When a business needs to execute contracts, open bank accounts, or enter legally binding agreements, someone must have the authority to sign on behalf of the organization. That person is an authorized signatory—a role that carries significant legal weight and responsibility. Understanding this designation helps businesses protect themselves while enabling efficient operations.

Authorized Signatory Meaning and Definition

An authorized signatory is an individual who has been granted explicit permission to sign documents and enter agreements that legally bind an organization. This authority stems from formal designation by the company's governing body, typically through board resolutions, operating agreements, or corporate bylaws.

The basic purpose is straightforward: corporations and other business entities cannot physically sign documents themselves. They need human representatives who can execute transactions, contracts, and legal instruments on their behalf. Unlike informal arrangements where someone might sign paperwork as a favor, authorized signatories operate within defined parameters that specify exactly what they can and cannot commit the organization to do.

Authorized signatories appear across numerous contexts. Banks require them for account access and financial transactions. Vendors need them to execute purchase agreements. Real estate transactions, employment contracts, vendor agreements, and regulatory filings all typically require signatures from individuals with documented authority. The scope varies dramatically—some authorized signatories can bind a company to multi-million dollar commitments, while others might only approve routine supply orders under $5,000.

The designation protects both the organization and third parties. Companies gain control over who can create legal obligations, while outside parties get assurance that the person signing actually has authority to do so.

Who Can Be an Authorized Signatory

Legal capacity forms the baseline requirement. The individual must be of legal age (18 or older in most states) and mentally competent. Beyond that, eligibility depends on organizational structure, internal policies, and the specific authority being granted.

