Modern bank compliance operations center with large digital monitoring screens showing data dashboards and network analysis diagrams in a professional office environment

Money laundering costs the global economy roughly $2 trillion annually. Terrorist financing threatens international security. Corruption erodes public trust and destabilizes governments. Banks and financial firms sit squarely in the crosshairs of these threats—whether they like it or not.

That's where sanctions screening and politically exposed person (PEP) screening come into play. Think of them as your institution's radar system, designed to spot trouble before it lands in your portfolio. Here's the reality, though: most banks struggle to get these systems right. The Office of Foreign Assets Control levied north of $240 million in civil penalties throughout 2025, with the majority tied directly to screening failures that could've been prevented.

Getting sanctions and PEP screening right isn't just about avoiding fines anymore. It's about survival in an increasingly scrutinized industry.

What Are Sanctions and PEP Screening?

Let's start by separating these two concepts, because they're related but definitely not identical.

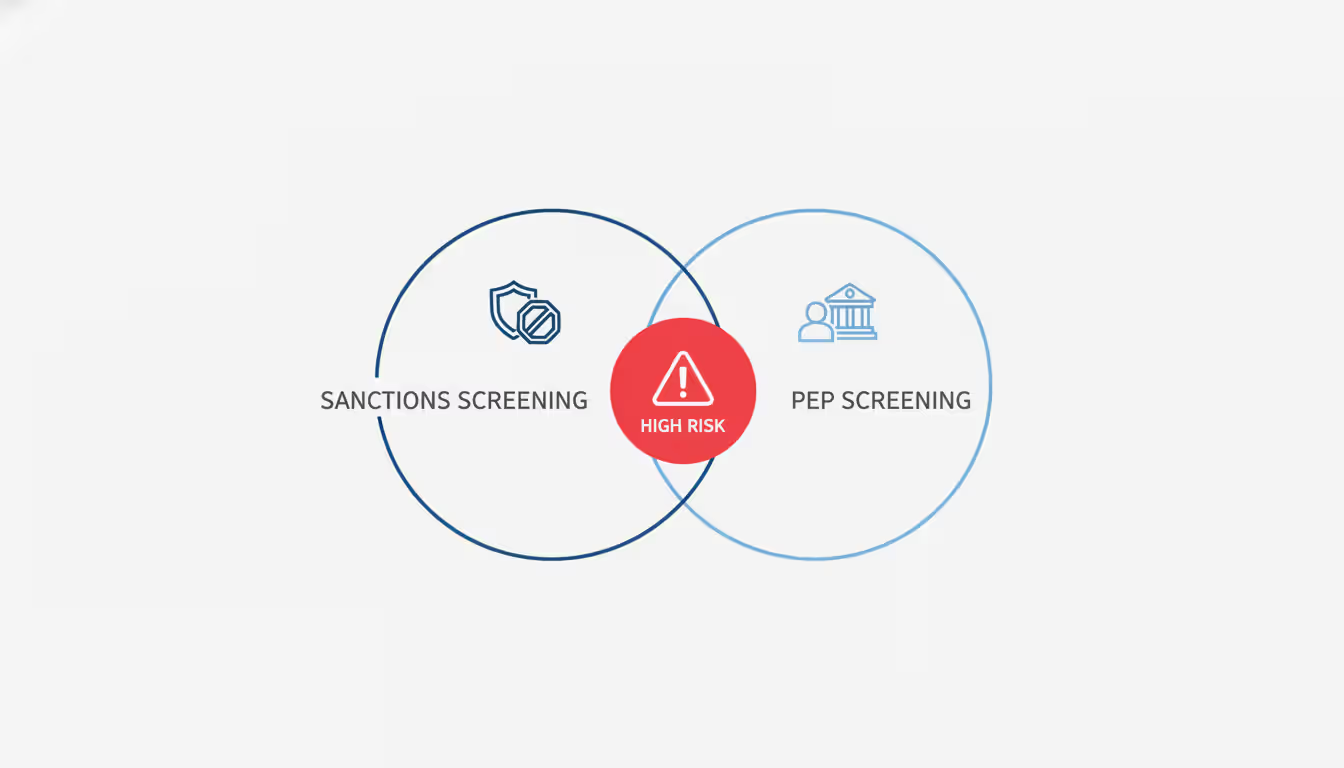

Sanctions screening is your frontline defense against doing business with the wrong people. Every time your bank processes a payment, opens an account, or executes a wire transfer, you're running names against government watchlists. These aren't suggestions—they're hard stops. The lists contain everyone from terrorist organizers to drug cartel leaders, from arms dealers to human rights violators. Miss one match, and you've just processed a transaction that violates federal law.

Meanwhile, PEP screening takes a different approach. Instead of catching criminals already on government lists, you're identifying people whose positions make them corruption risks. We're talking about government officials, their relatives, and their business cronies—people with access to public money and the power to abuse it. A city council member approving zoning changes? That's a PEP. A central bank official who controls monetary policy? Definitely a PEP. The spouse of a customs director who green-lights import licenses? You guessed it—also falls under PEP scrutiny.

Here's where it gets interesting: these screening types overlap. You might encounter a foreign minister (PEP status) who also appears on OFAC's sanctions list for human rights violations. That's when both systems need to work in concert, not in silos.

Author: Andrew Bellamy;

Source: craftydeb.com

Politically Exposed Persons Definition

The term "politically exposed person" covers anyone holding significant public authority, plus their family circle and known associates. FATF created this framework years ago, and now it's baked into AML regulations worldwide—though every country adds its own flavor.

