The Sarbanes-Oxley Act emerged from the ashes of corporate scandals that shook investor confidence at the turn of the millennium. Enacted in 2002, this legislation arrived in direct response to accounting frauds at Enron, WorldCom, and Tyco—disasters that erased billions in shareholder value and destroyed thousands of jobs overnight.

Congress designed the law to restore trust in financial reporting. Senator Paul Sarbanes and Representative Michael Oxley sponsored what became the most significant securities legislation since the 1934 Securities Exchange Act. The core purpose: force corporate executives to take personal responsibility for the accuracy of financial statements.

Before SOX, executives could claim ignorance about accounting irregularities. The new framework eliminated that escape route. Chief executive officers and chief financial officers now certify financial reports personally, under penalty of criminal prosecution.

The impact on corporate governance has been profound. Companies established audit committees composed entirely of independent directors. Internal audit functions gained authority and resources. Financial controls became documented, tested, and scrutinized in ways previously reserved for defense contractors or pharmaceutical manufacturers.

Critics initially predicted the law would drive companies to delist from US exchanges or incorporate abroad. While compliance costs did spike—particularly for smaller public companies—the predicted exodus never materialized. Instead, Sarbanes-Oxley corporate governance standards became a global benchmark. Foreign regulators adopted similar frameworks, and investors began demanding SOX-level controls even from private companies preparing for acquisition or public offering.

Twenty-four years later, the law remains controversial. Compliance expenses persist, and debates continue about whether the benefits justify the costs. Yet few dispute that financial reporting today is more reliable than it was in 2001.

