Modern bank compliance department office with multiple monitors showing connection diagrams and world map, analyst desk with documents, corporate cold lighting

Banks and financial firms can't treat every customer the same way anymore. Your neighborhood teacher depositing a paycheck? That's straightforward. A holding company registered in the Bahamas, owned by a government official's nephew, moving $2 million monthly through wire transfers? That's a different story entirely.

Enhanced due diligence helps institutions separate legitimate high-value business from sophisticated money laundering schemes. Think of it as the difference between a quick background check and a full-scale investigation—one takes minutes, the other might take weeks and involve multiple analysts poring through documents in three languages.

Understanding Enhanced Due Diligence in AML Compliance

Enhanced due diligence means conducting intensive background investigations on customers who show significant money laundering, terrorist financing, or fraud warning signs. You're not just confirming someone's identity—you're building a complete financial profile that explains where their money came from and why they're conducting specific transactions.

Banks started implementing these deeper checks after repeatedly getting burned. Remember the BCCI collapse in 1991? That bank operated as a criminal enterprise for years while regulators missed obvious signs. Then came the Russian money laundering scandals in the late 1990s, when billions flowed through major banks' correspondent accounts. After September 11th, everyone realized terrorists had been moving funds through regular banking channels without triggering any alarms.

These expensive lessons shaped modern AML enhanced due diligence protocols. The underlying question shifted from "Do we know who this customer is?" to "Do we understand this customer's entire financial situation well enough to spot when something doesn't make sense?"

Author: Samantha Keene;

Source: craftydeb.com

Financial institutions can't avoid this responsibility. Banks and credit unions face the strictest requirements, but the net extends further. Broker-dealers scrutinize investment accounts. Money services businesses examine customers conducting frequent international transfers. Casinos investigate high-rollers. Insurance companies look closely at customers buying policies with large cash values. Even real estate professionals and precious metals dealers encounter situations requiring deeper investigation.

KYC enhanced due diligence goes beyond collecting a driver's license and utility bill. You need to understand someone's career trajectory, their business relationships, their sources of income over time. A venture capitalist opening a wealth management account needs verification, sure—but a former government minister from a country known for corruption requires an entirely different level of scrutiny, even if both customers present similar account balances.

The first rule of laundering money is the same as the first rule ofeli crime generally: don't get caught

— Jeffrey Robinson

Enhanced Due Diligence vs Standard Due Diligence

Standard customer verification works fine for routine banking relationships. You check an ID, confirm an address, run the name through sanctions databases, assign a risk score. For someone opening a checking account to receive their salary and pay bills? That's sufficient. The whole process takes maybe 30 minutes.

What triggers the escalation to enhanced procedures? Sometimes you know immediately—the customer's profile screams high-risk from day one. Other times, a customer starts out looking normal but their behavior changes. Maybe they've maintained a $3,000 average balance for two years, then suddenly start receiving $50,000 wire transfers from overseas companies with no clear business connection.

Here's a detailed comparison:

Criteria

Standard Due Diligence

Enhanced Due Diligence

Customer Risk Level

Typical retail customers, established local businesses, routine transactions

Government officials, customers from FATF-blacklisted countries, complex ownership structures, cash-intensive operations

Documentation Required

Photo ID, address verification, basic business registration if applicable

Detailed wealth statements, tax filings from multiple years, complete beneficial ownership documentation, third-party professional references, transaction histories

Verification Depth

Automated database matching, standard sanctions list screening

Manual investigation of claims, independent source corroboration, negative news searches across multiple languages, possible in-person interviews or site visits

Monitoring Frequency

Annual or biennial profile updates

Continuous automated monitoring plus monthly or quarterly manual file reviews

Approval Authority

Branch managers or junior compliance staff

Senior compliance officers, risk committee, or executive management

Cost/Time Investment

15 minutes to 2 hours, minimal expense

Multiple days to several weeks, potentially thousands in investigation costs

You'll notice the resource difference is dramatic. One compliance officer can process dozens of standard due diligence cases daily. That same officer might spend an entire week on a single enhanced due diligence investigation, especially if the customer operates across multiple jurisdictions or has complicated ownership structures.

