Here's what most business owners want to know: what's the magic number? How much can I pay a freelancer, contractor, or consultant before I'm stuck dealing with tax forms?

The number you're looking for is $600. Pay someone $599.99 for business services throughout the year, and you're in the clear—no Form 1099 needed. Hit exactly $600, and the IRS wants paperwork.

But here's where it gets tricky. That $600 threshold doesn't apply to everyone. The person's business structure matters. How you paid them matters. What you paid them for definitely matters. I've seen business owners confidently skip filing 1099s because they thought the corporate exemption applied, only to get hit with penalties later. I've also seen people waste hours preparing forms for payments that never needed reporting in the first place.

Let's clear up the confusion so you can stay compliant without overthinking every contractor payment.

What Is the 1099 Reporting Threshold for 2026

For 2026, the magic number hasn't changed: $600 or more in total payments during the calendar year triggers reporting requirements for most business payments to contractors.

Notice I said "total payments"—not per invoice or per project. If you hire a photographer who bills you $200 in March, $150 in July, and $300 in November, you've hit $650 total. You'll need to issue a 1099 even though no single payment reached $600.

Two distinct forms handle different payment categories. The IRS brought back Form 1099-NEC in 2020 after a 37-year hiatus, and it's now the primary form for contractor payments.

Form 1099-NEC handles payments for services. Think freelancers, consultants, virtual assistants, bookkeepers, web developers, copywriters—anyone providing professional services to your business as a non-employee. Did you pay a marketing consultant $3,200 to overhaul your social media strategy? That goes on a 1099-NEC.

Form 1099-MISC covers everything else that hits the threshold. Rent payments to a landlord, award prizes at your company event, royalties to content creators, medical payments—these belong on the MISC version. The threshold stays at $600 for most categories, though royalties drop to just $10 (yes, ten dollars).

Here's a distinction that trips people up: the $600 applies to each separate payee, not your total contractor spending. Pay 10 different contractors $500 each? None require a 1099. Pay one contractor $5,000? Definitely requires a 1099.

The calendar year matters more than you'd think. Payments count based on when money leaves your account, not when services were performed. A contractor completes a project December 15, 2026, but you don't pay until January 5, 2027? That payment counts toward your 2027 reporting, not 2026.

Some business owners try to game the system by keeping payments just under $600 per contractor. The IRS isn't fooled. If they audit you and find you've artificially split work among multiple "contractors" who are really the same person or entity, you're looking at penalties plus potential fraud charges.

Who Gets a 1099 Form and Who Doesn't

The recipient's legal structure determines everything. This is why you'll see tax professionals obsess over collecting W-9 forms before paying anyone—that form tells you exactly what you're dealing with.