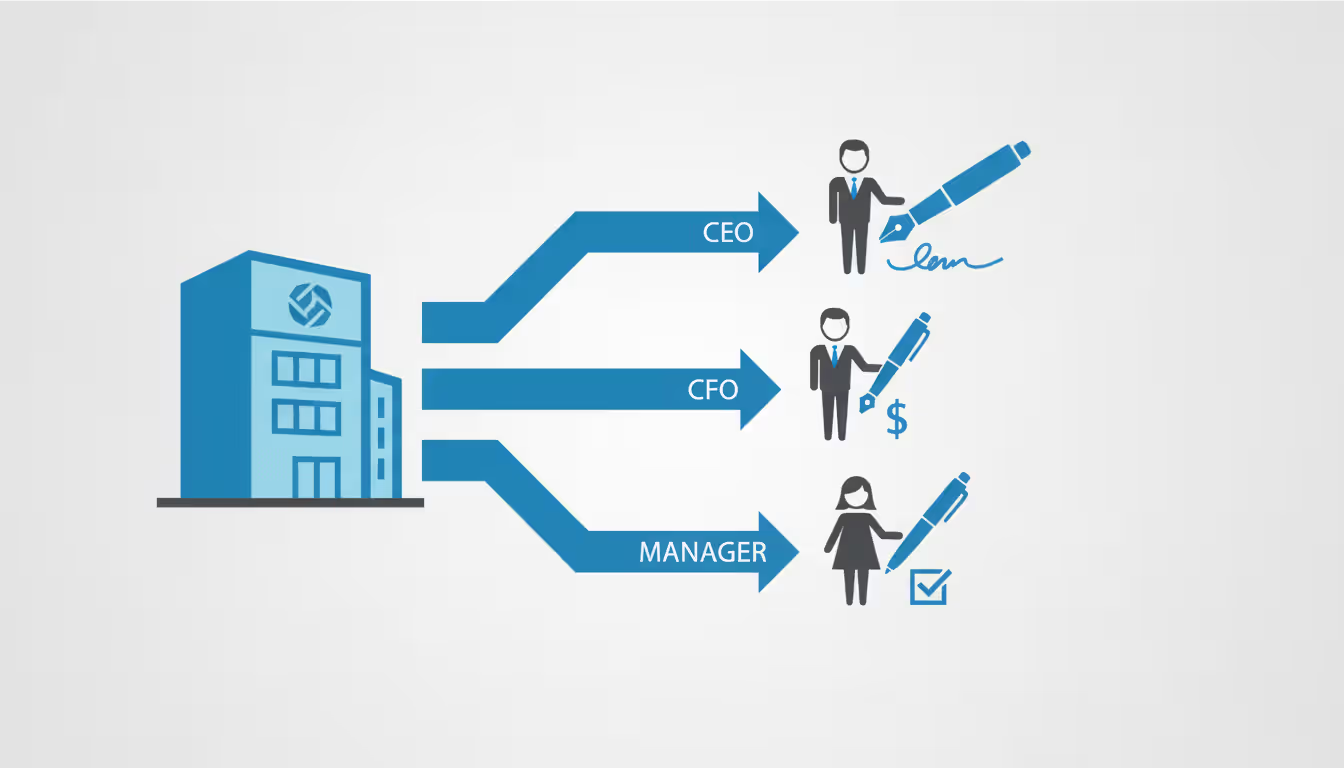

Most authorized signatories fall into predictable categories: corporate officers (CEO, CFO, President), board members, business owners, and designated managers. However, the role isn't restricted to senior leadership. A purchasing manager might serve as an authorized signatory for vendor contracts within their department's budget. A branch manager could have signing authority for local operational agreements. Some organizations designate administrative staff as authorized signatories for routine documents that don't require executive involvement.

The key distinction is formal designation. A vice president might assume they have signing authority based on their title alone, but without proper documentation granting that authority, their signature may not bind the company.

Corporate Authorized Signatory Roles

In corporations, authorized signatory roles typically align with the organizational hierarchy established in bylaws. The CEO or President generally holds broad signing authority by default. The CFO or Treasurer usually has specific authority over financial matters, banking relationships, and fiscal commitments.

Corporate secretaries often serve as authorized signatories for official filings, stock certificates, and corporate records. Board chairs may have authority for major strategic agreements approved by the board. Vice presidents and directors might receive limited signing authority within their functional areas—a VP of Operations signing facility leases, for instance, or a Director of Human Resources executing employment agreements.

Many corporations implement dual-signature requirements for transactions exceeding certain thresholds. A $50,000 contract might require signatures from both a department head and the CFO, preventing any single individual from committing substantial resources without oversight.

Authorized Signatory Requirements by Entity Type

LLCs typically designate authorized signatories through their operating agreement. Members or managers receive signing authority based on their ownership stake or management role. Single-member LLCs have straightforward arrangements—the sole member signs everything—but multi-member LLCs benefit from clearly documented authority to prevent disputes.

Partnerships usually grant all general partners signing authority unless the partnership agreement specifies otherwise. Limited partners typically cannot bind the partnership, though exceptions exist when they assume management roles.

Nonprofits commonly require board approval for authorized signatories. The executive director usually receives broad authority for operational matters, while the board president or treasurer handles major financial commitments. Many nonprofits mandate dual signatures for checks or contracts above specific amounts, building in financial controls.

Sole proprietorships have the simplest arrangement—the owner is the authorized signatory for all purposes, though they may grant power of attorney to others for specific transactions.

Authorized Signatory in Contracts and Legal Documents

When an authorized signatory executes a contract, they create legally enforceable obligations for the organization they represent. The signature block typically includes the individual's name, title, and the entity name, clearly indicating they're signing in a representative capacity rather than personally.

Proper execution format matters. A signature reading "John Smith, CEO, Acme Corporation" binds Acme Corporation. A signature showing just "John Smith" might inadvertently create personal liability, especially if the signer's representative capacity isn't clear from context.

The scope of authority determines what an authorized signatory can commit to. This scope should be documented in corporate resolutions, banking agreements, or authorization letters. A signatory might have unlimited authority for operational contracts but require board approval for commitments exceeding $100,000, acquisitions, real estate transactions, or agreements longer than three years.

Third parties entering contracts have a reasonable duty to verify signing authority, particularly for significant transactions. They typically request a corporate resolution or certificate of authority confirming the individual's power to bind the organization. However, if a company allows someone to act as an authorized signatory without objection, it may be estopped from later claiming the signature was unauthorized.