Who Must Comply with Sarbanes-Oxley Requirements

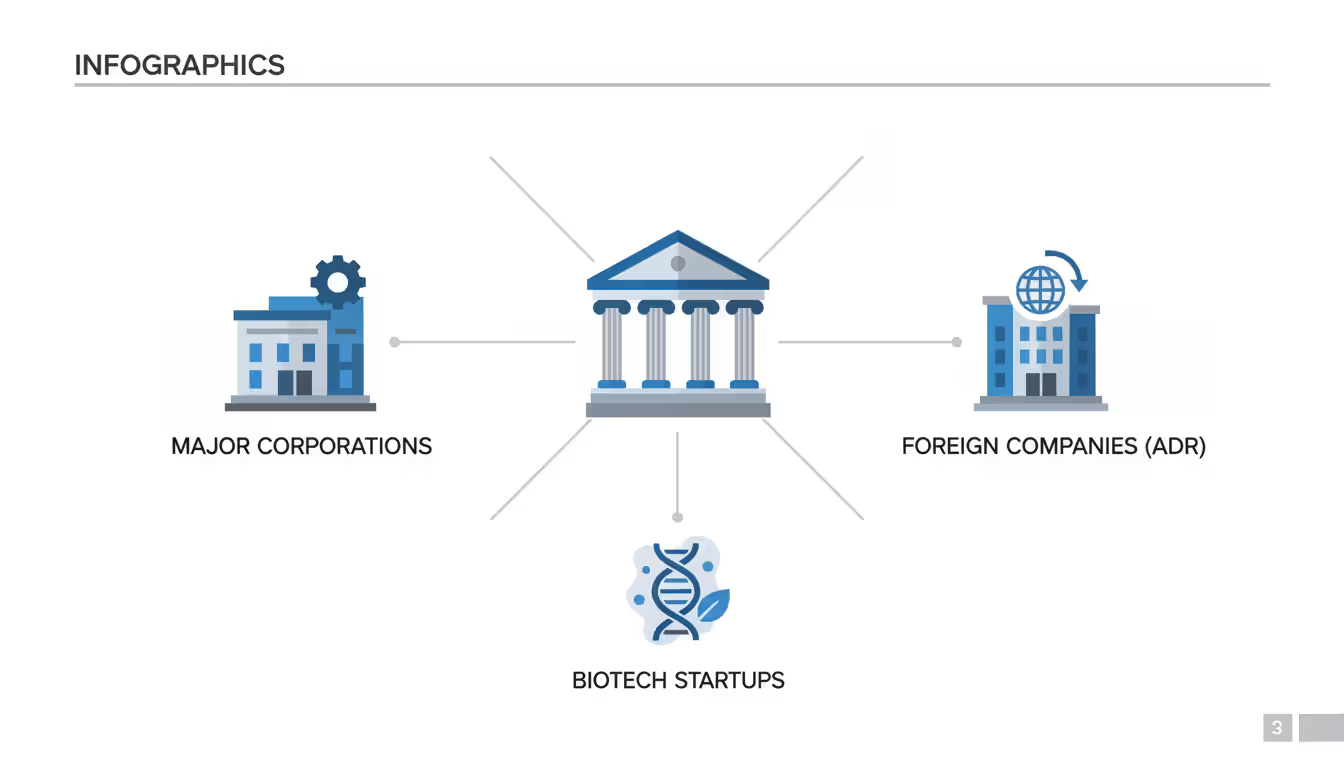

The law applies primarily to companies with securities registered under Section 12 of the Securities Exchange Act of 1934 and those required to file reports under Section 15(d). In practical terms: any company trading on US public exchanges must comply.

This includes domestic corporations and foreign private issuers with American Depositary Receipts (ADRs) trading on NYSE, NASDAQ, or other US markets. A German manufacturer or Japanese technology firm with shares available to US investors faces the same obligations as a Delaware corporation headquartered in Manhattan.

Size offers no exemption. A biotechnology startup completing its initial public offering confronts identical Section 302 certification requirements as a Fortune 500 conglomerate. The law does provide limited accommodations for smaller reporting companies and emerging growth companies—primarily extended timelines for Section 404(b) external auditor attestation—but core requirements remain universal.

Private companies occupy a gray zone. Technically exempt from SOX mandates, they often implement similar controls voluntarily. Venture capital firms increasingly demand SOX-ready internal controls before investing. Private equity buyers discount acquisition prices when targets lack documented financial controls. Companies planning to go public typically spend 18 to 24 months building SOX compliance frameworks before their IPO roadshow.

Wholly-owned subsidiaries of public companies generally fall under their parent's compliance umbrella. The parent company's consolidated financial statements must reflect adequate controls across all material operations, regardless of subsidiary structure.

Nonprofit organizations and government entities remain outside SOX jurisdiction, though some states have enacted analogous requirements for nonprofits receiving public funds.

Author: Samantha Keene;

Source: craftydeb.com

Key SOX Compliance Requirements by Section

The Sarbanes-Oxley Act contains eleven titles spanning everything from audit committee independence to analyst conflicts of interest. Three sections dominate compliance efforts.

Section 302: Corporate Responsibility for Financial Reports

Section 302 makes senior executives personally accountable for financial disclosure. The CEO and CFO must certify in each quarterly and annual report that:

They have reviewed the filing

The report contains no material misstatements or omissions

Financial statements fairly present the company's financial condition

They are responsible for establishing and maintaining internal controls

They have disclosed all significant deficiencies in controls to auditors and the audit committee

They have identified any fraud involving management or employees with significant control roles