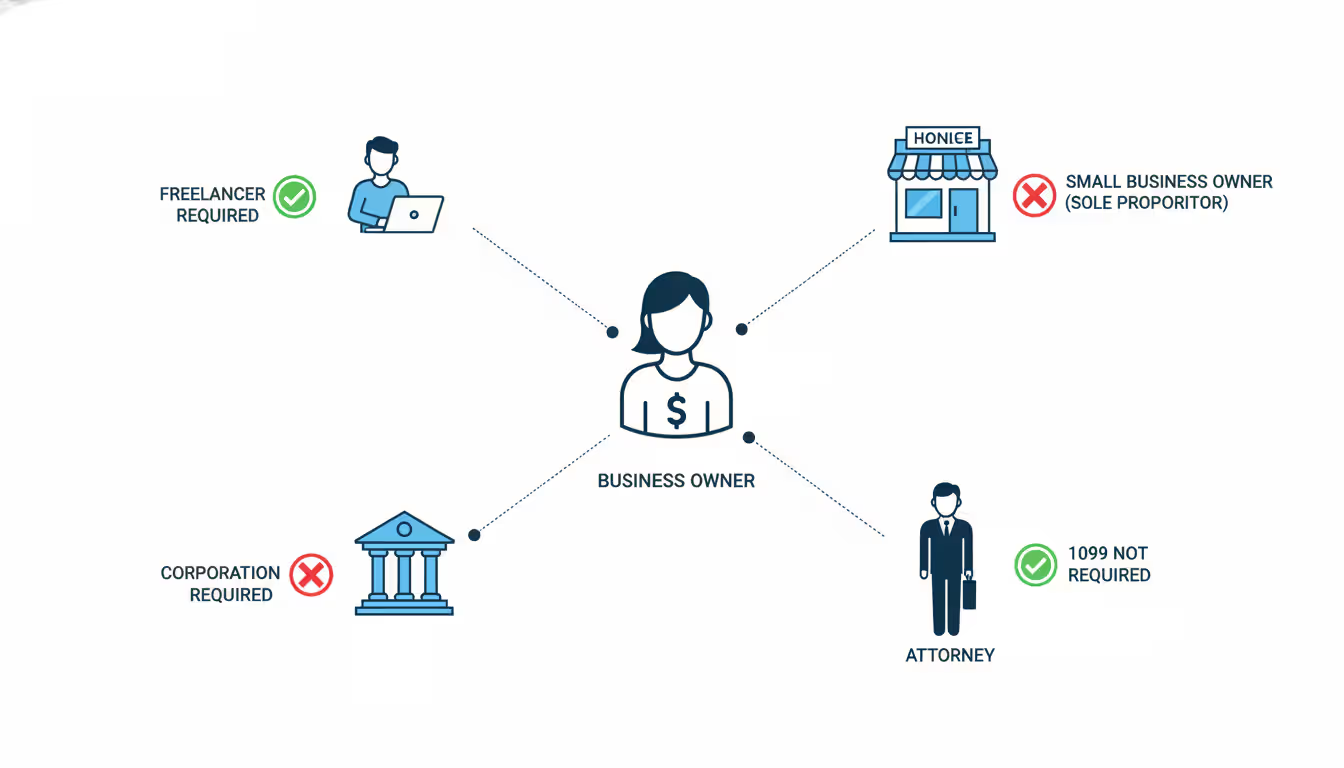

You're definitely issuing a 1099 to: - Self-employed individuals operating under their own name - Sole proprietorships (including DBAs) - Single-member LLCs that haven't elected special tax treatment - Partnerships of any size - Multi-member LLCs operating as partnerships

You're skipping the 1099 for: - Incorporated businesses (both C-corps and S-corps) - Anyone you paid exclusively through credit cards or PayPal - Merchandise suppliers (you're buying products, not services) - Your actual employees (they get W-2s instead) - Anyone you paid for purely personal, non-business reasons

Author: Olivia Farnsworth;

Source: craftydeb.com

The corporate exemption causes endless confusion. Let's say you paid "Johnson Marketing Services" $4,500 last year. Do you file a 1099? Impossible to answer without knowing their structure. Is Johnson Marketing Services a sole proprietorship? File a 1099. An S-corp? Skip it. An LLC? Depends on how they elected to be taxed.

This is exactly why the W-9 matters so much. Box 3 on that form shows the federal tax classification. An LLC can check "single-member LLC," "multi-member LLC," "C corporation," "S corporation," or "partnership." Each choice triggers different reporting requirements for you.

Attorney payments break all the normal rules. Even if you hire a massive law firm structured as a professional corporation, you still file a 1099 once payments hit $600. The IRS carved out this exception because they really, really want visibility into legal fee payments. Every law firm knows this, so they'll provide their tax info without hesitation.

Payment method creates another layer of exemptions. When you swipe your business credit card to pay a $2,000 contractor invoice, you don't file a 1099. Why? Because your credit card company reports that transaction to the IRS on Form 1099-K. Same with PayPal, Venmo, or any third-party payment processor. The IRS only wants one entity reporting each transaction—either you or the payment processor, never both.

But here's the catch: this only exempts the specific payments made through those channels. Pay a contractor $1,200 total last year—$700 by check and $500 through PayPal? You still file a 1099 reporting the $700 in check payments.

When to Issue a 1099 to Contractors and Service Providers

Deadlines aren't flexible, and the IRS doesn't care about your busy schedule or that your bookkeeper quit in December.

For any payments made during 2026, recipients must have their copies by January 31, 2027. Not postmarked by January 31—received by January 31. If you mail forms on January 29 and they arrive February 2, you're technically late.

Your deadline for filing with the IRS depends on format. Paper filers must submit by February 28, 2027. E-filing extends your deadline to March 31, 2027. The IRS strongly prefers electronic filing (and requires it if you're filing 10 or more forms), so that extra month often makes e-filing worth the setup.

Only business payments count. I can't stress this enough because I've seen people waste time reporting personal payments. Hired a teenager to mow your personal lawn all summer and paid them $800? No 1099—that's personal. Hired that same teenager to mow the lawn at your office building? Now it's a business expense requiring a 1099.