We're really looking at three distinct buckets here:

Foreign PEPs run foreign governments or hold senior posts within them. Presidents, prime ministers, cabinet secretaries, supreme court justices, top military brass, executives running state-owned oil companies—they all qualify. Here's a real-world example: imagine a former finance minister from an emerging market who left office three years ago but maintains close ties with the current administration through consulting contracts. That person remains a foreign PEP, and their accounts deserve heightened scrutiny.

Domestic PEPs hold equivalent positions within your own country. Banks used to give these folks a pass compared to foreign PEPs, but that thinking has shifted dramatically. A state treasurer controlling billions in pension funds? Same corruption risk exists whether they're domestic or foreign. Recent high-profile prosecutions of U.S. state officials have driven this point home with regulatory force.

International organization PEPs occupy leadership roles at bodies like the World Bank, IMF, UN, or regional development institutions. A program director at the Inter-American Development Bank approving infrastructure projects faces similar temptations as any government official with spending authority.

But wait—the definition extends beyond the officeholder. Spouses automatically inherit PEP status. So do parents, children, and siblings. Close associates get flagged too, particularly business partners who jointly control companies with PEPs. Identifying these extended relationships takes genuine investigative work, not just database searches.

What Sanctions List Screening Involves

When you screen for sanctions, you're matching your customer data against multiple government databases simultaneously. Sounds simple enough, right? The devil's in the details.

Different authorities maintain different lists, each with its own legal weight:

OFAC's Specially Designated Nationals (SDN) List is the big one for U.S. institutions. With more than 11,000 entries as of early 2026, it covers individuals and entities completely prohibited from touching the U.S. financial system. A confirmed SDN match triggers immediate asset freezes—no exceptions, no delays. You block the transaction, freeze the funds, and file your report with OFAC.

The UN Security Council Consolidated List implements international sanctions targeting terrorism and weapons proliferation. These carry global authority, though enforcement quality varies wildly depending on which country you're operating in. Some nations implement UN sanctions rigorously; others treat them as suggestions.

EU Sanctions Lists address terrorism, human rights abuses, and geopolitical threats from a European perspective. After Brexit, the UK now maintains parallel lists that usually align with EU designations but sometimes diverge based on British foreign policy priorities.

