through Form 872 (Consent to Extend the Time to Assess Tax). You're not obligated to agree, though refusing may prompt the IRS to assess tax quickly based on incomplete information. Extensions are routine when audits are complex. You can negotiate the extension length and limit it to specific tax issues rather than agreeing to an unlimited extension.

What triggers a six-year lookback instead of three?

The most frequent trigger is omitting more than 25% of gross income reported on your return. This includes underreporting revenue, failing to report entire income streams, or overstating cost of goods sold to reduce gross receipts. Unreported foreign income exceeding $5,000 also triggers six years even without meeting the 25% threshold. Substantially overstating basis in property (by more than 25%) extends the statute as well. The six-year period applies to the entire return, not just the understated items.

Most businesses face a three-year audit window from filing, though this baseline stretches to six years when you substantially understate income and stays open forever for fraud or unfiled returns. Your business structure determines which forms the IRS examines and how partnership or corporate-level adjustments flow through to owners.

The statute of limitations shields businesses from endless audit risk, provided you file complete, accurate returns and preserve supporting documentation. Minor understatements or honest errors rarely trigger extended periods, while deliberate omissions or fraud eliminate time limits entirely.

Experienced business owners preserve records at least six years, understand what triggers extended examination periods, and consult tax professionals when facing audit notices. The statute runs from your filing date or the return due date—whichever occurs later—and various actions like filing amendments or agreeing to extensions can modify these deadlines.

Knowing these rules lets you plan document retention, assess audit risk, and respond appropriately when the IRS makes contact. The clock usually ticks in your favor, counting down to when old returns become immune from examination. Make sure your business practices and record-keeping support that timeline rather than working against it.

UCC stands for the Uniform Commercial Code, a comprehensive set of laws governing commercial transactions across the United States. For business owners, attorneys, and anyone involved in buying or selling goods, understanding the UCC is essential to structuring enforceable agreements and avoiding costly disputes

Transactional law encompasses the legal work involved in business deals and commercial arrangements. Unlike litigation attorneys who resolve disputes in court, transactional lawyers structure transactions, draft agreements, and prevent legal problems before they arise

Section 382 limits NOL carryforwards after ownership changes to prevent tax loss trafficking. Learn how ownership tests work, limitation calculations, and compliance requirements for M&A transactions

Personal liability means you can be held financially responsible for business debts and lawsuits using your own assets. Understanding when protection applies, how corporate structures shield personal wealth, and where vulnerabilities exist helps you make informed decisions safeguarding your financial future

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to business and corporate law, contracts, compliance, disputes, M&A, and taxation for companies.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Legal outcomes may vary depending on jurisdiction, company structure, and individual circumstances.

This website does not provide legal advice, and the information presented should not be used as a substitute for consultation with qualified corporate attorneys or legal professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.