Let's walk through real scenarios:

January through December retainer payments. Your virtual assistant charges $450 monthly. January's payment alone doesn't trigger anything. But by March you've paid $1,350 cumulative, so you know you'll be filing a 1099 at year-end. The form reports the annual total—in this case, $5,400 if payments continued all year.

One-off project payment. You hire a consultant for a pricing strategy project. Single payment of $6,500. Easy—one payment, well above threshold, 1099 required.

Sporadic small payments adding up. This is where businesses mess up most often. A freelance editor does four projects: $175 in February, $220 in May, $140 in August, $80 in November. No single payment looks reportable, but the total is $615. You're filing a 1099.

Mixed payment methods. Your bookkeeper gets paid $400 monthly. Six months you paid by check, six months by credit card. You only report the $2,400 in check payments on the 1099 because the credit card company handles the other $2,400.

Prepayments. In December 2026, you prepay a contractor $1,500 for work they'll perform in January 2027. That $1,500 goes on your 2026 Form 1099 because money changed hands in 2026, regardless of when services occur.

What Happens If You Don't Issue a Required 1099

The penalty structure isn't designed to be friendly. It's designed to motivate compliance.

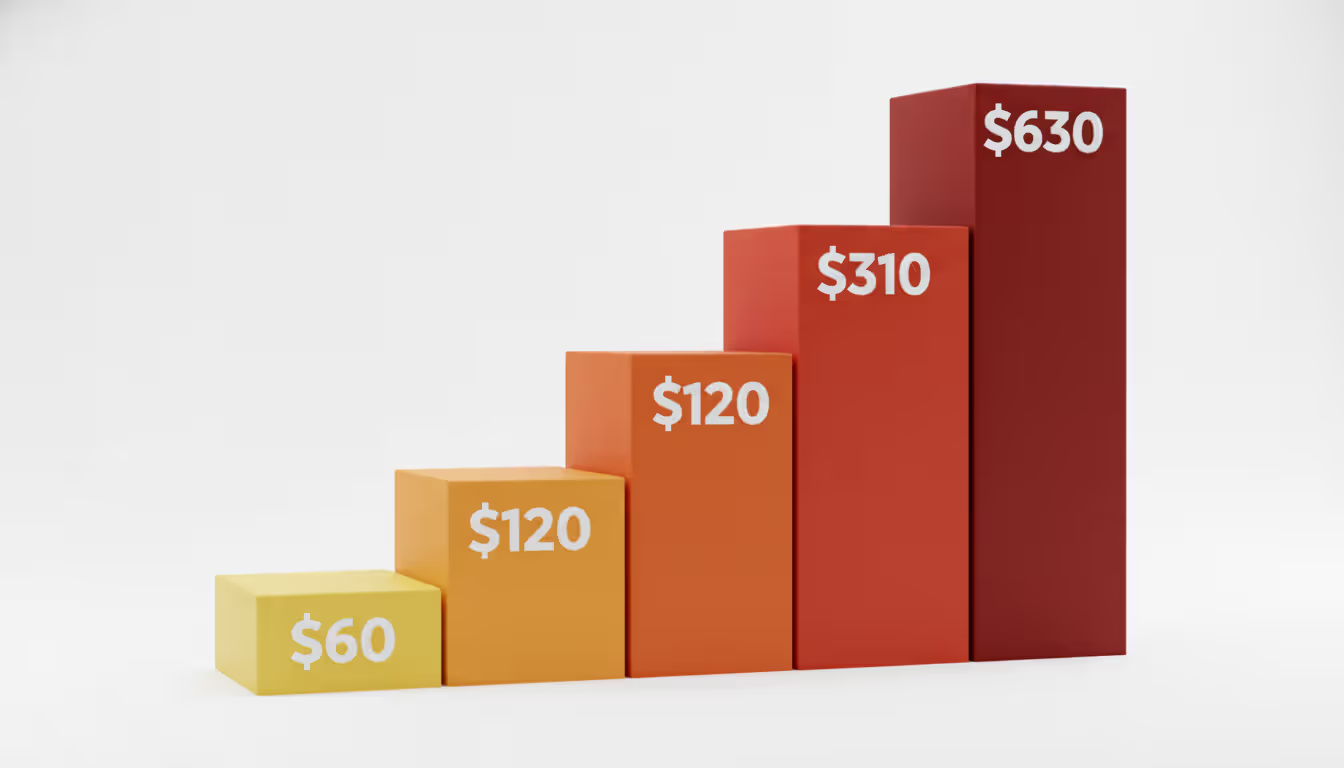

Current IRS penalties work on a sliding scale based on how late you file:

File up to 30 days late: $60 per form

File 31 days late through August 1: $120 per form

File after August 1 or never file: $310 per form

Intentional disregard of filing requirements: $630 per form

Author: Olivia Farnsworth;

Source: craftydeb.com

Small business? There's a slight break. If your average annual gross receipts are $5 million or less over the past three years, your maximum annual penalty caps at $630,000. Larger businesses face caps exceeding $3.7 million.