OFAC's sectoral sanctions programs add another layer of complexity. Rather than completely blocking all transactions, these target specific industries—think Russian energy companies or Venezuelan state enterprises. You're not necessarily blocking everything; you're restricting certain transaction types while allowing others. That ambiguity creates headaches for compliance teams trying to parse what's permitted versus prohibited.

Here's where technology becomes crucial: your screening engine needs to handle name variations that would make your head spin. "Muhammad" appears on sanctions lists as "Mohammed," "Mohamed," "Muhammed," and half a dozen other transliterations—all referring to the same individual. Your system either catches these variations or you're gambling with regulatory violations.

Why Sanctions and PEP Screening Matter in Banking

Banks function as chokepoints in the global financial system. When screening fails, illicit money flows freely, undermining everything from national security to anti-corruption efforts.

U.S. regulations don't mess around here. The Bank Secrecy Act mandates comprehensive AML programs that include sanctions compliance. OFAC's enforcement authority allows civil penalties up to $330,000 or double the transaction amount—whichever hurts more—for each violation. That's per transaction, not per customer. Process 50 payments for a sanctioned entity? You're looking at potential penalties in the tens of millions. Criminal violations carry even sharper teeth: $20 million in fines and 30-year prison sentences for willful violations.

FinCEN's Customer Due Diligence Rule bakes PEP identification into mandatory compliance frameworks. The 2025 Anti-Money Laundering Act amendments expanded domestic PEP requirements after several governors and state legislators caught corruption charges involving foreign business interests.

Beyond regulatory heat, consider the reputational fallout. A regional bank in the Midwest processed $12 million in transactions for a county commissioner later convicted of accepting bribes from construction contractors. The regulatory fine hit $3.2 million. But remediation costs—external consultants, system overhauls, enhanced monitoring—totaled another $14 million. Civil lawsuits from fraud victims added $8 million in settlements. Correspondent banks severed relationships, cutting off international payment channels. The full damage exceeded $25 million for failures that proper PEP screening would've flagged immediately.

Recent enforcement trends reveal regulators expect integrated approaches. Running sanctions and PEP screening through separate systems creates blind spots. A sanctioned official's adult daughter (who qualifies as PEP family) might slip through if your systems don't cross-reference both screening databases.

Author: Andrew Bellamy;

Source: craftydeb.com

How Sanctions Screening Compliance Works

Effective screening operates continuously, not just at account opening. Think of it as a living process that adapts to new information constantly.

Initial screening happens when prospects apply for accounts or services. You collect identifying details—legal name, birth date, citizenship, residential address, government ID numbers—then run everything against current sanctions lists. Smart institutions screen beneficial owners, authorized signers, and related parties simultaneously, not just the primary account holder.

Transaction screening monitors activity as it happens. A customer might pass initial checks clean, then receive a wire transfer from a sanctioned entity three months later. Transaction screening catches these indirect exposures before the money settles. Your system analyzes every party mentioned: sender, receiver, intermediary banks, and anyone referenced in payment message fields.

Periodic rescreening addresses list volatility. OFAC updates the SDN list constantly—sometimes daily during international crises. A customer who cleared screening Monday morning might match a designation added Friday afternoon. Leading institutions rescreen their entire customer base daily. Smaller banks with limited resources might run weekly or monthly rescreening, accepting higher risk as a trade-off for operational constraints.

Database coverage determines whether your screening actually works. Relying exclusively on OFAC lists leaves massive gaps if you handle international customers. Comprehensive programs pull from UN, EU, UK, Canadian, Australian, and other national sanctions authorities. Third-party vendors aggregate these sources, but you can't just trust their marketing claims. One institution discovered their vendor's EU sanctions data lagged 72 hours behind official updates—an eternity when Russia invaded Ukraine and designations multiplied daily.

Matching technology walks a tightrope between sensitivity and usability. Set matching too strict, and you'll drown in false positive alerts. Set it too loose, and you'll miss true matches buried in transliteration variations. Most systems assign match scores based on similarity across multiple data points. A 95% match demands investigation. A 60% match probably represents a different person who coincidentally shares a similar name.