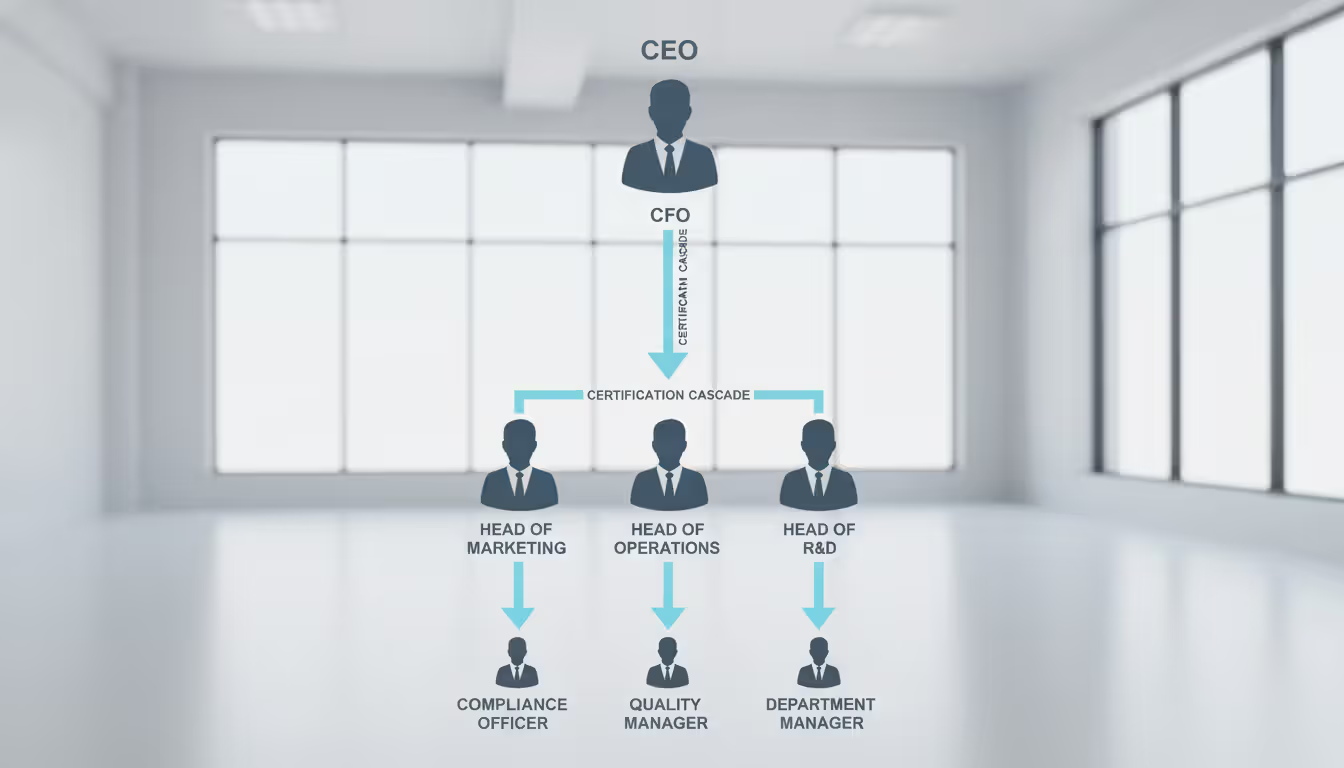

This certification is not ceremonial. Executives sign knowing that false certification carries criminal penalties of up to 20 years imprisonment. The certification cannot be delegated to subordinates or qualified with disclaimers.

SOX Section 302 explained simply: executives must know what's in their financial reports and vouch for its accuracy, or face prison. This shifts risk directly onto the individuals who benefit most from their positions.

Companies typically implement "sub-certifications" cascading down through the organization. Business unit leaders, controllers, and department heads certify the accuracy of their segment's financial data, creating a chain of accountability that supports the CEO and CFO's final certification.

Author: Samantha Keene;

Source: craftydeb.com

Section 404: Management Assessment of Internal Controls

Section 404 requirements represent the most resource-intensive SOX mandate. Management must:

Accept responsibility for establishing and maintaining adequate internal control over financial reporting

Assess the effectiveness of those controls annually

Include in the annual report a statement identifying the framework used to evaluate controls (typically COSO) and management's conclusion about control effectiveness

Section 404(b) adds a second layer: the company's external auditor must attest to and report on management's assessment. This auditor attestation requirement applies to larger filers; smaller reporting companies and emerging growth companies receive temporary or permanent exemptions.

The distinction matters financially. Management's assessment (404(a)) might cost a mid-sized company $500,000 to $1.5 million annually in internal labor and consulting fees. Adding external auditor attestation (404(b)) can double or triple that expense.

Companies must document every financial control—from revenue recognition policies to access controls in accounting systems. They identify key controls, test them for operating effectiveness, remediate deficiencies, and maintain evidence of the entire process. A manufacturing company might test hundreds of controls quarterly: purchase order approvals, inventory counts, depreciation calculations, payroll authorizations, bank reconciliations.

The testing burden never ends. Controls must be re-evaluated each year because business processes change, systems are upgraded, and personnel turn over.

Author: Samantha Keene;

Source: craftydeb.com

Section 906: Criminal Penalties for Certifying Misleading Reports

Section 906 creates criminal liability for executives who certify financial reports knowing they fail to comply with SEC requirements. Penalties reach $5 million in fines and 20 years imprisonment for willful violations.