Common triggers for moving from standard to enhanced procedures include: discovering the customer qualifies as a politically exposed person, learning their business operates primarily in countries with weak AML controls, noticing transaction patterns that contradict their stated business purpose, or finding negative media coverage suggesting criminal associations.

Here's a mistake many institutions make: they treat enhanced due diligence as a one-time hurdle. They conduct an intensive investigation, approve the relationship, then relax their vigilance. Wrong approach. A customer requiring enhanced scrutiny at onboarding still needs elevated monitoring throughout the relationship. You can't downgrade their risk profile unless their circumstances fundamentally change—and you'd better document why you think the risk decreased.

When Financial Institutions Must Perform Enhanced Due Diligence

Regulations mandate enhanced procedures for specific situations, but institutions also need to apply their own risk-based judgment. Here are the clearest scenarios requiring deeper investigation:

Politically Exposed Persons (PEPs): Anyone holding significant government positions—cabinet ministers, legislators, senior military commanders, executives running state-owned corporations. This category covers family members too. A transportation minister's wife starting a logistics company deserves intense scrutiny, even though she holds no official government role herself. Close business associates of PEPs also fall under enhanced requirements. If someone's primary business partner is a government official, you need to understand that relationship thoroughly.

Author: Samantha Keene;

Source: craftydeb.com

High-Risk Jurisdictions: The Financial Action Task Force maintains lists of countries with strategic AML deficiencies. Nations under comprehensive sanctions obviously raise red flags. Tax havens and secrecy jurisdictions like the British Virgin Islands or Panama warrant closer looks, especially when customers maintain complex corporate structures there without clear business reasons. A wire transfer request to a bank in Iran or North Korea should stop the transaction immediately for investigation—though most banks wouldn't maintain any relationships touching those jurisdictions.

High-Risk Customer Categories: Non-resident aliens without clear ties to the United States. Cash-intensive operations like check cashing stores, money transmitters, or casinos (yes, financial institutions serving these businesses need enhanced procedures for their customers). Shell companies using nominee shareholders or bearer shares. Customers who dodge questions or provide incomplete information. Here's an obvious example: an LLC listing only a registered agent's address, with nominee officers and no transparency about who actually owns or controls it.

Suspicious Activity Patterns: Transactions that don't make economic sense given what you know about the customer. Structuring deposits to stay just under $10,000 reporting thresholds. Money moving rapidly in and out of accounts—coming in via wire transfer Monday, transferred back out Tuesday. Activity completely mismatched to the customer's supposed business. Picture a nonprofit organization that receives $5 million in wire transfers monthly, then immediately forwards the funds to accounts in three different countries. What charitable purpose does that serve? None, most likely.

Transaction Thresholds: Large transactions don't automatically require enhanced due diligence, but they demand attention when combined with other risk factors. That customer with a $5,000 typical balance depositing $100,000 in cash needs to explain where that money came from and why they're depositing it in cash rather than through normal banking channels.

FinCEN expects institutions to develop their own risk criteria beyond regulatory minimums. Two customers might both qualify as PEPs, but a defense minister from a country ranked highly corrupt presents different risks than a city council member from Norway. Your procedures should account for these distinctions.

The Enhanced Due Diligence Process Step by Step

Conducting enhanced procedures follows a structured workflow, though you'll adapt specific steps based on each customer's unique risk factors.