Author: Samantha Keene;

Source: craftydeb.com

Limitations and restrictions create important boundaries. An authorized signatory cannot typically bind the organization to matters outside their designated scope, even if they hold a senior title. The CFO authorized to sign financial agreements might lack authority to execute employment contracts. A regional manager with authority for local vendor agreements cannot commit the company to a national distribution deal.

Authorized Signatory vs Power of Attorney

While both roles involve signing authority, authorized signatories and attorneys-in-fact (those holding power of attorney) operate under different legal frameworks with distinct purposes.

Aspect

Authorized Signatory

Power of Attorney

Authority Source

Corporate resolution, bylaws, operating agreement, or board action

Formal power of attorney document executed by the principal

Scope

Typically limited to specific business functions or transaction types

Can be broad (general) or narrow (limited/special); often very specific

Duration

Ongoing until revoked or role changes; tied to position

May be temporary, event-specific, or durable; often expires on specific date

Principal can revoke anytime (unless durable and principal becomes incapacitated)

Typical Use Cases

Routine business operations, banking, contracts, vendor agreements

One-time transactions, temporary absence, incapacity planning, real estate closings

Legal Formality

Internal corporate documentation; may require certification for banks

Requires notarization; often needs recording for real estate; strict statutory requirements

The fundamental difference lies in the relationship structure. Authorized signatories derive authority from their role within an organization's governance framework. Power of attorney creates a principal-agent relationship where one person (the principal) grants another (the attorney-in-fact) authority to act on their behalf.

A corporation might grant power of attorney to an attorney for a specific real estate closing when the authorized signatory cannot attend. That's appropriate for a one-time event. Making that attorney an authorized signatory would be unusual unless they're joining the company in an official capacity.

Revocation processes differ significantly. Removing an authorized signatory requires corporate action—board resolutions, amended banking agreements, updated signature cards. Revoking power of attorney typically requires only written notice from the principal to the attorney-in-fact and relevant third parties, though practical complications arise if the power of attorney has been recorded or relied upon.

Authorized Signer for Business and Banking

Banks require explicit documentation of authorized signers before granting account access or transaction authority. When opening a business account, banks typically request a corporate resolution or banking resolution identifying who can sign checks, initiate wire transfers, access account information, and make other financial decisions.

Financial transaction authority varies by designation. Some authorized signers have view-only access for monitoring purposes. Others can write checks up to certain limits. Senior signatories might have unlimited authority to move funds, close accounts, or establish new banking relationships.

Most banks distinguish between individual and dual signature requirements based on transaction type and amount. A company might allow any authorized signer to write checks under $10,000, but require two signatures for larger amounts. Wire transfers often require dual authorization regardless of amount, given their irreversible nature and fraud risk.

Author: Samantha Keene;

Source: craftydeb.com

Documentation needed for banks includes certified board resolutions listing authorized signers by name and title, specifying their authority levels, and including specimen signatures. Many banks use standardized forms—corporate signature cards or authorized signer agreements—that must be completed, notarized, and kept on file.

Adding authorized signers requires submitting updated resolutions and new signature cards. The process protects banks from liability if they honor signatures from individuals who lack actual authority. Banks can rely on resolutions and signature cards until formally notified of changes.

Removing authorized signers demands proactive notification. When an employee with signing authority leaves the company, businesses must immediately notify all banks, update signature cards, and submit new resolutions. Failure to do so leaves the organization vulnerable—the departed employee retains technical authority until the bank receives proper documentation removing them.

Account reconciliation becomes more complex with multiple authorized signers. Companies should implement internal controls tracking who signed what, matching signatures on checks and authorization forms to approved signatories, and flagging discrepancies.

How to Designate an Authorized Signatory

The designation process varies by entity type but follows a general pattern requiring formal documentation and proper authorization.

For corporations, the board of directors typically passes a resolution identifying authorized signatories, specifying their authority scope, and setting any limitations or dual-signature requirements. The corporate secretary records this resolution in the corporate minutes. The resolution should include:

Full legal names and titles of authorized signatories

Specific powers granted (contracts, banking, real estate, etc.)