Let's make this concrete. You paid 15 contractors last year, all requiring 1099s, and you completely forgot about filing. By the time you realize the mistake in September, you're looking at $310 × 15 = $4,650 in penalties. For comparison, hiring a service to prepare and file those 15 forms would've cost maybe $150.

How does the IRS even find out? Three main ways:

Income matching. Contractors report their total income on Schedule C when filing personal returns. The IRS runs automated matching programs. When a contractor reports receiving $8,000 from your business but the IRS has no 1099 on file from you, the system flags it. You'll get a notice.

Audit discovery. During an audit, examiners request your general ledger and expense documentation. They scan for payments to individuals and non-corporate entities. Found a $5,000 payment to "Sarah Johnson Designs" with no corresponding 1099 on file? That's a penalty, plus potential expanded audit scope.

Third-party reports. Sometimes contractors proactively contact the IRS when they don't receive expected 1099s, especially if they're concerned about income matching issues on their own returns.

Here's what business owners misunderstand: even if you never filed a 1099, the contractor still owes taxes on that income. The 1099 is just an information report. It doesn't create the tax liability—the income itself does. But contractors who don't receive 1099s sometimes (illegally) underreport their income, which is precisely why the IRS enforces these rules aggressively.

Can you escape penalties? Maybe, if you've got "reasonable cause." This requires demonstrating a good-faith effort to comply that failed due to circumstances genuinely beyond your control. A fire that destroyed your records the week before the deadline might qualify. Simply being busy or unaware of the rules won't cut it—the IRS publishes the requirements publicly, so ignorance isn't reasonable cause.

How to Track and Report Contractor Payments Correctly

Systems prevent panic. Here's what actually works:

Get the W-9 before issuing the first payment. Not after. Not "I'll grab it next time." Before. Make this non-negotiable. No W-9, no payment. Period.

Why the hard line? That W-9 gives you the contractor's legal name as registered with the IRS, their current mailing address, their taxpayer identification number (either SSN or EIN), and—critically—their tax classification. Without these details, you can't accurately complete a 1099. Plus, if you skip the W-9 and the contractor's info later proves incorrect, you're liable for penalties even though it was their mistake.

Author: Olivia Farnsworth;

Source: craftydeb.com

What if someone refuses? You're required to start backup withholding. Hold back 24% of every payment and send it to the IRS. Pay someone $1,000? They get $760, and you remit $240 to the IRS using Form 945. Most contractors provide the W-9 immediately once you explain backup withholding.

Track every contractor payment as it happens. Your accounting software probably categorizes contractor payments automatically if you set it up right. QuickBooks, Xero, FreshBooks—all have contractor tracking features. If you're old-school with spreadsheets, fine, but update it with each payment, not once a quarter.

Record these details minimum: payment date, payee name exactly as shown on W-9, amount, payment method, description of services. Takes 30 seconds per entry, saves hours in January.

Separate payment methods matter. Create distinct categories for payments made by check or ACH versus credit card or PayPal. Only the first category requires 1099s from you. When you run your year-end report, you want to instantly see which payments you're responsible for reporting.

Review your contractor list quarterly. Don't wait until December 15 to discover you've been paying someone all year without a W-9 on file. Run a report every quarter showing year-to-date payments to all contractors. Identify anyone approaching $600. Verify you have current W-9s for everyone who'll cross the threshold.

Consider using 1099 preparation services. For $5-10 per form, services like Track1099, Tax1099, or even your payroll provider will handle everything: generating forms, printing and mailing recipient copies, filing electronically with the IRS and state agencies, storing records. Given that a single penalty costs $60 minimum, this is cheap insurance.

State requirements vary wildly. Some states want copies of every 1099 you file federally. Others only want certain boxes. A few piggyback on federal filing and don't require separate submission. Check your state's revenue department requirements or let filing software handle it.

The January crunch is real. You've got 31 days after year-end to compile info, generate forms, and distribute them. Starting in mid-December—while December's payments are still processing—makes this manageable. Starting January 2? You'll be working weekends.