Alert review separates signal from noise. Screening generates an alert, then human analysts compare the customer's full profile against the list entry. They're not just checking name similarity—they're verifying birth dates, nationalities, known addresses, and listed aliases. An alert for "John Smith" requires deeper digging than one for "Svetlana Tikhanovskaya" simply because millions of people share common names.

Escalation protocols activate when analysts confirm matches. Potential sanctions hits go straight to senior compliance officers who determine required actions. Confirmed OFAC SDN matches trigger immediate freezes—assets locked, transactions blocked, usually within 30 minutes of confirmation. Your institution files a blocked property report with OFAC within 10 business days and maintains the freeze until OFAC removes the designation or issues a specific license permitting the relationship.

PEP Risk in Banking and AML PEP Checks

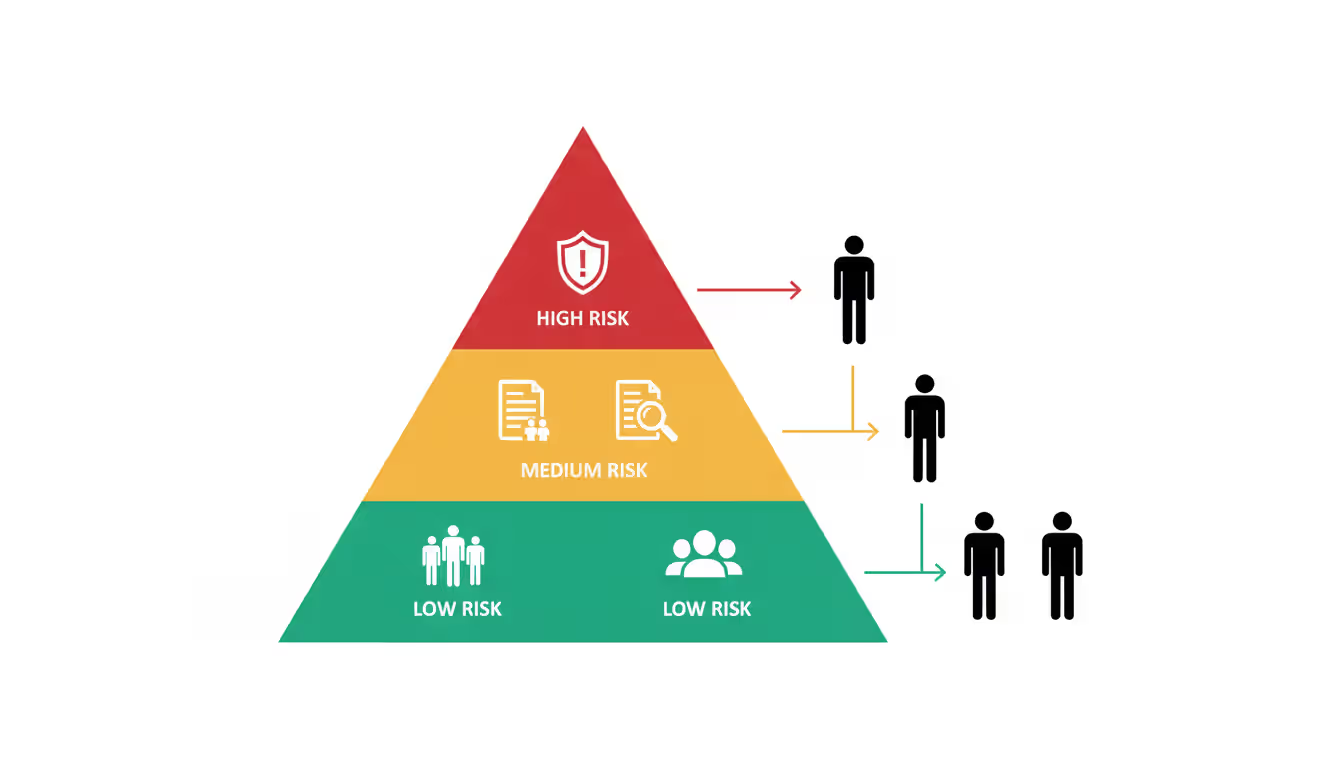

Not every PEP creates equal risk. Smart AML programs apply risk-based frameworks that match scrutiny levels to actual threat profiles.