Initial Risk Assessment and Customer Profiling

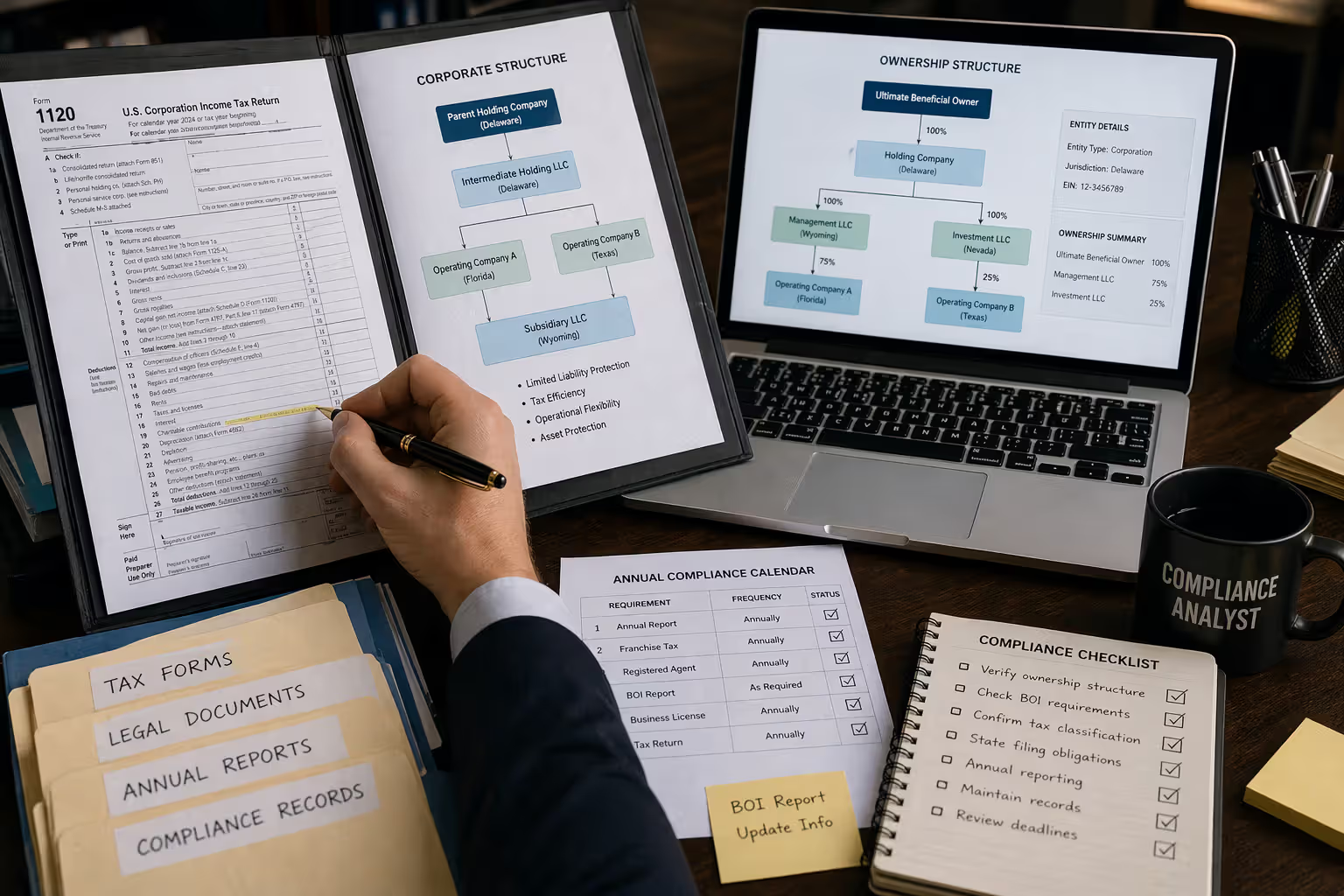

You start by gathering far more information than standard onboarding requires. Beyond identity documents, you're collecting business registration filings, ownership charts mapping corporate structures, and detailed questionnaires about business operations.

For individuals, you need employment history going back years. How did someone progress from entry-level positions to claiming $10 million net worth by age 35? They mentioned "successful investments"—what investments? When did they make them? What was the initial capital? Where did that initial capital come from?

Corporate customers create layered complexity. You might start with a Delaware LLC, trace ownership to a Cayman Islands holding company, follow that to a Panamanian private foundation, and eventually—hopefully—identify the actual human beings controlling everything. Each ownership layer requires verification through corporate registries, legal documentation, and independent research.