This section differs from Section 302 in burden of proof. Section 302 violations can be prosecuted as strict liability offenses; Section 906 requires prosecutors to prove knowledge or willfulness. In practice, Section 906 serves as the enforcement mechanism for the most egregious violations—cases where executives clearly knew their certifications were false.

The threat is not theoretical. Multiple executives have been sentenced under Section 906, including Richard Scrushy of HealthSouth and Bernard Ebbers of WorldCom.

Internal Controls and Audit Requirements Under SOX

Sarbanes-Oxley internal controls follow the COSO framework in most implementations. The Committee of Sponsoring Organizations published its Internal Control—Integrated Framework in 1992, updated in 2013, providing a structured approach to designing, implementing, and evaluating controls.

COSO identifies five components: control environment, risk assessment, control activities, information and communication, and monitoring. Within these components, companies design controls addressing specific financial reporting risks.

A revenue recognition control might require sales contracts above $100,000 to receive legal review before booking revenue. An inventory control might mandate physical counts reconciled to system records quarterly. A payroll control might require human resources approval before adding employees to the payment system.

Controls are classified as preventive (stopping errors before they occur) or detective (identifying errors after the fact). Preventive controls generally receive higher marks because they avoid the need for correction. A system that prevents non-approved vendors from being paid is superior to a monthly review that detects unauthorized payments after money has left the bank.

Documentation standards are exacting. Each control requires a written description, identification of the control owner, specification of the control frequency (daily, monthly, quarterly), and definition of evidence that the control operated. A bank reconciliation control might specify: "Treasury analyst reconciles bank statements to general ledger within five business days of month-end, documents reconciling items on standard template, and obtains controller approval via email."

Testing procedures vary by control risk. High-risk controls affecting material account balances receive more frequent testing with larger sample sizes. A company might test monthly revenue recognition controls every quarter using samples of 25 to 40 transactions, while testing annual fixed asset depreciation calculations once per year with a smaller sample.

External auditors play a dual role. They audit the financial statements and, for companies subject to Section 404(b), they audit management's assessment of internal controls. This creates a "double audit"—one focused on whether the numbers are correct, another focused on whether the processes producing those numbers are reliable.

SOX audit requirements mandate auditor independence. Accounting firms cannot provide certain non-audit services to audit clients. Audit partners must rotate off engagements after five years. Audit committees, not management, hire and compensate auditors.

The Public Company Accounting Oversight Board (PCAOB), created by SOX, inspects audit firms and can sanction auditors for deficient work. This regulatory oversight replaced the profession's previous self-regulation model.

How to Implement a SOX Compliance Program

Building a functional compliance program requires more than checking boxes. Companies that treat SOX as a paperwork exercise inevitably face deficiencies, restatements, or worse.

Risk assessment comes first. Finance teams identify financial statement accounts and disclosures material to investors. A software company might determine that revenue, deferred revenue, accounts receivable, and stock-based compensation are material. A manufacturer adds inventory, fixed assets, and warranty reserves.

For each material account, the team identifies what could go wrong. Revenue might be recognized prematurely. Inventory might be obsolete but carried at full value. Receivables might be uncollectible but not reserved.

Control design follows risk identification. For each identified risk, the company designs controls to prevent or detect the error. Controls should be specific, measurable, and assigned to individuals with appropriate authority and competence.

Avoid vague controls like "management reviews financial statements." Instead: "Controller performs analytical review comparing monthly revenue by product line to prior year and budget, investigates variances exceeding 10% or $500,000, documents investigation in variance memo, and obtains CFO approval before closing the books."

Documentation transforms informal practices into auditable evidence. Companies create control matrices listing each control, its objective, the risk it addresses, the control owner, the frequency, and the evidence produced. They develop process narratives describing how transactions flow through systems. They maintain policies and procedures governing financial processes.

Many companies use governance, risk, and compliance (GRC) software to manage documentation. These platforms store control descriptions, track testing schedules, manage deficiencies, and generate reports for auditors.

Testing validates that controls work as designed. The finance team or internal audit function selects samples of transactions and examines evidence that controls operated. For a purchase order approval control, testers might select 30 purchase orders and verify each bears the required approval signature or electronic workflow approval before payment was issued.

Testing frequency depends on control risk and the company's assessment approach. Most companies test key controls quarterly to accumulate evidence throughout the year rather than scrambling before the annual audit.