Risk stratification considers way more than just PEP status alone. A retired town clerk from Denmark carries fundamentally different risk than an active defense procurement minister from a country where corruption is endemic. Geography matters enormously—PEPs from high-corruption jurisdictions warrant intensive scrutiny regardless of specific position. Transparency International's Corruption Perceptions Index offers useful benchmarks, though you'll want to develop internal risk matrices tailored to your customer base.

Position type drives risk assessment too. PEPs with direct access to public funds—tax collectors, government procurement officers, border customs officials—present higher corruption potential than ceremonial roles. A foreign ambassador to the United Nations has limited opportunities for financial misconduct compared to a provincial governor approving multimillion-dollar construction contracts.

Family proximity to the PEP influences risk ratings as well. An adult child running a completely independent tech startup poses less concern than a spouse who jointly manages investment portfolios with the PEP. A college roommate from 20 years ago deserves different treatment than a current 50/50 business partner.

Enhanced due diligence kicks in for high-risk PEPs. Standard customer due diligence might suffice for low-risk domestic PEPs from stable democracies. Foreign PEPs from high-corruption countries? You're conducting deep-dive investigations.

Enhanced measures include source of wealth verification—documenting how the PEP legally accumulated assets they're depositing. A cabinet minister earning $175,000 annually who shows up with $8 million to invest raises obvious red flags. You need to document legitimate sources: inheritance from a wealthy family, business success before entering public service, or spousal income from private-sector activities. Documentation means more than the customer's verbal explanation—you're collecting tax returns, inheritance records, business financial statements, whatever proves the story.

Ongoing monitoring intensifies dramatically for PEP relationships. Transaction patterns get microscopic attention. A PEP whose account normally handles $75,000 monthly suddenly processing $3 million in wire transfers? That triggers investigation even without any sanctions matches. Periodic relationship reviews occur more frequently—annually or every six months rather than the standard three-to-five-year cycle for regular customers.

Relationship approval often requires senior management sign-off. Many banks prohibit relationship managers from onboarding PEP customers without explicit compliance committee or board approval. This governance layer prevents sales pressure from overriding risk management discipline.

Exit strategies become necessary when PEP relationships exceed manageable risk thresholds. If your customer gets appointed to a cabinet position in a newly sanctioned country, continuing the relationship might violate regulations or exceed your institution's risk appetite. Orderly exit procedures let customers transfer funds elsewhere while protecting you from abrupt terminations that could trigger suspicious activity reporting obligations.

Building an Effective Sanctions Compliance Program

Author: Andrew Bellamy;

Source: craftydeb.com

Technology alone won't save you. Sustainable sanctions compliance requires policies, procedures, systems, training, and oversight working together seamlessly.

Written policies create your program's architecture. Effective policies define exactly what requires screening—which products, services, customer types, and transaction categories fall within scope. They specify which lists you're screening against, what matching thresholds trigger alerts, how analysts should investigate hits, and who makes final escalation decisions. Good policies address edge cases that will definitely come up: customers traveling to sanctioned countries, transactions denominated in currencies of sanctioned nations, or indirect exposure through multi-party transactions involving intermediaries.

Technology infrastructure separates functional programs from security theater. Modern screening platforms deliver capabilities manual processes can't match:

Real-time screening integration with core banking systems blocks prohibited transactions before they process. A wire transfer to a sanctioned party gets rejected automatically rather than discovered during quarterly audit reviews.

Automated list updates eliminate dangerous lag time between OFAC publishing new designations and your screening database reflecting changes. Cloud-based systems push updates within minutes of official publication—no waiting for overnight batch processes.

Machine learning improves accuracy over time by learning from analyst decisions. If your team consistently dismisses alerts for a common name when contextual information clearly identifies a different person, the system adjusts matching parameters to reduce similar false positives going forward.