Common 1099 Filing Mistakes to Avoid

The hardest thing in the world to understand is the income tax

— Albert Einstein

Even conscientious business owners stumble on these:

Misclassifying employees as contractors. This goes beyond just 1099 issues—it's potentially the most expensive mistake on this entire list. The IRS uses a 20-factor test examining behavioral control (who directs the work?), financial control (who provides tools and bears risk?), and relationship type (ongoing or project-based?).

Get this wrong and you're facing back payroll taxes at 7.65% of all wages, federal unemployment tax, penalties for failing to withhold, interest on everything, and potential state unemployment claims. A $50,000 worker misclassified for two years could easily trigger $20,000+ in back taxes and penalties.

Rule of thumb: if you control when, where, and how someone works, provide their equipment, pay them regularly rather than per project, and expect ongoing availability, they're probably an employee. Calling them a contractor doesn't make it so.

Forgetting about rent payments. This catches people constantly. You pay your landlord $2,000 monthly for office space—that's $24,000 annually. If your landlord operates as a sole proprietor or partnership (many small property owners do), you owe them a 1099-MISC. The form isn't just for hired services; rent is a major category.

Same with equipment rentals. Lease a van from an individual for business deliveries? Report it.

Using 1099-NEC when you should use 1099-MISC, or vice versa. Services go on NEC. Rent, royalties, prizes, medical payments go on MISC. Mixing them up frustrates recipients because the IRS processes these forms differently and expects income reported in specific places on tax returns.

Name/TIN mismatches. The IRS automatically checks whether the name and taxpayer ID number on your 1099 match their records. Mismatch? You get a B-notice demanding correction. This happens when contractors give you their business name but their personal Social Security number, or their legal name doesn't match what they go by professionally.

The W-9 should show both the legal name per IRS records and any DBA ("doing business as") name. Use the legal name on the 1099.

Assuming all LLCs are corporations. Single-member LLCs are disregarded entities by default—treated exactly like sole proprietorships for tax purposes. They need 1099s. Only LLCs that have formally elected corporate tax status get the exemption. Check box 3 on the W-9 to be certain.

Treating combined payments inconsistently. You paid someone $800 total: $500 by check, $300 via credit card. Your 1099 should report $500, not $800, because the card processor reports the other $300. But you need to track both amounts to understand the full business relationship and verify your expense records.

1099 Reporting Requirements by Payment Type and Recipient

What You Paid For

Who You Paid

Total for Year

Which Form

Must You File?

Professional services

Self-employed individual

$600 or more

1099-NEC

Yes

Professional services

LLC with one owner (default tax status)

$600 or more

1099-NEC

Yes

Professional services

Partnership or multi-owner LLC

$600 or more

1099-NEC

Yes

Professional services

Incorporated business (C-corp)

$600 or more

None

No—except law firms

Professional services

S-corporation

$600 or more

None

No—except law firms

Legal fees or settlements

Any law firm or attorney

$600 or more

1099-NEC

Yes, regardless of structure

Office or property rent

Individual landlord

$600 or more

1099-MISC

Yes

Equipment or vehicle rental

Non-corporate lessor

$600 or more

1099-MISC

Yes

Contest prizes or awards

Individual winner

$600 or more

1099-MISC

Yes

Medical service payments

Individual or non-corp provider

$600 or more

1099-MISC

Yes

Any payment via credit card

Anyone

Any amount

None

No—processor files 1099-K

PayPal or Venmo for business

Anyone

Any amount

None

No—platform files 1099-K

Product purchases

Anyone

Any amount

None

No—buying goods isn't reportable

Personal (non-business) expense

Anyone

Any amount

None

No—must be business-related

The IRS states in Publication 15 that businesses must submit a 1099-NEC when they've paid $600 or more during the year for services to someone who isn't on their payroll. The tax agency emphasizes these information returns exist because they significantly improve taxpayers' voluntary compliance rates—people report income more accurately when they know matching documentation is on file with the government.

FAQ: 1099 Contractor Payment Rules

Do I need to issue a 1099 for payments under $600?

No. The trigger point is $600 or more in cumulative payments throughout the calendar year. Pay someone $550 total and you're off the hook—no form to file, no reporting to the IRS. That said, keep records of all contractor payments for your own accounting and tax deduction purposes. And remember, that contractor still owes income tax on the $550 they earned from you, regardless of whether they receive a 1099.

What if I paid someone $599 – do I still report it?