Dollar limits or transaction type restrictions

Effective date and any expiration terms

Dual-signature requirements if applicable

Author: Samantha Keene;

Source: craftydeb.com

LLCs document authorized signatories through their operating agreement or through written consent of members/managers. If the operating agreement already designates managers with signing authority, no additional documentation may be needed. Otherwise, members should adopt a resolution similar to corporate resolutions.

Partnerships should amend their partnership agreement or adopt a partnership resolution documenting which partners (or employees, in some cases) have signing authority and for what purposes.

Required documentation extends beyond internal records. Banks need certified resolutions and signature cards. Vendors entering significant contracts may request certificates of authority. Some states require authorized signatories to be listed in annual reports or registered with the Secretary of State for certain entity types.

The corporate secretary or equivalent officer typically certifies that resolutions are accurate and currently in effect. This certification, often notarized, provides third parties with confidence that the signatory has actual authority.

Official registration procedures vary by jurisdiction and transaction type. Real estate transactions may require recording authorized signatory designations with county recorders. Securities transactions might need SEC or FINRA documentation. Government contracts often require specific authorization forms and representations.

After designation, communicate the change to all relevant parties: banks, major vendors, insurance companies, legal counsel, and accountants. Update internal systems to reflect who can approve what, preventing unauthorized commitments and ensuring proper workflow routing.

Common Mistakes and Risks with Authorized Signatories

Scope creep represents a frequent problem. An employee designated to sign routine purchase orders starts executing service agreements, then facility leases, then employment contracts—each step seeming like a logical extension of their authority. Without clear boundaries and enforcement, authorized signatories often exceed their actual authority, creating legal ambiguity and potential liability.

Author: Samantha Keene;

Source: craftydeb.com

Lack of documentation creates vulnerability. A CEO verbally tells the operations manager to "handle the vendor contracts," and the manager signs agreements for months. When a dispute arises, the company claims the manager lacked authority, but the vendor argues the company held out the manager as authorized. Courts may find apparent authority existed, binding the company despite the absence of formal designation.

Failure to update records after personnel changes causes significant problems. An employee with signing authority leaves the company, but no one notifies the bank or updates corporate resolutions. Six months later, the former employee writes checks on the company account—technically still authorized based on outdated bank records. Recovery becomes a criminal matter rather than a simple reversal.

Similar issues arise when authority should be modified but isn't. A CFO gets demoted to controller but remains listed as an authorized signatory with broad financial authority. The company assumes the demotion revoked signing rights, but without formal documentation, the authority persists.

Liability issues emerge when authorized signatories act negligently or outside their scope. If a signatory commits the company to an agreement knowing it violates corporate policy or exceeds their authority, they may face personal liability for resulting damages. Directors and officers insurance doesn't always cover intentional acts or knowing violations.

The single most important protection for any business is maintaining current, specific documentation of authorized signatory authority. Vague resolutions saying someone 'can sign contracts' create more problems than they solve. Specify what types of contracts, what dollar limits, what approval processes apply, and update these designations whenever roles change

— Margaret Chen

Overlapping authority without coordination leads to duplicated efforts or conflicting commitments. Two authorized signatories might each sign agreements with competing vendors for the same service, both believing they're acting properly. Clear internal communication and approval workflows prevent these scenarios.

Insufficient due diligence by third parties creates mutual risk. A vendor accepts a signature from someone claiming to be an authorized signatory without requesting proof. If that person lacked actual authority, the contract may be voidable, wasting everyone's time and resources. Both parties benefit from proper verification.

Frequently Asked Questions About Authorized Signatories

Can an authorized signatory sign any document on behalf of a company?

No. Authorized signatories can only sign documents within their designated scope of authority. A signatory authorized for vendor contracts cannot bind the company to real estate purchases or employment agreements unless specifically granted that authority. The authorizing resolution or agreement defines what types of documents and transactions fall within their power. Exceeding that scope may result in an invalid signature that doesn't bind the company, though apparent authority doctrines sometimes create exceptions.

Does an authorized signatory need to be an employee?