Case management workflows create audit trails proving regulatory compliance. These systems assign alerts to specific analysts, track investigation time, flag overdue reviews, and document resolution rationale for every single alert.

Sanctions due diligence procedures guide analysts through investigation steps systematically. Procedures should specify exactly what information to review, where to find it, and how to document decisions. A standard sanctions alert investigation typically includes:

Comparing every available customer data point against the list entry—full legal name, all known aliases, birth date, birthplace, citizenship, passport numbers, current and historical addresses, and any government ID numbers. Even one definitive mismatch might clear the alert if it's something like birth date that couldn't plausibly be in error.

Searching public records and media sources for additional customer or list entry information. A customer claiming to be a different person than the list entry should have verifiable presence—social media profiles, property ownership records, business registrations, professional licenses—corroborating their distinct identity.

Documenting specific rationale for clearing false positives or escalating true matches. "Different person" is inadequate documentation; analysts should note precisely which differences justify their conclusion and what sources they consulted.

Training programs ensure everyone understands their specific responsibilities. Frontline staff who interact with customers need different training than back-office screening analysts. Relationship managers should recognize PEP red flags and know when to consult compliance before accepting business. Screening analysts need technical depth on list structures, name matching algorithms, investigative techniques, and escalation criteria.

Training frequency varies by role. Annual awareness sessions work for general staff. Analysts handling complex investigations benefit from quarterly updates covering regulatory changes, emerging typologies, new system features, and lessons learned from recent enforcement actions.

Independent testing validates whether your program actually works. Internal audit or external consultants should review screening processes annually at minimum. Testing might involve seeding test transactions containing sanctioned names to verify detection, reviewing closed alerts to assess decision quality, or interviewing analysts to gauge procedural understanding. The goal isn't checking compliance boxes—it's identifying gaps before regulators do.

Governance and oversight create accountability structures. Senior management needs regular reporting on screening metrics: alert volumes, false positive rates, processing times, confirmed true matches, regulatory communications, and system performance issues. Board-level committees should review program effectiveness annually at minimum, ensuring adequate budget and resources while addressing systemic weaknesses that metrics reveal.

You can't run sanctions and PEP screening in separate silos anymore—that's where your biggest risks hide. The dangerous cases emerge at the intersection: politically exposed persons exploiting their positions to help sanctioned entities, or designated parties using PEP relationships as backdoors into the financial system. Programs that connect these dots through integrated screening represent where compliance needs to go, not where it's been

— Jennifer Morrison

Common Challenges in OFAC Sanctions Screening

Even sophisticated programs hit obstacles that require continuous adaptation and problem-solving.

False positives plague every screening operation. Common names generate thousands of worthless alerts annually. "Mohammed Ali," "Maria Rodriguez," or "Robert Johnson" appear on sanctions lists but also represent millions of legitimate customers globally. False positive rates frequently exceed 95%—meaning 19 out of 20 alerts waste analyst time investigating people who clearly aren't sanctions targets.

Mitigation strategies include tuning matching logic to weight multiple data points rather than name alone, whitelisting verified customers after thorough vetting to suppress repeat alerts on the same non-match, and continuously adjusting matching thresholds based on operational data showing where false positives concentrate.

Data quality problems undermine screening accuracy fundamentally. Incomplete customer records missing birth dates or current addresses reduce the identifying information available to distinguish false matches from true hits. Inconsistent data entry—"Mohammed" versus "Muhammad," "Street" versus "St.," "New York" versus "NYC"—creates matching failures where screening algorithms can't connect obviously similar entries.

Fixing data quality requires front-end controls enforcing complete data capture at account opening, periodic data cleansing projects standardizing existing records, and integration with third-party data sources that append missing information from public records and commercial databases.

List maintenance headaches multiply as sanctions programs proliferate. Between OFAC, UN, EU, UK, Canada, Australia, Japan, Switzerland, and other jurisdictions, global institutions might screen against 40+ separate lists. Each has different structures, update schedules, and legal implications requiring different handling.