Remediation addresses identified deficiencies. When controls fail—approvals are missing, reconciliations are late, system access is too broad—the company must investigate root causes and implement corrective actions. Deficiencies are categorized by severity: control deficiencies, significant deficiencies, and material weaknesses.

Material weaknesses must be disclosed in SEC filings and remediated promptly. A material weakness indicates reasonable possibility that a material misstatement would not be prevented or detected. Investors react negatively to material weakness disclosures; stock prices often drop on the news.

Continuous monitoring sustains compliance. SOX is not a one-time project. Companies must update controls when processes change, re-test controls periodically, train new employees on control responsibilities, and maintain documentation. The compliance program becomes part of the organization's operational rhythm.

The Sarbanes-Oxley Act has fundamentally changed the relationship between corporate management and their auditors, and between both of them and the board of directors. It has restored investor confidence by making clear that those who are responsible for a company's financial reports must actually be held responsible

— Chairman Christopher

Penalties for Non-Compliance and Enforcement Actions

Sarbanes-Oxley penalties split between civil and criminal tracks, with consequences for both companies and individuals.

Civil penalties start with SEC enforcement actions. The Commission can impose monetary fines, require disgorgement of ill-gotten gains, ban individuals from serving as officers or directors, and suspend or revoke broker-dealer registrations. In 2025, the SEC brought enforcement actions against 17 companies for SOX violations, with settlements ranging from $250,000 to $8 million.

Criminal prosecution escalates the stakes dramatically. The Department of Justice can charge executives under Section 906 (false certifications), Section 807 (securities fraud), or traditional mail and wire fraud statutes. Convictions carry prison sentences measured in years, not months.

Real-world examples illustrate the risks. In 2023, the former CFO of a medical device company received a four-year prison sentence for certifying false financial statements that overstated revenue by $45 million. In 2024, a software company CEO paid $2.5 million to settle SEC charges related to inadequate internal controls that failed to detect a $12 million accounting error.

Beyond regulatory penalties, SOX violations trigger shareholder lawsuits, director and officer liability claims, and reputational damage. Companies that restate financials due to control failures watch their stock prices decline 10% to 30% on average. Credit ratings may be downgraded. Customer and supplier relationships suffer when stakeholders question financial stability.

The personal toll on executives can be devastating. Even when criminal charges are not filed, executives lose their jobs, pay settlements from personal assets, and find future employment opportunities limited. Directors face shareholder derivative suits alleging breach of fiduciary duty for failing to maintain adequate oversight.

Audit committees and boards increasingly demand robust compliance programs not from regulatory zeal but from rational risk management. The cost of prevention—perhaps $1 million to $3 million annually for a mid-sized public company—pales against the cost of failure.

Frequently Asked Questions About SOX Compliance

Does Sarbanes-Oxley apply to private companies?

No, private companies are not legally required to comply with SOX. The law applies only to companies with securities registered with the SEC or required to file periodic reports. However, many private companies voluntarily implement SOX-type controls. Venture capital investors often require portfolio companies to maintain documented financial controls. Private equity buyers conduct SOX readiness assessments during due diligence and adjust purchase prices when controls are weak. Companies planning to go public typically begin SOX compliance 18 to 24 months before their IPO to avoid scrambling after becoming public.

What is the difference between Section 302 and Section 404?

Section 302 requires CEO and CFO certification of financial reports and disclosure controls. It focuses on executive accountability and personal responsibility. Section 404 requires management to assess and report on the effectiveness of internal controls over financial reporting, with external auditor attestation for most companies. Section 302 is a quarterly certification; Section 404 is an annual assessment. Both are mandatory, but Section 404 demands far more documentation, testing, and resources. Think of Section 302 as the executive promise and Section 404 as the proof supporting that promise.

How often must SOX audits be conducted?

External auditors conduct SOX audits annually in conjunction with the year-end financial statement audit. However, companies perform internal testing throughout the year. Most organizations test key controls quarterly to build evidence supporting the annual assessment. High-risk controls might be tested monthly. The external auditor's fieldwork typically occurs in the fourth quarter and continues through the audit opinion date, usually 60 to 90 days after year-end. Interim reviews by external auditors occur quarterly but focus primarily on financial statements rather than comprehensive control testing.