Risk scoring systems assign numerical values to various factors: customer type, geographic connections, products they're using, transaction volumes. Scores exceeding certain thresholds trigger enhanced protocols automatically. But you can't rely solely on automated scoring. A customer might score moderate on quantitative factors while showing qualitative warning signs—maybe there's negative news coverage, or their explanation for source of wealth keeps changing, or they're evasive when asked direct questions.

Source of Wealth and Funds Verification

This distinguishes enhanced from standard procedures more than any other element. Source of wealth examines how someone accumulated assets over their lifetime. Source of funds focuses on the specific money involved in this particular banking relationship.

A real estate developer claiming wealth from property investments? You need tax returns showing rental income and capital gains from sales. Title records proving which properties they own. Documentation of major property transactions. Vague statements about "successful real estate deals" don't cut it.

Someone claiming they inherited $5 million needs to produce the deceased person's will, estate settlement documents, and tax filings showing estate values. Plus you should verify that the deceased person actually had $5 million to leave behind—did they earn it, inherit it themselves, win a lawsuit? The investigation can extend back multiple generations.

For funds entering the current banking relationship, you need wire transfer details, sales contracts, loan agreements, or investment statements. Customer deposits $500,000 claiming it's from selling their business? Show me the purchase agreement. Verify the buyer exists and has the financial capacity to make this purchase. Confirm the transaction's legitimacy through public records or third-party sources.

Third-party verification adds crucial credibility. With customer consent, contact their accountant, attorney, or business partners. Search property registries. Check corporate databases. Look for independent confirmation of their story.

Author: Samantha Keene;

Source: craftydeb.com

A useful principle: customer statements alone never satisfy enhanced requirements. If you can't verify claims through documents or reliable third parties, the risk remains unmitigated regardless of how convincing the customer sounds.

Ongoing Transaction Monitoring

Approved customers requiring enhanced procedures need continuous surveillance, not just careful onboarding. Monitoring systems flag transactions deviating from expected patterns established during initial assessment.

You're watching transaction sizes, frequency, geographic destinations, types of counterparties, products being used. That customer whose business profile indicated domestic retail sales suddenly starts wiring funds to shell companies in the Cayman Islands? Alert. Investigate immediately.

Review frequency scales with risk severity. Your highest-risk relationships might need weekly manual reviews by experienced compliance officers. Automated systems can watch daily transaction activity, but humans must investigate anything the systems flag as unusual.

Periodic re-evaluations—typically annual for enhanced relationships—reassess the customer's overall risk profile. Has their business legitimately expanded, or do transaction volumes seem disconnected from their stated operations? Have new PEP connections emerged? Has their operating jurisdiction improved or deteriorated in AML effectiveness ratings?

Document everything. Compliance teams maintain detailed logs showing review dates, specific findings, investigative steps taken. "We monitored this account" means absolutely nothing to examiners unless you have records proving what you reviewed, what you found, and what conclusions you reached.

Enhanced Due Diligence Requirements Under US Regulations

The Bank Secary Act established foundational customer due diligence mandates, with deeper investigation required when circumstances warrant. Section 312 of the USA PATRIOT Act created explicit enhanced requirements for correspondent banking arrangements and private banking services provided to non-US persons.

FinCEN's Customer Due Diligence Rule—fully effective since May 2018—established explicit beneficial ownership requirements. Institutions must identify and verify individuals owning 25% or more of legal entity customers, plus at least one person exercising significant control. When enhanced procedures apply, institutions often lower that ownership threshold to 10% or verify all owners regardless of ownership percentage.

Regulators care about substance, not just checking boxes. Examiners evaluate whether your EDD procedures reasonably detect and report suspicious activity. A bank performing perfunctory enhanced reviews without substantive investigation faces criticism even when they've technically collected required documents.

Penalties for inadequate programs range from civil money penalties into the millions to enforcement actions restricting business activities. Recent years have seen institutions paying massive settlements for AML failures that included insufficient enhanced due diligence. A regional bank paid $35 million in 2024 after examiners discovered it approved multiple high-risk relationships without properly verifying source of wealth claims.