Centralized list management platforms help by aggregating sources, normalizing formats, and tracking update histories. But institutions still must map each list to appropriate screening scenarios—not every list applies to every transaction type or customer segment.

Cross-border complications arise when customers or transactions touch multiple jurisdictions with conflicting requirements. A European subsidiary of a U.S. bank faces both OFAC and EU sanctions, which sometimes point in opposite directions. EU regulations might permit transactions that OFAC prohibits, or vice versa. Your compliance program needs controls satisfying the stricter requirement while documenting compliance with both regulatory regimes to satisfy examiners from different agencies.

Technology limitations constrain some institutions, particularly smaller community banks operating legacy systems. Integrating real-time screening into core banking platforms built in the 1990s requires major investment that strained technology budgets can't support. Batch processing—screening transactions hours or days after they occur—creates windows where prohibited transactions might settle before detection.

Phased modernization approaches balance cost against risk. Critical high-value transactions might receive real-time screening immediately while lower-risk activities continue batch processing until budget allows system upgrades.

Resource constraints affect compliance programs across the industry. Qualified sanctions analysts command salaries exceeding $85,000 in competitive markets, and specialized expertise is scarce. Institutions in secondary markets struggle recruiting talent with the necessary technical skills and regulatory knowledge. Chronic understaffing produces alert backlogs, superficial investigations cutting corners, and elevated error risk from overworked analysts.

Outsourcing to specialized compliance firms offers partial solutions, though ultimate responsibility remains with your institution regardless of who performs the work. Technology investments reducing false positives and automating routine decisions can stretch existing staff further—one analyst supported by strong automation might handle workload previously requiring three people.

FAQ: Sanctions and PEP Screening

How do sanctions screening and PEP screening differ from each other?

Sanctions screening identifies whether customers or transactions involve parties explicitly prohibited by government regulations—terrorists, drug traffickers, sanctioned government officials, blocked entities. It's essentially binary: someone either appears on a sanctions list requiring action or they don't. PEP screening works differently—it flags politically exposed persons who aren't necessarily prohibited but require enhanced scrutiny due to elevated corruption risk from their government positions. You can be a PEP without being sanctioned, sanctioned without qualifying as a PEP, or both at once if you're a corrupt official who got designated.

What's the right frequency for conducting PEP and sanctions screening?

Initial screening hits every new customer at account opening, no exceptions. For sanctions, you need real-time or near-real-time transaction screening because OFAC and other authorities update lists constantly—sometimes multiple times daily during international crises like the Ukraine invasion. Customer rescreening against sanctions lists should run at least daily for active relationships; leading institutions rescreen continuously. PEP screening requires periodic updates matching your risk assessment—annually for lower-risk customers, quarterly or semi-annually for higher-risk relationships. You should also rescreen whenever customers update profile information or experience significant life changes like new government appointments.

What actions are required when a customer matches a sanctions list?

Response depends entirely on which list matched and the match type. A confirmed OFAC SDN match demands immediate action: freeze all assets under your control, block any attempted transactions, and file a blocked property report with OFAC within 10 business days. The customer cannot access frozen funds until OFAC removes their designation or issues a specific license. Other sanctions programs or non-blocking lists might require rejecting specific prohibited transactions while allowing the relationship to continue under enhanced monitoring, or filing reports without asset freezes. OFAC sectoral sanctions create the most ambiguity—you might need to block certain transaction types while permitting others involving the same customer.

Does PEP status automatically mean a customer is high-risk?

Not automatically, no. All PEPs require enhanced scrutiny beyond standard customers, but risk-based programs recognize that corruption risk varies enormously across PEP types. A retired municipal clerk from Norway who left office 10 years ago might qualify for medium or even low-risk classification after appropriate due diligence. Meanwhile, an active cabinet minister from a country ranking in the bottom quartile of Transparency International's Corruption Perceptions Index—someone with direct authority over government procurement—would definitely rate high-risk. Geography, specific position type, tenure duration, access to public funds, and individual circumstances all feed into appropriate risk classification.