No, $599 is below the threshold. You need to reach exactly $600 before reporting kicks in. But watch out for this scenario: you pay someone $599 one year, then $100 the next year. That second year, you're filing a 1099 for the $100 because it crosses the threshold for that year. Some businesses issue "courtesy" 1099s for amounts below $600 to help contractors with their bookkeeping, but it's completely optional.

Do I need to send a 1099 to an LLC?

Sometimes yes, sometimes no—it entirely depends on how that LLC is taxed. An LLC with one owner that hasn't filed special paperwork with the IRS is treated as a sole proprietorship, so yes, you file a 1099. An LLC with multiple owners defaults to partnership taxation, so again, yes to the 1099. But an LLC that elected to be taxed as a corporation? No 1099 required (except for legal services). You can't tell just from the name. Request a W-9—box 3 shows exactly how they're classified for tax purposes.

Can I be penalized if the contractor doesn't provide a W-9?

Absolutely, but you can protect yourself. When a contractor won't provide Form W-9, federal rules require you to implement backup withholding—deduct 24% from every payment and send it directly to the IRS. So a $1,000 payment becomes $760 to the contractor and $240 to the government. You report this using Form 945. This withholding shields you from penalties when you can't file an accurate 1099 due to missing information. Best approach? Make W-9 submission mandatory before releasing any payment.

What's the difference between 1099-NEC and 1099-MISC?

1099-NEC is exclusively for reporting payments to independent contractors for services they performed. Hired a freelance graphic designer, marketing consultant, or bookkeeper? That's 1099-NEC territory. Form 1099-MISC handles the miscellaneous category: rent you paid to landlords, prizes awarded at company events, royalty payments to creators, medical and healthcare payments. The IRS split these forms in 2020 to simplify processing. NEC has a hard January 31 deadline for both recipient copies and IRS filing, while MISC deadlines vary based on which specific boxes contain amounts.

Do I need to issue a 1099 for payments made via PayPal or Venmo?

Not from you directly. When you send payment through PayPal, Venmo, or any third-party settlement network for business purposes, that platform handles the reporting by issuing Form 1099-K to the recipient. You're not required to also file a 1099-NEC for those same transactions—that would mean double-reporting to the IRS. Important caveat: this exemption only applies to payments actually made through the platform. If you paid a contractor $1,000 total—$600 through Venmo and $400 by business check—you must issue a 1099-NEC reporting the $400 check payment.

The $600 threshold is straightforward. Everything surrounding it—entity types, payment methods, form variations, deadlines—creates the complexity.

Build systems now, before January arrives and you're scrambling. Require W-9 forms before cutting any contractor's first check. Set up your accounting software to flag contractor payments. Run quarterly reviews instead of annual fire drills. When you're uncertain whether a specific payment needs reporting, spend $100 on a CPA consultation rather than risking a $310 penalty.

The IRS has gotten increasingly serious about information reporting because the data works. Contractors who receive 1099s declare their income more completely than those who don't, and automated matching systems catch discrepancies almost immediately. This isn't going away—enforcement is only getting stricter as IRS technology improves.

Treat 1099 compliance as part of your regular financial close process, not as a special annual project. Collect forms in real-time, categorize payments as they happen, and review obligations quarterly. This approach eliminates the January panic while keeping you solidly compliant with IRS requirements. Your contractors will appreciate receiving their forms on time, and you'll avoid the penalties that can quickly exceed the cost of proper systems.

UCC stands for the Uniform Commercial Code, a comprehensive set of laws governing commercial transactions across the United States. For business owners, attorneys, and anyone involved in buying or selling goods, understanding the UCC is essential to structuring enforceable agreements and avoiding costly disputes

Transactional law encompasses the legal work involved in business deals and commercial arrangements. Unlike litigation attorneys who resolve disputes in court, transactional lawyers structure transactions, draft agreements, and prevent legal problems before they arise

Section 382 limits NOL carryforwards after ownership changes to prevent tax loss trafficking. Learn how ownership tests work, limitation calculations, and compliance requirements for M&A transactions

Personal liability means you can be held financially responsible for business debts and lawsuits using your own assets. Understanding when protection applies, how corporate structures shield personal wealth, and where vulnerabilities exist helps you make informed decisions safeguarding your financial future

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to business and corporate law, contracts, compliance, disputes, M&A, and taxation for companies.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Legal outcomes may vary depending on jurisdiction, company structure, and individual circumstances.

This website does not provide legal advice, and the information presented should not be used as a substitute for consultation with qualified corporate attorneys or legal professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.