Individual accountability has intensified. Compliance officers and senior executives can face personal penalties for willful violations. Regulators send a clear message: enhanced due diligence isn't paperwork theater performed for examination purposes. It's a substantive defense against facilitating financial crime.

Recordkeeping mandates require retaining all EDD documentation for five years minimum after relationships end. This includes initial investigation files, ongoing monitoring logs, investigation notes, suspicious activity reports filed. During examinations, regulators sample high-risk relationships and scrutinize the complete file for each one.

Enhanced Customer Due Diligence Checklist

A practical approach to enhanced investigation includes these components:

Customer Identification and Verification: - Government-issued photo identification (passport, driver's license, national ID card) - Third-party database verification confirming identity details - Biometric verification for extreme risk cases - Comprehensive adverse media searches covering criminal records, sanctions lists, negative news coverage in multiple languages

Beneficial Ownership and Control: - Complete ownership structure charts for entity customers - Identification and verification of all beneficial owners (applying risk-appropriate percentage thresholds) - Documentation identifying control persons and decision-makers - Corporate registry searches in all formation and operating jurisdictions

Source of Wealth Documentation: - Personal or business tax returns covering at least three years - Audited financial statements and bank account records - Employment verification letters and income documentation - Documentation showing asset acquisition (property deeds, investment account statements, business sale agreements) - Inheritance or gift documentation with independent verification of the donor's wealth

Source of Funds Verification: - Complete transaction documentation for funds entering the relationship - Third-party verification of transaction counterparties - Business contracts, sale agreements, or settlement documents - Loan documentation if funds were borrowed

Business Purpose and Activity: - Detailed written description of business operations - Customer's explanation of anticipated account activity patterns - Expected transaction characteristics (volume, frequency, destinations, amounts) - Relevant business licenses and regulatory approvals - Client or customer lists if applicable

Geographic Risk Assessment: - Identification of all jurisdictions where customer operates, maintains accounts, or conducts regular business - Evaluation of each jurisdiction's AML/CFT regulatory framework - Assessment of sanctions exposure related to those jurisdictions

Ongoing Monitoring Parameters: - Customer-specific transaction monitoring thresholds - Scheduled review frequency - Escalation procedures for suspicious activity - Timeline for next comprehensive re-evaluation

Red Flags Requiring Investigation: - Reluctance or refusal to provide requested information - Inconsistencies between stated business activities and observed transaction patterns - Transactions lacking clear economic rationale - Unnecessary use of intermediaries without transparent business purpose - Rapid movement of funds with minimal float time - Activity inconsistent with customer's documented wealth or income sources - Changes in account behavior without corresponding changes in business circumstances

Approval and Documentation: - Senior management approval documented in writing - Risk assessment memorandum explaining the approval decision - Ongoing monitoring logs with dated entries - Investigation reports documenting any suspicious activity reviews

Missing even a single element creates compliance gaps that examiners will identify. Institutions sometimes thoroughly verify identity but inadequately document source of wealth, leaving themselves vulnerable to unwittingly accepting laundered funds.

Common Challenges and Best Practices

Building robust enhanced due diligence programs creates operational difficulties requiring careful navigation.

Resource Intensity: Enhanced procedures consume enormous time and personnel resources. A single high-risk customer might need 20-40 compliance hours during onboarding, then ongoing monitoring adding several hours monthly. Smaller institutions struggle justifying this investment for individual relationships, sometimes leading to de-risking—refusing entire customer categories rather than managing them appropriately.

Author: Samantha Keene;

Source: craftydeb.com

The fundamental trade-off: accept fewer high-risk customers while performing genuinely effective investigations versus maintaining larger portfolios with superficial reviews that won't withstand regulatory scrutiny. Quality always beats quantity when examiners sample your files.

Information Availability: Customers from certain jurisdictions operate in environments with limited public records, unreliable government documentation, and deliberately opaque business practices. Verifying source of wealth for a customer from a country with poor record-keeping becomes an exercise in assembling fragmentary evidence from multiple partial sources.