Not necessarily. While most authorized signatories are employees, officers, or owners, companies can designate outside parties for specific purposes. A law firm partner might be designated as an authorized signatory for a particular litigation matter. An accountant could receive authorization to sign tax documents. However, granting broad signing authority to non-employees creates control and liability risks, so it's typically limited to narrow, specific purposes with clear boundaries.

How do you prove someone is an authorized signatory?

Proof comes from certified corporate documents. A Certificate of Authority or Certificate of Incumbency, signed by the corporate secretary and often notarized, confirms that specific individuals hold particular positions with defined signing authority. Board resolutions or operating agreement excerpts serve similar purposes. Banks maintain signature cards with specimen signatures. For significant transactions, third parties should request current certification—documents more than 90 days old may not reflect recent changes. Some jurisdictions allow verification through Secretary of State filings for certain entity types.

Can a company have multiple authorized signatories?

Yes, and most companies do. Different signatories often have authority for different purposes—one for contracts, another for banking, another for regulatory filings. This division of responsibility provides operational flexibility and internal controls. Many companies also designate backup signatories to ensure business continuity when primary signatories are unavailable. However, having multiple signatories requires clear documentation of each person's specific authority to prevent confusion and unauthorized actions.

What happens if an unauthorized person signs a contract?

The contract may be voidable at the company's option, meaning the company can choose to enforce it or reject it. If the company ratifies the contract through its actions—accepting performance, making payments, or otherwise treating it as valid—it may become bound despite the initial lack of authority. Third parties who reasonably relied on apparent authority (the company held out the person as authorized) might successfully enforce the contract even without formal designation. The unauthorized signer may face personal liability for damages if the other party relied on false representations of authority.

How do you remove an authorized signatory?

Removal requires formal corporate action similar to designation. The board of directors passes a resolution revoking the individual's signing authority, the corporate secretary records it in the minutes, and the company notifies all relevant third parties—banks, vendors, partners. Banks need updated signature cards and certified resolutions. Major vendors should receive written notice. The company should also retrieve any signature stamps, check stock, or other materials the former signatory possessed. Immediate action is critical when an employee with signing authority leaves the company, especially if the departure is contentious.

Authorized signatories form the essential link between organizations and the legal commitments they make. Proper designation, clear documentation, and regular updates protect companies from unauthorized obligations while enabling efficient operations. The role carries significant responsibility—authorized signatories must understand their scope of authority, act within those bounds, and recognize when corporate approval is required before signing.

Whether you're designating your first authorized signatory or managing a complex structure with multiple signers across departments, the fundamentals remain constant: formal authorization through proper corporate channels, clear documentation of scope and limits, communication to all affected parties, and diligent updates when roles or circumstances change. These practices prevent the common pitfalls that create legal disputes, financial losses, and operational disruptions.

For businesses establishing or reviewing their authorized signatory structure, consulting with legal counsel ensures compliance with state law requirements and alignment with best practices for your entity type and industry. The investment in proper documentation and processes pays dividends through reduced risk and smoother business operations.

Commercial use refers to employing copyrighted material for business purposes or financial gain. Understanding these boundaries prevents costly legal disputes and ensures compliance with licensing requirements for images, software, and creative content

The Sarbanes-Oxley Act transformed corporate accountability by making executives personally responsible for financial reporting accuracy. This comprehensive guide explains who must comply, key requirements under Sections 302 and 404, internal control frameworks, audit standards, penalties for violations, and practical implementation steps

Financial institutions rely on sanctions and PEP screening to prevent money laundering and meet AML compliance obligations. This guide explains how sanctions list screening and politically exposed person checks work, regulatory requirements, implementation challenges, and best practices for building effective programs

Safe harbor codes provide legal protection when businesses meet specific compliance requirements. This comprehensive guide explains how these provisions work across tax law, employment regulations, copyright, and data privacy—plus common mistakes that can eliminate your protection

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to business and corporate law, contracts, compliance, disputes, M&A, and taxation for companies.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Legal outcomes may vary depending on jurisdiction, company structure, and individual circumstances.

This website does not provide legal advice, and the information presented should not be used as a substitute for consultation with qualified corporate attorneys or legal professionals.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.