What specific OFAC sanctions screening requirements apply to U.S. banks?

OFAC requires U.S. financial institutions to block accounts and reject transactions involving anyone on the SDN list, comprehensively sanctioned countries, and other designated parties. Banks must screen customers at onboarding, screen transactions before processing, and maintain systems capable of identifying matches despite name variations, transliteration differences, and incomplete data. You need risk-based procedures appropriate to your institution's size, customer demographics, and transaction patterns. When blocking occurs, you must file reports promptly, maintain blocked assets securely, and avoid tipping off the customer about why their transaction failed. OFAC doesn't mandate specific technologies or procedures—they expect effective programs that actually prevent prohibited transactions regardless of how you achieve that outcome.

What technology improvements can boost sanctions and PEP screening accuracy?

Modern technologies address multiple screening pain points simultaneously. Artificial intelligence and machine learning slash false positive rates by learning from analyst decisions and identifying patterns distinguishing genuine matches from coincidental name similarities—potentially reducing false positives by 40-60% compared to rules-based systems. Natural language processing handles name variations across different languages and writing systems more effectively than simple text matching that misses transliteration variants. Robotic process automation accelerates routine alert investigations by automatically gathering publicly available information about customers and list entries from news sources, corporate registries, and government databases. Network analysis tools map hidden relationships between customers and sanctioned parties that wouldn't surface from individual screening—like identifying that your customer's business partner is the adult child of a sanctioned oligarch. Cloud-based platforms deliver instant list updates and provide scalability handling transaction volume spikes without performance degradation during peak periods.

Sanctions and PEP screening anchor modern AML compliance frameworks, protecting individual institutions from regulatory consequences while defending the broader financial system against exploitation. Understanding the distinction matters critically: sanctions screening catches prohibited parties requiring immediate blocking actions, while PEP screening identifies relationships needing enhanced ongoing oversight.

Success extends well beyond implementing screening software. You need comprehensive programs integrating accurate data, current list sources, trained analysts, documented procedures, and robust governance. The challenges—overwhelming false positives, inconsistent data quality, resource limitations—are substantial but manageable through risk-based approaches and continuous refinement.

Regulatory expectations keep tightening while enforcement actions intensify. Institutions treating screening as compliance theater rather than strategic risk management will find themselves increasingly vulnerable. Those investing in sophisticated programs, leveraging advancing technology, and building genuine compliance cultures will navigate this complex landscape successfully.

The stakes transcend institutional self-preservation. Effective screening disrupts terrorist financing networks, impedes weapons proliferation, combats corruption that steals from public treasuries, and advances international security objectives. Financial institutions serve as essential frontline defenders in these efforts—a responsibility demanding sustained commitment and adequate resources.

Commercial use refers to employing copyrighted material for business purposes or financial gain. Understanding these boundaries prevents costly legal disputes and ensures compliance with licensing requirements for images, software, and creative content

The Sarbanes-Oxley Act transformed corporate accountability by making executives personally responsible for financial reporting accuracy. This comprehensive guide explains who must comply, key requirements under Sections 302 and 404, internal control frameworks, audit standards, penalties for violations, and practical implementation steps

Safe harbor codes provide legal protection when businesses meet specific compliance requirements. This comprehensive guide explains how these provisions work across tax law, employment regulations, copyright, and data privacy—plus common mistakes that can eliminate your protection

US companies processing EU residents' data face full GDPR obligations regardless of location. This guide explains when GDPR applies to American businesses, key requirements including consent and data subject rights, compliance steps from data mapping to vendor assessment, and how GDPR differs from US privacy laws

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to business and corporate law, contracts, compliance, disputes, M&A, and taxation for companies.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Legal outcomes may vary depending on jurisdiction, company structure, and individual circumstances.

This website does not provide legal advice, and the information presented should not be used as a substitute for consultation with qualified corporate attorneys or legal professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.