Best practice: establish minimum documentation standards and decline relationships that can't meet them. "We cannot verify this claim through available information" provides legitimate grounds for rejection.

Customer Experience: Enhanced procedures create significant friction. Customers accustomed to opening accounts in 20 minutes face extensive questionnaires, multiple documentation requests, and approval delays potentially lasting weeks. Some perceive this as discriminatory or unreasonably invasive.

Clear communication helps considerably. Explain that enhanced procedures protect both the institution and the customer—preventing account misuse that could lead to funds being frozen or accounts closed abruptly. Frame the process as protective rather than punitive.

Technology Solutions: Modern AML platforms offer automated screening, continuous transaction monitoring, and case management tools. These systems handle data aggregation and pattern detection that would be completely impossible manually given transaction volumes.

Technology can't replace human judgment, though. Automated systems flag anomalies—humans must investigate context. A $100,000 deposit might indicate money laundering or might represent a documented business sale. Software algorithms can't make that distinction without human analysts reviewing evidence.

Staff Training: Effective investigations require skilled analysts who understand financial crime typologies, red flag indicators, and investigative techniques. Many institutions underinvest in training, leaving junior staff to conduct complex investigations without adequate preparation or supervision.

Regular training on emerging risks keeps teams effective—new money laundering methods, evolving regulatory expectations, jurisdiction-specific issues. Case studies showing real-world compliance failures and enforcement actions provide practical learning more valuable than abstract policy discussions.

Balancing Risk and Access: Overly aggressive enhanced procedures can exclude legitimate customers, particularly immigrants, entrepreneurs, and individuals from developing countries who may have limited documentation. Insufficiently cautious procedures expose institutions to illicit finance.

Risk-based approaches calibrate scrutiny to actual risk. A refugee with limited formal documentation presents different considerations than a PEP with wealth claims inconsistent with documented income. Both might require enhanced procedures, but specific steps and evidentiary standards should reflect their distinct risk profiles.

Frequently Asked Questions About Enhanced Due Diligence

How much time does an enhanced investigation typically require?

Timeline varies dramatically based on customer complexity and information availability. Straightforward cases involving individuals with transparent income sources might conclude within several days. Complex corporate structures spanning multiple jurisdictions with opaque ownership can take several weeks or even months. Customers providing complete, organized documentation upfront significantly accelerate the process. Those submitting information piecemeal or requiring multiple follow-up requests extend timelines substantially. Institutions should set realistic expectations with customers—explain that approval isn't guaranteed and that the timeline depends partly on how thoroughly they respond to information requests.

How does customer due diligence differ from enhanced due diligence?

Customer due diligence establishes the baseline requirements for every banking relationship—identity verification, address confirmation, sanctions screening, initial risk assessment. Enhanced due diligence adds multiple investigative layers: deeper investigation into wealth origins, more frequent monitoring, additional documentation requirements, senior-level approval authority. Think of CDD as the routine health screening everyone gets at an annual checkup, while EDD resembles the comprehensive diagnostic testing ordered when symptoms suggest potential serious problems requiring specialist attention.

Must every financial institution conduct enhanced investigations?

All regulated financial institutions must maintain written enhanced due diligence procedures and apply them when circumstances warrant. Larger banks with international operations typically have more elaborate programs because they encounter more high-risk customer types regularly. Smaller community banks might rarely perform EDD if their customer base consists primarily of local individuals and businesses presenting standard risk profiles. However, regulatory requirements apply regardless of institution size—even small banks must have documented procedures and implement them appropriately when they encounter politically exposed persons, high-risk jurisdictions, or suspicious activity patterns.

Which documents does enhanced verification require?