Can executives go to jail for SOX violations?

Yes. Section 906 provides criminal penalties up to 20 years imprisonment for willfully certifying false financial reports. Multiple executives have been sentenced to prison for SOX violations. The former CEO of WorldCom received 25 years (later reduced to 13 years). HealthSouth's CEO was acquitted on SOX charges but convicted on other fraud counts. The threat of criminal prosecution is real and serves as the ultimate enforcement mechanism. Even when criminal charges are not filed, executives face civil penalties, loss of employment, and professional reputational damage that effectively ends their careers.

What are the most common SOX compliance mistakes?

The most frequent errors include: inadequate documentation of controls (vague descriptions that auditors cannot test), failure to test controls with sufficient sample sizes or frequency, not updating controls when business processes change, treating SOX as an annual event rather than continuous process, relying on detective controls when preventive controls are feasible, poor segregation of duties in small finance teams, and inadequate IT general controls over financial systems. Another common mistake is management override—executives bypassing controls for "business reasons," which defeats the entire purpose of the control framework and creates material weaknesses.

How much does SOX compliance cost?

Costs vary dramatically based on company size, complexity, and maturity of the compliance program. First-year implementation for a newly public mid-sized company might range from $1.5 million to $4 million, including consulting fees, software, internal labor, and incremental external audit fees. Ongoing annual costs typically decrease to $800,000 to $2 million as processes mature. Large multinational corporations spend $10 million to $50 million annually. Smaller reporting companies exempt from Section 404(b) auditor attestation might spend $300,000 to $800,000. Internal labor represents 50% to 60% of total costs—finance staff time spent documenting, testing, and remediating controls.

Sarbanes-Oxley compliance remains a cornerstone of financial reporting integrity for US public companies. The law transformed corporate governance by making executives personally accountable for financial accuracy and requiring rigorous internal controls over financial reporting.

Compliance demands sustained investment in people, processes, and technology. Companies must document controls, test them regularly, remediate deficiencies promptly, and maintain evidence sufficient to support management's annual assessment and the CEO and CFO's quarterly certifications.

The stakes are high. Criminal penalties, SEC enforcement actions, shareholder lawsuits, and reputational damage await companies that treat SOX as a checkbox exercise. Yet organizations that build robust compliance programs gain more than regulatory protection—they develop financial discipline, operational transparency, and investor confidence that create competitive advantages.

Twenty-four years after enactment, the debate about costs versus benefits continues. Compliance expenses remain substantial, particularly for smaller public companies. Yet the financial scandals that prompted the law have not recurred at the same scale. Financial restatements, while still occurring, are less frequent and less severe than in the pre-SOX era.

For companies entering public markets in 2026, SOX compliance is not optional—it's the price of admission. The most successful organizations integrate compliance into their operational DNA rather than treating it as a separate regulatory burden. They recognize that strong internal controls serve business objectives beyond compliance: preventing errors, detecting fraud, supporting decision-making, and enabling growth.

Building an effective compliance program requires executive commitment, adequate resources, and sustained attention. Companies that invest wisely in SOX compliance protect themselves from regulatory penalties while building financial infrastructure that supports long-term success.

Commercial use refers to employing copyrighted material for business purposes or financial gain. Understanding these boundaries prevents costly legal disputes and ensures compliance with licensing requirements for images, software, and creative content

Financial institutions rely on sanctions and PEP screening to prevent money laundering and meet AML compliance obligations. This guide explains how sanctions list screening and politically exposed person checks work, regulatory requirements, implementation challenges, and best practices for building effective programs

Safe harbor codes provide legal protection when businesses meet specific compliance requirements. This comprehensive guide explains how these provisions work across tax law, employment regulations, copyright, and data privacy—plus common mistakes that can eliminate your protection

US companies processing EU residents' data face full GDPR obligations regardless of location. This guide explains when GDPR applies to American businesses, key requirements including consent and data subject rights, compliance steps from data mapping to vendor assessment, and how GDPR differs from US privacy laws

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to business and corporate law, contracts, compliance, disputes, M&A, and taxation for companies.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Legal outcomes may vary depending on jurisdiction, company structure, and individual circumstances.

This website does not provide legal advice, and the information presented should not be used as a substitute for consultation with qualified corporate attorneys or legal professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.