Required documentation depends heavily on customer type and specific risk factors identified. Common requirements include government-issued identification, address verification, multiple years of tax returns, audited financial statements, detailed source of wealth documentation (employment records, investment statements, inheritance papers, business sale agreements), complete beneficial ownership information for entities, relevant business licenses, and transaction documentation. Higher-risk cases might demand additional materials: professional references from attorneys or accountants, proof of business operations (client contracts, invoices, delivery records), or reports from on-site business visits. Institutions should provide customers with specific, tailored checklists rather than generic document requests.

Can technology fully automate enhanced investigations?

Technology automates specific components effectively—database searches, sanctions screening, adverse media monitoring, transaction pattern analysis, risk scoring. However, core elements require human judgment: evaluating whether source of wealth explanations make sense, assessing document authenticity, investigating inconsistencies or contradictions, making ultimate approval decisions. The most effective programs combine automated data gathering and monitoring with skilled analyst review and investigation. Attempting fully automated EDD would miss contextual factors and nuanced risk indicators that experienced compliance professionals recognize through training and experience.

What occurs when customers refuse enhanced verification?

Institutions cannot maintain relationships with customers refusing to provide information necessary for adequate due diligence. If someone declines submitting required documentation or answering questions about wealth sources, the institution must deny the account application or terminate the existing relationship. No middle ground exists—regulatory requirements don't permit accepting high-risk customers without appropriate scrutiny. Customers who legitimately cannot provide certain specific documents might work with compliance teams to identify alternative verification methods achieving similar objectives, but outright refusal to cooperate ends the relationship immediately.

Enhanced due diligence provides financial institutions' most powerful defense against money laundering, terrorist financing, and fraud. The process demands significant resources, skilled personnel, and institutional commitment. But consider the alternative—facilitating criminal activity through inadequate scrutiny carries far greater costs in regulatory penalties, reputational damage, and societal harm.

Effective programs balance thoroughness with practicality. They concentrate resources on genuine threats through risk-based approaches rather than treating all customers identically. They leverage technology for efficiency while preserving human judgment for complex decisions requiring expertise and context. They maintain documentation demonstrating to regulators and institutional leadership that high-risk relationships receive appropriate oversight.

The landscape continues evolving constantly. Regulatory expectations increase. Financial crime methods grow more sophisticated. Technology offers new capabilities for both criminals and compliance teams. Institutions viewing EDD as a dynamic process requiring continuous improvement position themselves to meet these challenges successfully. Those treating it as a static checklist will find themselves perpetually behind both regulatory expectations and criminal innovation.

For compliance professionals, mastering enhanced procedures means developing investigative skills, understanding global financial crime patterns, and maintaining professional skepticism necessary to question convenient explanations. For financial institutions, it means building cultures where compliance concerns receive serious attention and adequate resources. For the financial system overall, robust practices create friction making criminal exploitation more difficult and detection more likely.

The question isn't whether to perform enhanced due diligence—regulations and prudent risk management demand it. The real question is whether your institution's program genuinely identifies and mitigates risks or merely creates compliance theater. That difference determines whether EDD protects your institution or leaves it vulnerable to the next enforcement action.

UCC stands for the Uniform Commercial Code, a comprehensive set of laws governing commercial transactions across the United States. For business owners, attorneys, and anyone involved in buying or selling goods, understanding the UCC is essential to structuring enforceable agreements and avoiding costly disputes

Transactional law encompasses the legal work involved in business deals and commercial arrangements. Unlike litigation attorneys who resolve disputes in court, transactional lawyers structure transactions, draft agreements, and prevent legal problems before they arise

Section 382 limits NOL carryforwards after ownership changes to prevent tax loss trafficking. Learn how ownership tests work, limitation calculations, and compliance requirements for M&A transactions

Personal liability means you can be held financially responsible for business debts and lawsuits using your own assets. Understanding when protection applies, how corporate structures shield personal wealth, and where vulnerabilities exist helps you make informed decisions safeguarding your financial future

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to business and corporate law, contracts, compliance, disputes, M&A, and taxation for companies.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Legal outcomes may vary depending on jurisdiction, company structure, and individual circumstances.

This website does not provide legal advice, and the information presented should not be used as a substitute for consultation with qualified corporate attorneys or legal professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.